The investment philosophy of legendary fund manager Peter Lynch, as detailed in his book One Up on Wall Street, focuses on finding high-quality, growing companies trading at sensible prices. Often called a Growth at a Reasonable Price (GARP) method, Lynch’s process sidesteps speculative, high-priced growth stocks for businesses with steady, clear expansion. He used particular quantitative filters to find these companies, concentrating on earnings growth, valuation, profitability, and financial soundness. A recent filter using these Lynch ideas has identified PULTEGROUP INC (NYSE:PHM) as a candidate for more study for long-term investors.

Matching the Lynch Criteria

PulteGroup, a leading U.S. homebuilder with brands like Centex, Pulte Homes, and Del Webb, seems to fit several important parts of Lynch’s method. The filter’s settings are made to find companies with a particular financial picture, and PulteGroup’s present measurements hit these marks.

- Steady Earnings Growth: Lynch wanted companies with a confirmed history of growth, but he was cautious of unsustainably high rates. The filter needed a 5-year earnings per share (EPS) growth average between 15% and 30%. PulteGroup’s EPS has increased at an average yearly rate of 18.05% over this time, fitting well within Lynch’s desired range. This shows a record of good expansion without the warning sign of extreme, possibly temporary growth.

- Sensible Valuation (PEG Ratio): Possibly the central idea of the GARP method, the Price/Earnings to Growth (PEG) ratio helps decide if a stock’s price is fair relative to its growth rate. Lynch preferred companies with a PEG ratio of 1 or lower, hinting the market might be pricing the growth too low. PulteGroup’s PEG ratio, using its past 5-year growth, is 0.59, meaning its present valuation may not completely account for its historical earnings growth.

- Good Profitability (ROE): Return on Equity (ROE) shows how well a company produces profits from shareholder equity. Lynch wanted an ROE above 15% as a mark of a well-run, profitable business. PulteGroup’s ROE of 17.09% is higher than this level, showing efficient use of investor money.

- Financial Soundness (Debt & Liquidity): A careful balance sheet was key for Lynch. He liked companies financed more by equity than debt, often wanting a Debt/Equity ratio below 0.6 (and preferably under 0.25). PulteGroup’s D/E ratio of 0.17 shows a very careful capital structure. Also, its Current Ratio of 6.82 is much higher than the filter’s need of 1, indicating strong liquidity to meet near-term needs, a sign of financial strength.

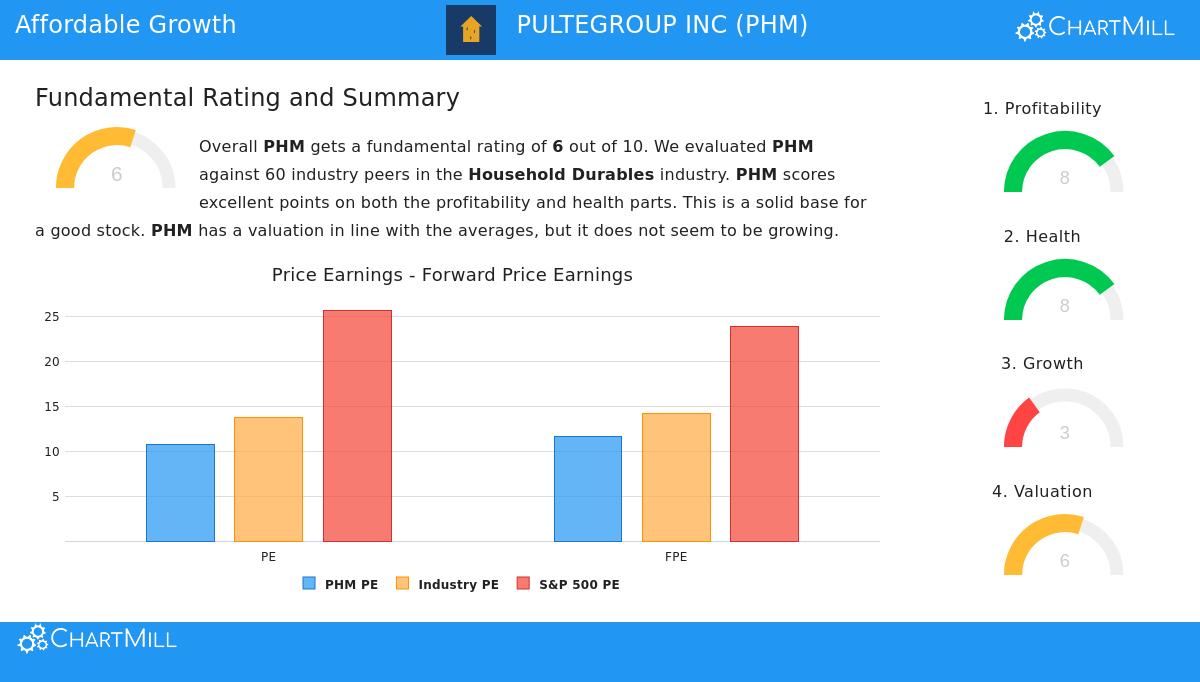

Fundamental Condition Review

Outside the specific filter settings, a wider view of PulteGroup’s fundamental condition supports its position as a financially solid company. Based on ChartMill’s full study, PulteGroup gets an overall fundamental score of 6 out of 10. The report points out two especially good areas:

- Profitability: With a score of 8/10, the company is seen as "very profitable." It performs well in important measurements like Return on Assets (12.29%), Return on Invested Capital (14.00%), and Operating Margin (17.27%), regularly placing in the high end of its Household Durables industry group.

- Financial Health: Also scoring 8/10, PulteGroup’s balance sheet is strong. The report mentions a good Altman-Z score (5.82), showing low bankruptcy risk, and confirms the company is building value as its ROIC is above its cost of capital. The decrease in shares outstanding over recent years is another good point, matching Lynch’s liking for companies that repurchase stock.

The main point of care in the full fundamental report is growth. While past results have been good, recent yearly EPS and revenue have fallen, and future growth projections are moderate. This highlights the Lynch idea that filtering is just the initial stage; investors must then study why growth has weakened and judge the long-term view for the housing market and the company’s place in it.

A Candidate for More Study

For investors following Peter Lynch’s idea of buying understandable businesses with good growth and sensible prices, PulteGroup offers a noteworthy beginning point for careful examination. It meets a strict group of Lynch-based filters, having a history of profitable growth, a careful balance sheet, and a valuation that seems fair compared to its historical growth. The company’s focus on a basic human need, housing, fits the Lynch model of investing in what you understand.

It is key to note that any filter gives a list for more inquiry, not a suggestion to buy. The present neutral short-term direction for the wider S&P 500 also indicates a careful, study-based method is wise. Interested investors should look more closely into industry cycles, interest rate effects, land purchase plans, and management’s methods to handle possible economic challenges.

You can review other companies that presently fit the Peter Lynch investment standards by visiting the Peter Lynch Strategy stock screen.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer to buy or sell any security. The study uses data and a preset filtering method. Investors should do their own complete research and think about their personal financial situation and risk tolerance before making any investment choices. Past performance does not guarantee future results.