The peace talks in Pakistan are over. JD Vance flew home without a deal, Donald Trump ordered the US Navy to blockade the Strait of Hormuz, and anyone who thought last week's ceasefire rally had cleared the air is in for a rude awakening this Monday morning.

The Rundown

- US-Iran nuclear talks in Pakistan ended without agreement, with both delegations walking away from the table

- Trump ordered a full US Navy blockade of the Strait of Hormuz, sharply escalating the Middle East conflict

- US consumer inflation jumped to 3.3% in March, energy prices are the main culprit, and consumers expect it to get worse before it gets better

- AI infrastructure demand kept attracting serious capital, with CoreWeave inking major multi-year supply agreements with two of tech's biggest names

From Ceasefire to Naval Blockade

Friday’s trading session was already subdued. Wall Street saw this week’s rally lose some steam, with investors taking profits rather than risking it all ahead of what was always going to be a crucial weekend in Islamabad.

The Dow Jones had posted its best single day in a year on Wednesday after the Iran-US ceasefire was announced, but translating a temporary truce into anything durable was always going to be the hard part.

It didn't happen. JD Vance sat across the table from Iranian negotiators in Pakistan, laid out Washington's core demand (Iran gives up its nuclear weapons development program full stop) and got a flat refusal. Both delegations left. "The bad news is, we didn't reach a deal," Vance told reporters afterwards.

He added that it was worse for Iran than for the US, which may well be true, but that's a cold comfort when oil markets open Monday morning.

Then Trump responded. The US Navy has been ordered to begin a full blockade of every ship attempting to pass through the Strait of Hormuz, effective immediately. Mines will be cleared. And the warning to Tehran was about as blunt as it gets: "Every Iranian who fires at us or peaceful ships, we will blast to hell."

This is a genuine escalation, not a negotiating posture. The ceasefire was already fragile before it collapsed, Iran's parliament speaker Mohammad Bagher Ghalibaf had been demanding the release of blocked Iranian assets as a precondition before talks even started properly.

That standoff never got resolved. Now the naval blockade puts a hard floor under oil prices and a ceiling on diplomatic optimism.

The Strait of Hormuz is not a secondary concern. Roughly 20% of global oil consumption passes through it. For weeks, Iran had been selectively allowing passage, China, India, Japan and Iraq all negotiated their way through while Western-bound tankers were blocked.

Even with those exceptions, traffic was running at perhaps a quarter of pre-war levels. A US-imposed blockade now adds an entirely different layer of disruption to an already fractured supply chain.

Those Oil Prices? Already Outdated

WTI crude closed Friday at $96.57 per barrel (▼1.3%) and Brent at $95.20 (▼0.8%). Both lost 13-14% on the week as the ceasefire briefly allowed the market to breathe. Don't anchor to those numbers. The spot market was already moving sharply higher by Sunday following Trump's announcement, and Monday's open will tell a very different story.

Energy stocks, defense names and anything upstream in the oil supply chain deserve a close look this week. The inverse is also true, industries with high energy input costs, transport and airlines in particular, are going to feel this quickly.

Inflation: The War Is Already on the Receipt

The March CPI print landed Friday and confirmed what energy prices had been telegraphing for weeks. Headline inflation rose to 3.3% year-on-year, up from 2.4% in February.

Energy prices drove it, a 10.9% monthly surge, the direct result of the Middle East conflict disrupting supply. On a monthly basis, CPI jumped from 0.3% to 0.9%.

The brighter spot: core inflation came in at 2.6% versus 2.5% in February, a slight beat against estimates. But "core" deliberately strips out energy and food, and energy is precisely where this war is being felt. The headline number is the one that lands on kitchen tables.

More telling than March's reading is where consumers think things are going. The University of Michigan's latest survey puts 12-month inflation expectations at 4.8%, a full percentage point higher than in March.

Consumer confidence itself dropped to 47.6 in April, down from 53.3 in March and 52.2 a year ago. To be fair, most of those survey responses were submitted before the April 7 ceasefire announcement. With that ceasefire now in serious jeopardy, I wouldn't expect the next reading to look much better.

The Fed is in an uncomfortable position. Rising headline inflation and deteriorating consumer confidence is the kind of stagflationary mix that makes rate decisions genuinely difficult. Rate cuts are off the table for the foreseeable future.

If oil prices spike materially from Monday's open - and the blockade announcement gives every reason to expect they will - the conversation may eventually shift toward whether additional tightening becomes necessary.

CoreWeave: The Week's Unlikely Standout

In a week dominated by geopolitical noise, one stock cut straight through it.

CoreWeave (CRWV | ▲10.87%) surged 11% on Friday after announcing a multi-year supply agreement with Anthropic, the company behind the Claude AI model. Anthropic will use CoreWeave's cloud and datacenter infrastructure to feed Claude's fast-growing compute requirements.

That followed a billion-dollar deal with Meta Platforms announced on Thursday. Two major AI clients signed in two consecutive days.

