A blockbuster earnings beat from Oracle injected rare optimism into an otherwise jittery session, as escalating conflict in the Strait of Hormuz kept energy markets and investor nerves on edge.

Geopolitics Sets the Tone

Wednesday was another day where the headlines out of the Middle East carried more weight than anything on a balance sheet.

Iran reportedly laid approximately ten sea mines in the Strait of Hormuz over recent days, according to American officials who spoke to The Wall Street Journal, and three ships in the strait are said to have been struck by rockets. With roughly 20% of global oil production passing through that waterway on tankers, markets were understandably on edge.

The oil price reaction was swift. WTI crude in New York surged 4.5% to $87.25 per barrel, while Brent climbed nearly 5% to $91.98 per barrel and that was despite a meaningful attempt by authorities to cool things down. The International Energy Agency announced the release of 400 million barrels from strategic reserves to counteract the price spike. It barely made a dent. The market is clearly pricing in a risk premium that storage releases alone cannot offset.

Diplomatically, there was little comfort either. Remarks from U.S. Defense Secretary Pete Hegseth gave no indication of a desire to de-escalate, while Iran's Revolutionary Guard vowed that no oil would flow to America or its allies through the strait. Iranian tankers, for their part, continue to depart the Gulf, with China as the primary destination, per The Wall Street Journal.

Given all of this, the broader market's relatively contained decline is almost impressive. The Dow Jones fell 0.6%, while the Nasdaq managed a narrow gain of 0.1%. Investors, it seems, are learning to compartmentalize...

Oracle: Proof That AI Spend Can Pay Off

The clear standout of the session was Oracle (ORCL | +9.18%). At a time when AI infrastructure spending has attracted skepticism - is it all capex with no payback? - Oracle delivered a quarterly report that read like a direct rebuttal to that concern.

Q3 revenue came in at $17.2 billion, up 22% year-over-year and ahead of the analyst consensus of $16.9 billion. Non-GAAP EPS of $1.79 also beat expectations of $1.70.

More striking than the headline beat, though, was what's sitting in the pipeline. Oracle's remaining performance obligations - essentially contracted future revenue - reached $553 billion, a 325% increase year-over-year and a $29 billion sequential jump. The overwhelming majority of that growth is tied to large-scale AI contracts.

Cloud revenue, which includes both infrastructure and software as a service, came in at $8.9 billion, up 44% from the prior year. Oracle Cloud Infrastructure (OCI) alone grew 84%. These are not incremental gains, they reflect a genuine acceleration in enterprise adoption of Oracle's AI and cloud platforms.

Management guided for Q4 revenue growth of 19% to 21% in USD, and raised its fiscal 2027 revenue target to $90 billion, a figure that puts Oracle firmly in the conversation alongside the hyperscalers it is increasingly competing with. Crucially, Oracle noted that much of the latest RPO increase came from contracts where the company does not expect to raise additional capital, as equipment is either pre-funded by customers or supplied by them directly.

That detail matters enormously for anyone who has been watching Oracle's balance sheet with concern.

Wall Street responded enthusiastically. JPMorgan upgraded the stock from 'hold' to 'buy' and raised its price target by $20 to $230, citing Oracle's ability to expand revenue while simultaneously growing operating income at double-digit rates. RBC Capital Markets called the results solid and highlighted that management expects to outperform its own targets in fiscal 2027 and beyond.

One internal detail caught my attention: Oracle noted it is now using AI code generation to restructure its product development teams into smaller, more agile groups, building more software in less time and at lower cost.

It's a signal that Oracle is among the first large enterprise software firms to demonstrably use AI to structurally reduce costs. That kind of margin leverage, compounding over time, could be worth far more than any single product launch.

