The market did what it has done so often lately: it exhaled the moment oil stopped climbing. After a bruising stretch driven by Middle East supply fears, Monday’s session finally brought some relief, with the S&P 500 closing up 1.01% at 6,699.38, the Dow Jones Industrial Average up 0.83% at 46,946.41, and the Nasdaq gaining 1.22% to 22,374.18.

I’d frame it as a tactical rebound rather than a clean all-clear, because the underlying trigger was not suddenly better fundamentals, but a temporary cooling in crude.

The Real Driver Was Oil, Not Optimism

The biggest swing factor was the energy market. WTI crude settled around $93.50 a barrel and Brent around $100.20 after comments from Treasury Secretary Scott Bessent and fresh reporting on a U.S.-led effort to protect tanker traffic through the Strait of Hormuz.

That mattered because the market has been trading as if every extra dollar in oil immediately raises the odds of stickier inflation, fewer Fed cuts, and more pressure on margins. When crude finally backed off, equities responded almost on cue.

I still wouldn’t call this an oil problem that has been solved. Reuters noted that Brent and WTI remain sharply above pre-conflict levels, while the International Energy Agency said member countries could release more reserves if needed after coordinating a historically large stock release.

That tells me policymakers have managed to create a pressure valve, but not yet restore real confidence in the physical flow of supply. As long as Hormuz remains the market’s emotional fault line, energy will keep dictating risk appetite.

AI Was Ready to Run the Moment the Macro Backdrop Softened

Once oil eased, investors moved right back into the part of the market that has repeatedly carried this tape: artificial intelligence.

Nvidia (NVDA | +1.65%) benefited from renewed enthusiasm around Jensen Huang’s GTC keynote, while Meta Platforms (META | +2.24%) drew attention both for its AI spending posture and for reports that it may cut roughly 20% of its workforce.

The message the market seemed to embrace was straightforward: if AI can genuinely unlock productivity gains, investors are willing to tolerate aggressive restructuring in exchange for better margins later.

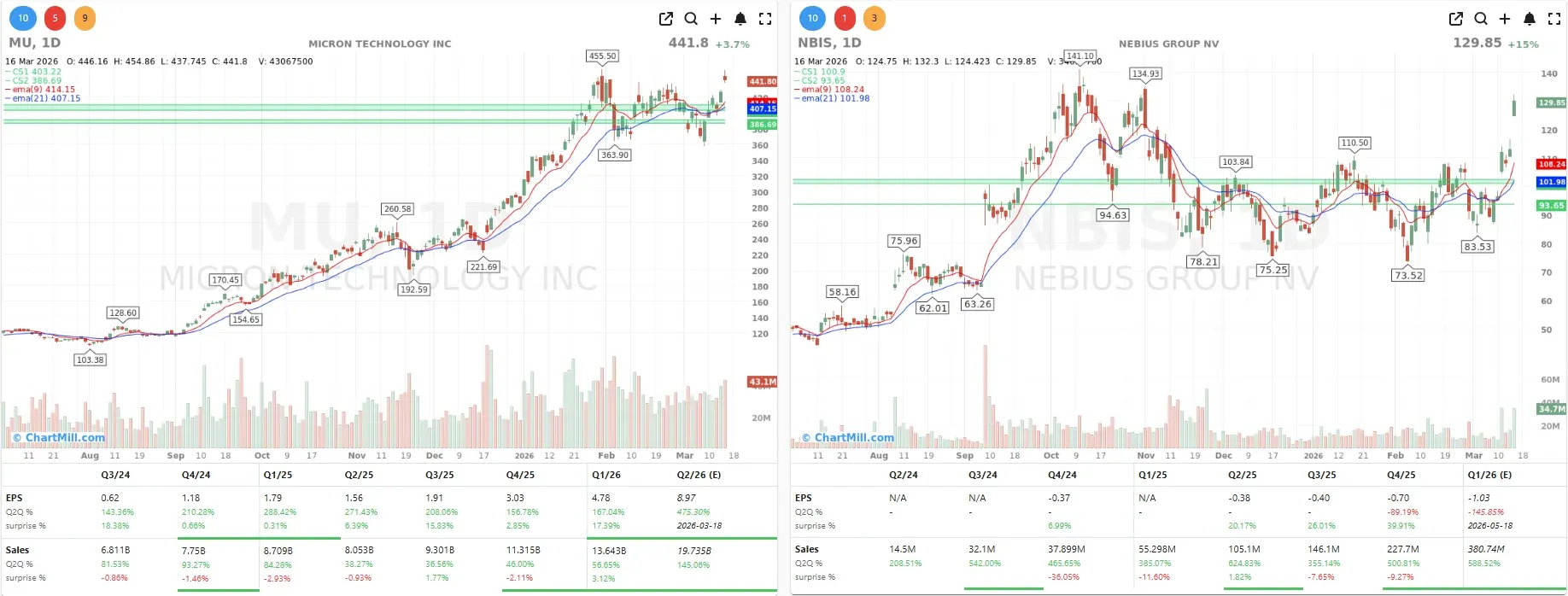

Nebius Group (NBIS | +14.96%) was one of the session’s standout movers after its Meta deal drew fresh attention to the company’s position in AI infrastructure. According to the source material, the agreement could ultimately be worth as much as $27 billion, with Nebius set to provide large volumes of dedicated AI capacity beginning next year.