Whatever questions linger about CoreWeave's balance sheet (the company simultaneously announced a $3.5 billion convertible debt issuance), the market's message was clear: the revenue pipeline matters more right now.

CoreWeave went public just over a year ago at $40 per share. The journey since has been bumpy, initially shunned for its debt load, then embraced as the AI build-out accelerated, then cooled again heading into 2026. Even after that pullback, it's still trading 160% above the IPO price.

The Anthropic deal suggests AI infrastructure spending isn't slowing down, whatever the macro backdrop looks like.

The broader chip and AI hardware space had a solid day as well. TSMC (TSM | ▲1.4%) reported strong March revenue numbers, beating both monthly and year-on-year comparisons. Nvidia (NVDA | ▲2.57%) and Broadcom (AVGO | ▲4.69%) closed higher alongside it.

Software: Still Looking for a Floor

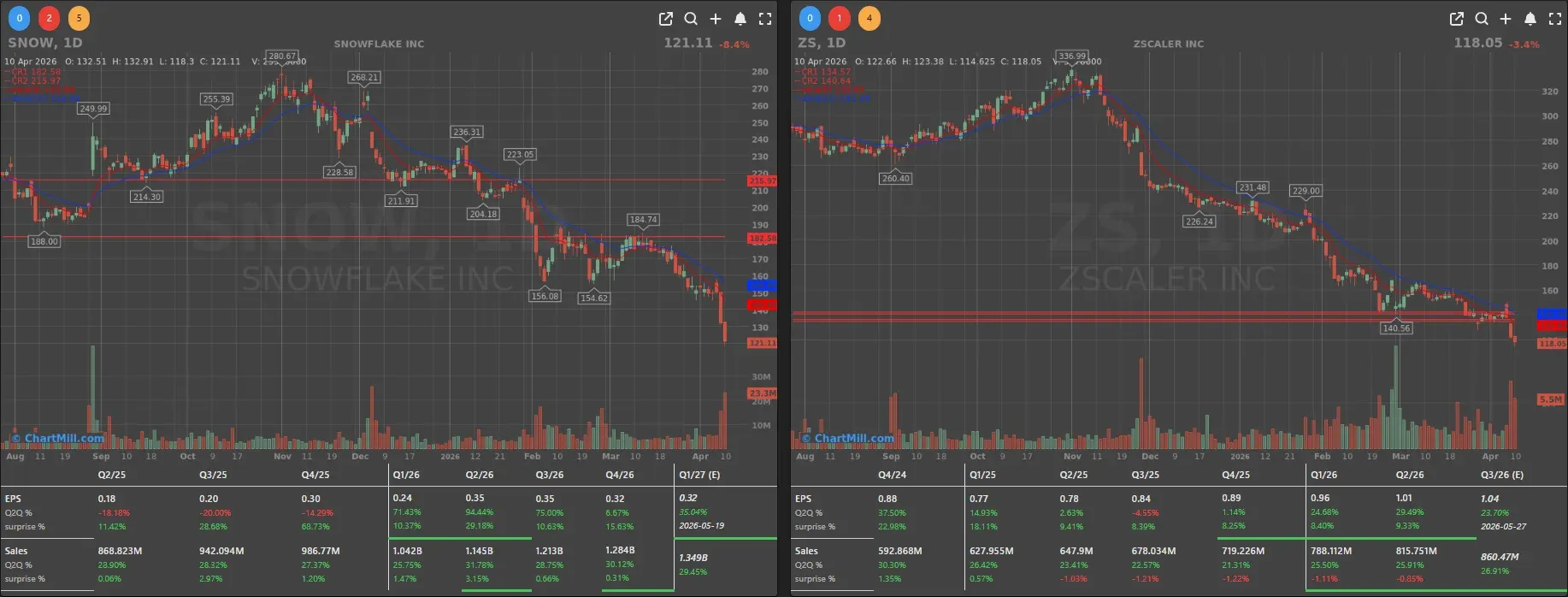

Not all of tech was celebrating. Software names took another hit on Friday, extending Thursday's sell-off.

Snowflake (SNOW | ▼8.4%) and Zscaler (ZS | ▼3.42%) both closed lower for a second straight session, Snowflake has now given back a significant chunk across the two days.

Oracle (ORCL | ▲0.17%) staged a modest recovery after Thursday's 4% drop, but the broader pattern is hard to ignore.

Investors are rotating within tech, out of software and into hardware and infrastructure. What's clear is that the AI investment thesis is increasingly being expressed through picks-and-shovels names like CoreWeave, Nvidia and Broadcom rather than through SaaS multiples.