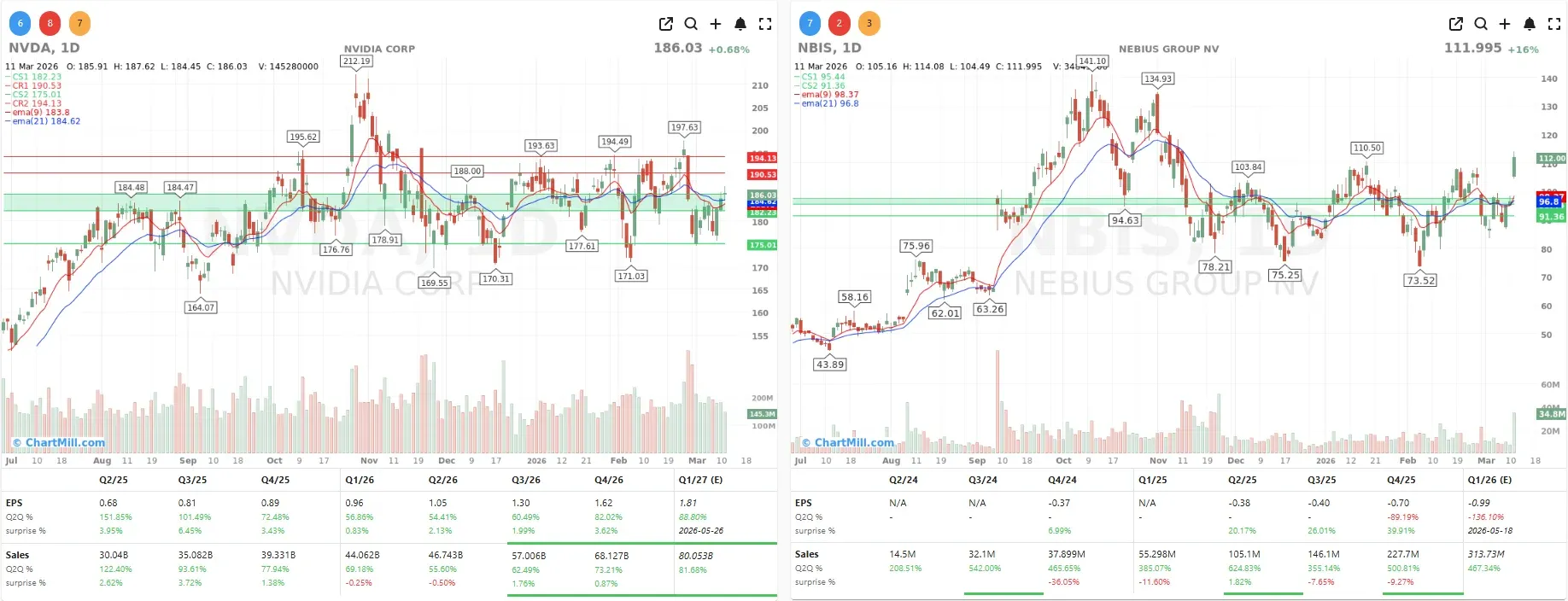

Nvidia Doubles Down on Nebius

If Oracle was the headline, Nvidia (NVDA | +0.68%) and Nebius Group (NBIS | +16.14%) provided a compelling subplot. Nvidia announced a $2 billion strategic investment in Amsterdam-based Nebius Group, aimed at developing next-generation hyperscale cloud infrastructure for the AI market.

As part of the partnership, Nvidia will collaborate with Nebius across the full AI technology stack, from AI factory design and GPU fleet management to inference software and provide early access to next-generation hardware including the Rubin platform, Vera CPUs, and BlueField storage systems. A filing with the SEC confirmed that Nvidia agreed to acquire approximately 8.3% of Nebius at $94.94 per share.

Nebius has also secured approval to construct a 1.2 gigawatt AI factory spanning 400 acres near Independence, Missouri, with power delivery expected in the second half of 2026. To put that in context, that single facility would exceed the total active power capacity of some of Nebius's closest competitors.

For Nvidia, this investment follows a familiar playbook, backing companies that are both customers and validators of its ecosystem. For investors, Nebius is a high-conviction bet on AI infrastructure build-out, though it currently trades at a lofty valuation relative to revenue.