That kind of number explains why the market did not treat Nebius like a side story. It treated it like a reminder that, even with geopolitics dominating headlines, capital spending around AI compute is still accelerating.

Micron Technology (MU | +3.68%) added to that theme after outlining plans to build a second production facility in Taiwan by the end of 2026. The read-through was broader than Micron alone: investors also pushed up memory and storage names on the idea that the supply chain behind AI remains one of the few areas where spending momentum still looks durable. In a market starved for dependable growth narratives, that continues to matter.

Macro Data Was Mixed, but Good Enough

The economic backdrop did not deliver a major upside surprise, but it also did not get in the way.

The New York Fed’s Empire State manufacturing index slipped to -0.2 in March from 7.1 in February, pointing to a mild contraction, while U.S. industrial production rose modestly in February and homebuilder sentiment improved from very weak levels.

None of that was spectacular, but in the context of a market already on edge about oil and inflation, “not worse” was apparently enough.

Treasury yields also helped. The 10-year yield moved lower toward 4.23%, which gave rate-sensitive equities some breathing space and took a bit of pressure off valuation multiples. That drop in yields, combined with weaker oil on the day, created a much friendlier backdrop for growth stocks than investors had been dealing with late last week.

It was one of those sessions where the macro clouds did not disappear, but they thinned just enough for the market to chase upside again.

Outside the Mega-Cap AI Trade, There Was Plenty of Movement

The rebound was not limited to the usual large-cap tech names.

Dollar Tree (DLTR | +6.42%) moved higher after reporting adjusted quarterly earnings that narrowly beat expectations, even if its near-term outlook stayed soft.

Circle Internet Group (CRCL | +9.06%) gained after a bullish analyst upgrade, while crypto-linked stocks such as Coinbase Global (COIN | +3.98%) and Robinhood Markets (HOOD | +2.62%) were helped by Bitcoin moving back above $74,000. That broader participation matters because it suggests Monday was not just a single-theme bounce. There was at least some willingness to add risk across different corners of the market.

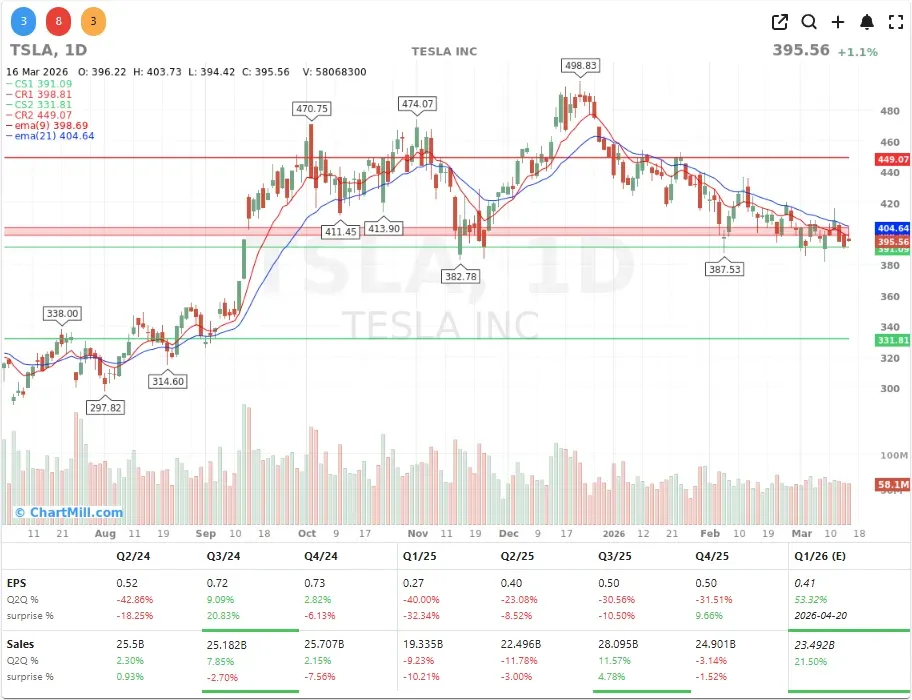

Tesla (TSLA | +1.11%) also joined the advance after Elon Musk said the company’s Terafab chip initiative would launch within a week. I’d still treat that one with some caution.

Investors clearly liked the ambition, but ambition is something Tesla never lacks. Execution is what will determine whether the market keeps rewarding the story. Even so, Monday showed that traders are still very willing to pay for any angle that ties a company more tightly to the AI buildout.

My Take

What stood out to me most is how little it took for investors to re-embrace risk. Lower oil prices were enough to shift the mood from defensive to opportunistic, and the money went straight back into AI, semis, and speculative growth.

That is bullish in one sense, because it shows buyers are still there. But it is also a little uncomfortable, because it shows just how dependent this market remains on a fragile macro variable it cannot control.

Conclusion

Monday’s session was a welcome rebound, but I would not confuse relief with resolution.

Oil eased, yields dipped, and AI leadership reclaimed the spotlight, which was enough to lift the major indexes and improve sentiment. Still, the core market tension remains unchanged: if crude resumes its climb or the geopolitical backdrop worsens, investors will be forced right back into inflation and rate anxiety.

Wall Street got a breather. Whether it gets a lasting trend is another question entirely.

ChartMill Market Desk - Kristoff

This daily update is prepared by ChartMill for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.

Next to read: Market Breadth Rebounds Sharply, But the Broader Damage Is Still Visible