If there's one thing markets taught us again on Wednesday, it's that geopolitics can rattle the cage for a day or two, but when the economic data cooperates, buyers don't stay sidelined for long.

After Tuesday's volatile session that shaved roughly 1% off the major averages amid escalating tensions following the US–Israel military offensive against Iran, Wednesday saw a decisive recovery. The Dow Jones gained 0.5% to close at 48,739, while the tech-heavy Nasdaq surged 1.3% to 22,807.

ISM Services Data Hands Bulls a Gift

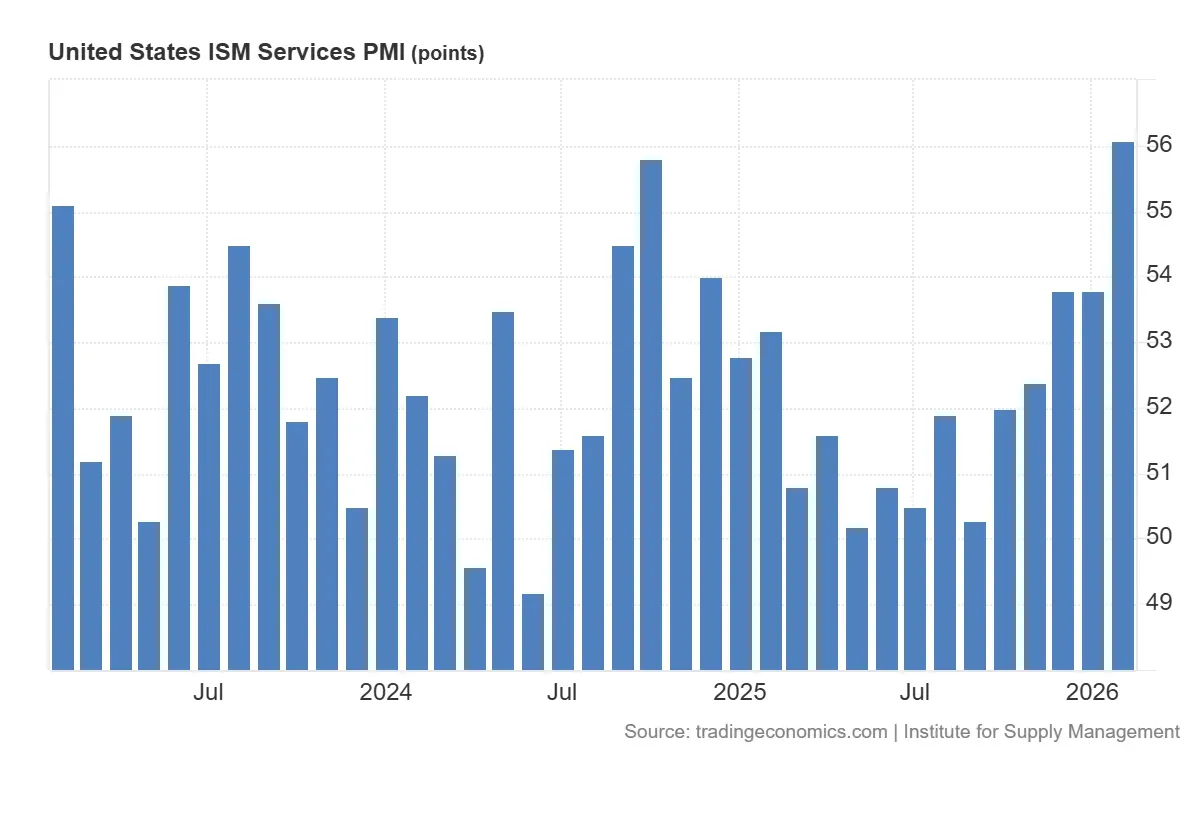

The single most important catalyst for Wednesday's bounce was the ISM Non-Manufacturing index. February's reading came in at 56.1, up sharply from January's 53.8 and well above the consensus estimate of 53.5.