Macro Snapshot

-

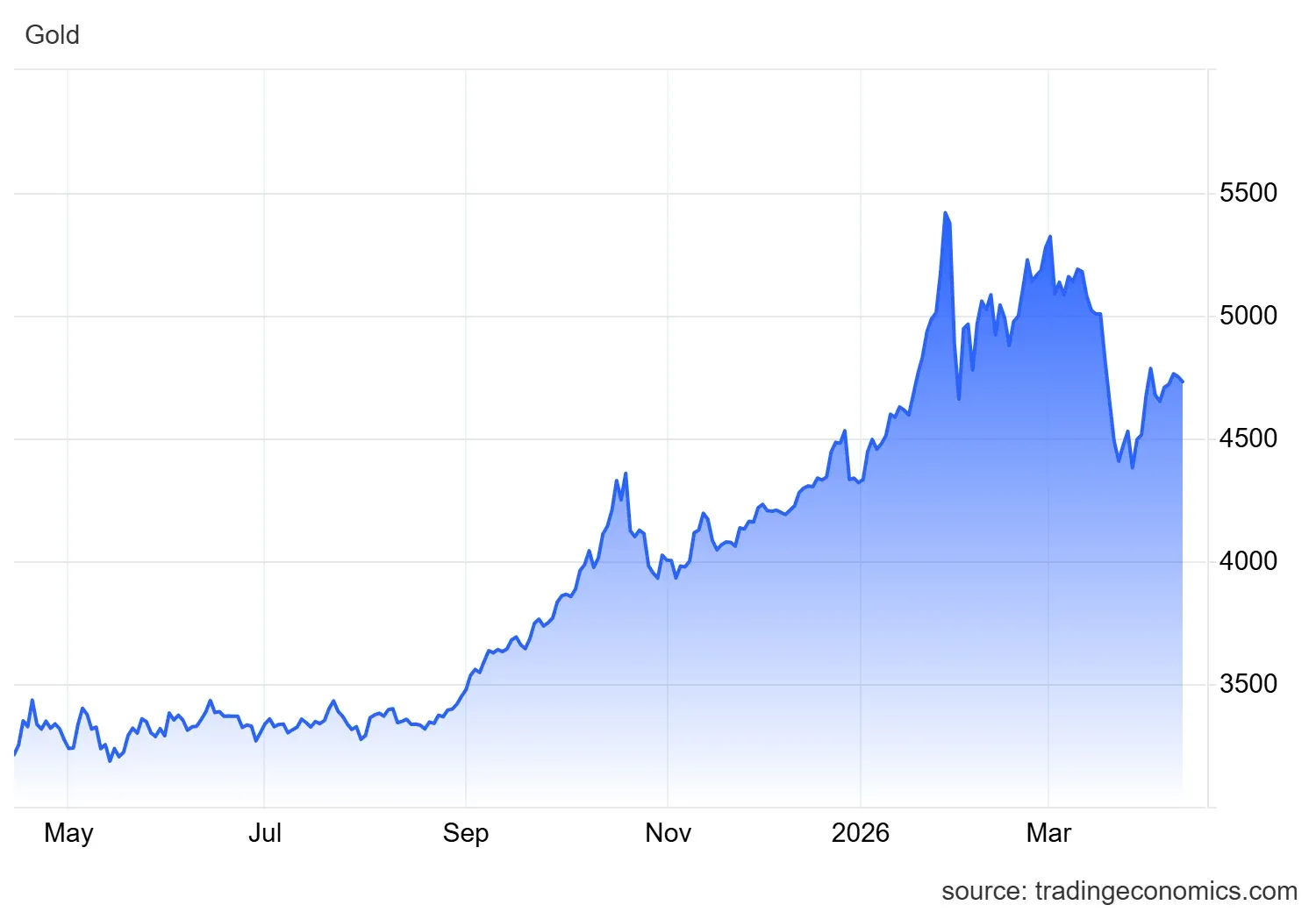

Gold stabilized just below $4,800 per troy ounce, a level that reflects sustained safe-haven demand since the conflict began in late February and isn't likely to reverse quickly with the blockade now in place.

-

Bitcoin closed the week at $73,000, up 9% for the week, benefiting from the same flight-to-alternatives dynamic. Whether that correlation survives a genuine oil supply shock is a different question, crypto hasn't been tested against this kind of macro pressure in a while.

-

The 10-year US Treasury yield edged up 2 basis points to 4.31% on Friday.

-

The euro continued to strengthen against the dollar, with EUR/USD at 1.1728.

One genuinely positive footnote: Ukrainian top negotiator Kyrylo Budanov told Bloomberg on Friday that a Russia-Ukraine peace deal could be within reach in the short term. If that materializes, it would be a meaningful geopolitical shift, though for now, all investor attention is pointed squarely at the Strait of Hormuz.

Conclusion

The failed Iran talks and Trump's Hormuz blockade announcement define the setup for this week. Friday's oil prices are already a relic, expect markets to reprice from the open.

Inflation data confirmed the war's economic cost is spreading beyond energy into the broader consumer basket, and with the ceasefire effectively over, that pressure isn't going away. CoreWeave's back-to-back deals are a real bright spot for AI infrastructure investors, but they're unlikely to offset the risk-off mood that Monday morning brings.

Keep your exposure to energy and defense on the radar. Watch how bond markets respond to any further escalation. And don't let last week's relief rally create a false sense of where things actually stand.

ChartMill Market Desk - Kristoff

This daily update is prepared by ChartMill for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.

Next to read: Breadth Cools, But the Repair Still Holds