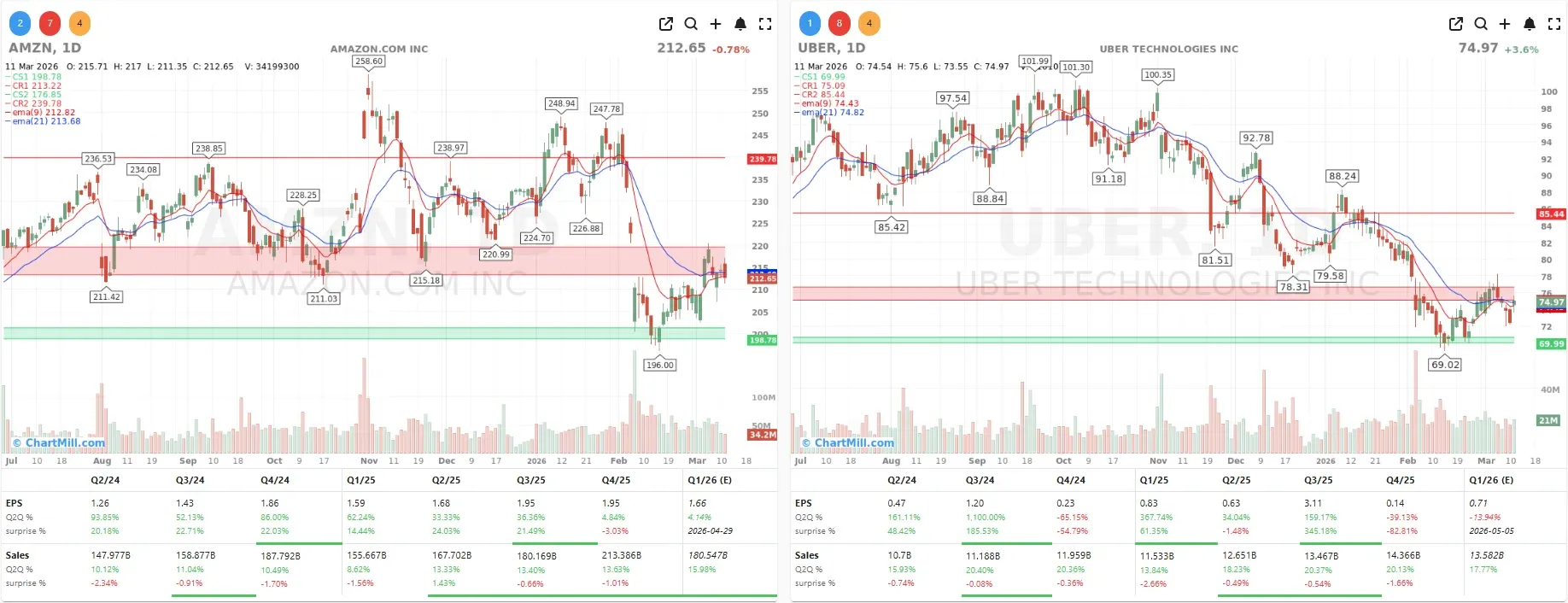

Uber Bets on the Driverless Future

Uber (UBER | +3.61%) climbed on news that will likely generate more column inches over the coming months. Uber and Amazon's (AMZN | -0.78%) Zoox announced a multi-year strategic partnership to deploy Zoox's purpose-built robotaxis on the Uber platform, beginning in Las Vegas this summer and expanding to Los Angeles in mid-2027.

This marks the first time Zoox has entered into a partnership with a third-party platform. It's a meaningful milestone, Zoox has spent years developing its vehicles with inward-facing seats and no steering wheel or pedals, and the Uber integration provides the commercial distribution that could finally accelerate scale. Zoox has already logged more than one million autonomous miles and transported over 300,000 riders.

Uber CEO Dara Khosrowshahi has argued that autonomous vehicles on Uber's platform achieve significantly higher utilization than on standalone platforms, with trips per vehicle per day running approximately 30% higher through Uber. That's a compelling economic argument for AV companies considering where to deploy their fleets and it strengthens Uber's case as the aggregator of choice in this space.

Other Movers Worth Noting

-

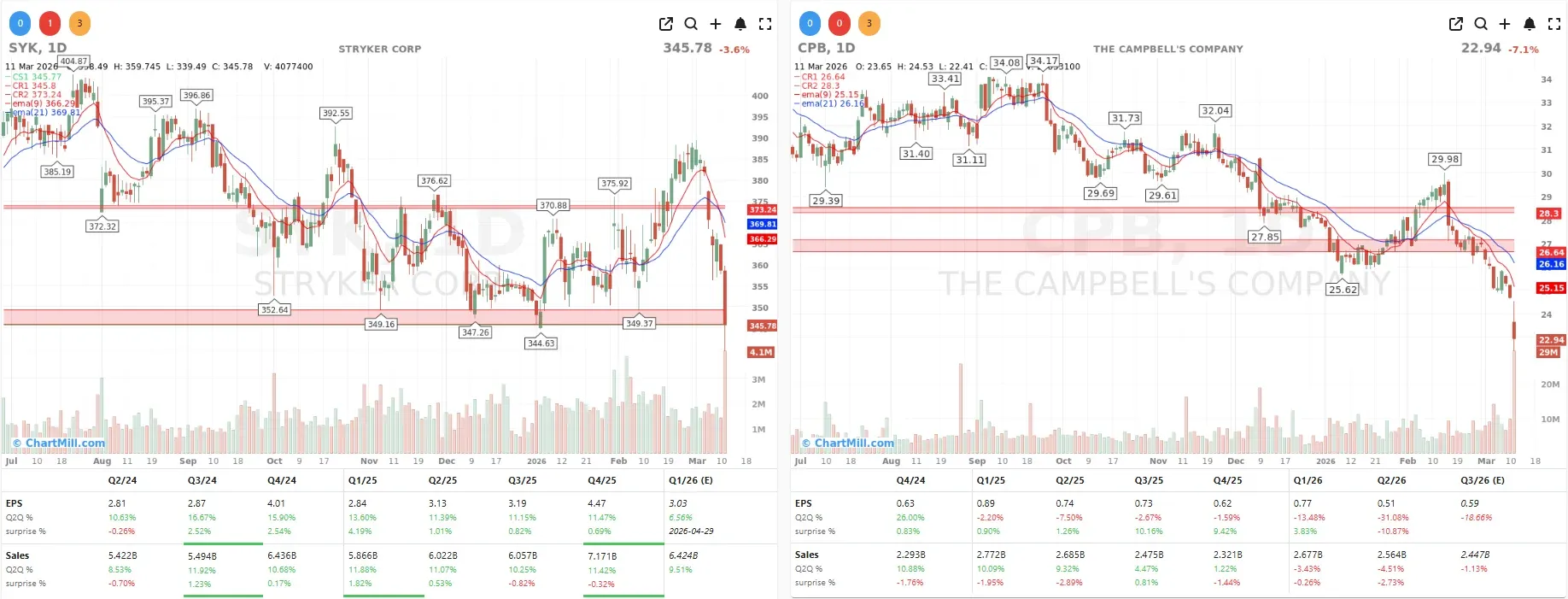

Campbell's (CPB | -7.05%) had a rough session after reporting second-quarter adjusted EPS below expectations. CEO Mick Beekhuizen cited disappointing performance in the Snacks segment and weather-related supply disruptions as the primary culprits. Nothing systemic, but the market punished it all the same.

-

Stryker (SYK | -3.59%) suffered a global systems outage, and according to The Wall Street Journal, the login page of the medical technology company was defaced with a logo linked to an Iran-affiliated hacking group, a stark reminder that geopolitical conflict has a cyber dimension that extends well beyond the oil patch.

-

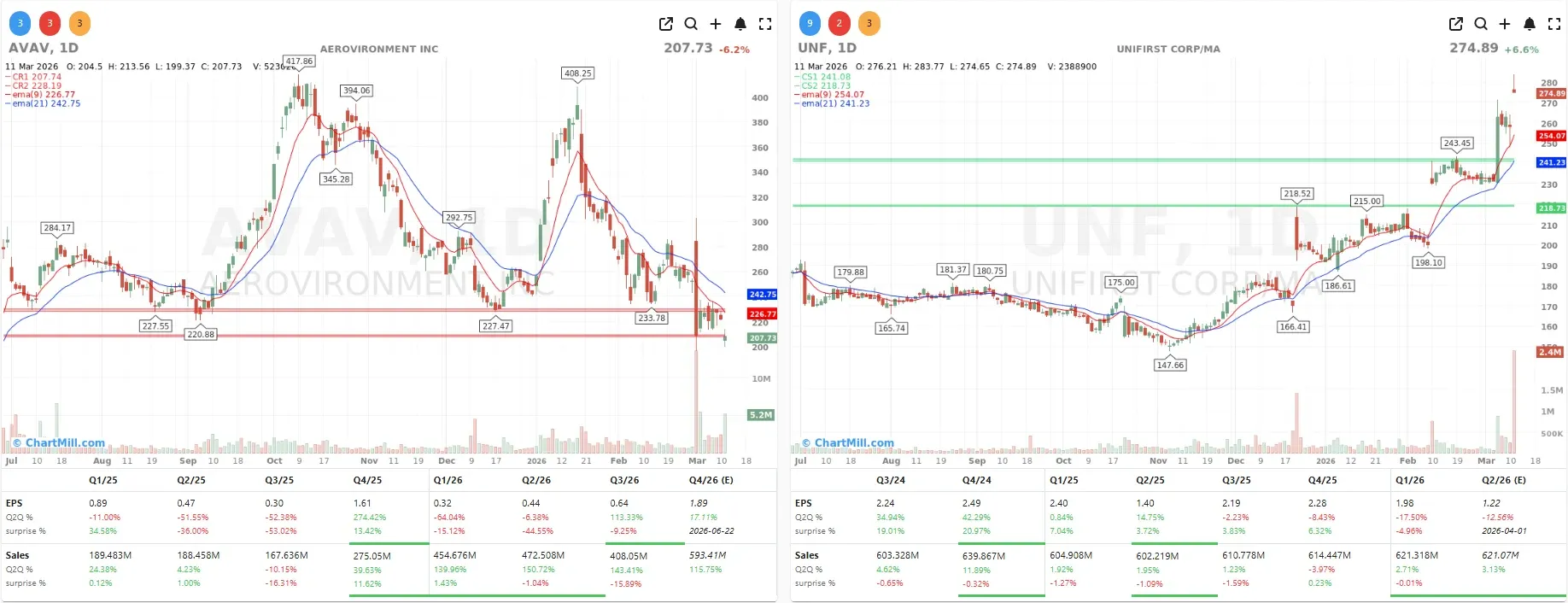

UniFirst (UNF | +6.58%) rallied after rival Cintas (CTAS | +1.05%) made a $5.5 billion acquisition bid, a premium that investors in UniFirst clearly welcomed.

-

AeroVironment (AVAV | -6.25%) disappointed with its third-quarter adjusted earnings and trimmed its full-year outlook — an unexpected stumble for a drone manufacturer that, on paper, should benefit from the current geopolitical environment.

Macro Snapshot

On the economic data front, U.S. inflation came in at 2.4% in February, unchanged from January. Under normal circumstances, a stable inflation reading would command attention. Right now, as one analyst noted, investors are largely looking past the data given how rapidly geopolitical developments are unfolding.

The euro/dollar pair was trading around 1.1570, and rising U.S. ten-year Treasury yields weighed modestly on gold and silver prices.

OPEC maintained its demand growth forecast of 1.4 million barrels per day.

Conclusion

Wednesday's session offered a useful contrast: one company - Oracle - demonstrating in concrete financial terms that the AI investment cycle can produce real earnings, while the broader market wrestled with an oil shock that no earnings beat can fully neutralize.

The Hormuz situation is the variable that could unravel a lot of careful analysis very quickly. For now, markets are holding up, but the risk premium in energy is real and deserves a prominent spot in any portfolio review.

The Oracle results, meanwhile, should give confidence to investors in the broader AI infrastructure trade, the demand is there, the contracts are signed, and the revenue is coming through.

ChartMill Market Desk

This daily update is prepared by ChartMill for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.

Next to read: Market Breadth Deteriorates Further as Participation Keeps Narrowing