For context, any reading above 50 signals expansion, so 56.1 is comfortably in growth territory. Even more encouraging: the prices sub-index came in below expectations, hinting that services inflation isn't spiraling out of control. That combination - solid growth, contained inflation - is exactly the "Goldilocks" narrative that underpins the bull case for equities. It doesn't erase the geopolitical risk premium on energy, but it does give investors reason to look past it.

The ISM reading essentially handed bulls a permission slip, grow fast, keep prices in check, and the Fed stays patient. That's about as good as it gets.

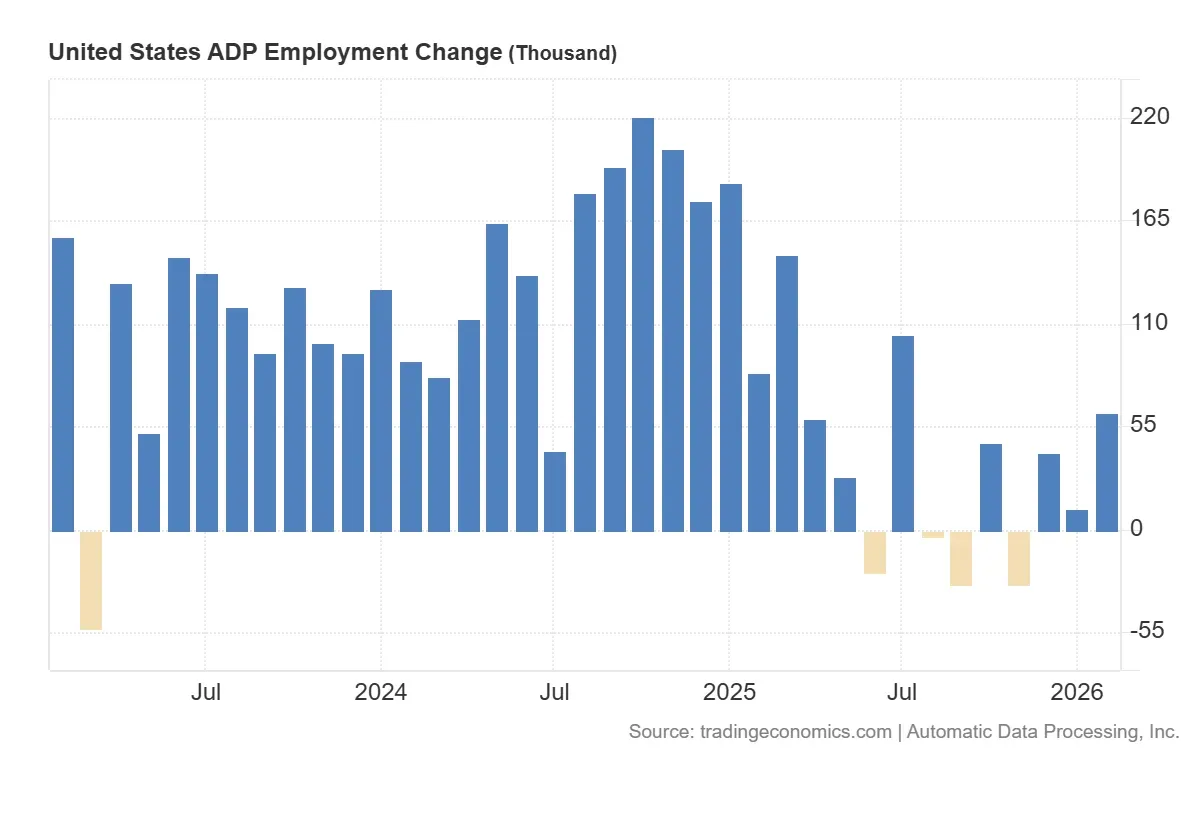

The ADP private payrolls report added a second layer of reassurance. Private employers added 63,000 jobs in February against a forecast of just 48,000, with wages rising 4.5% year-over-year. Solid, but not the kind of red-hot reading that would panic bond markets. All eyes now shift to Friday's official non-farm payrolls — expect volatility if the number surprises sharply in either direction.

Memory Chips and Mega-Caps: The AI Trade Refuses to Die

Semiconductor stocks were the unambiguous stars of the session.

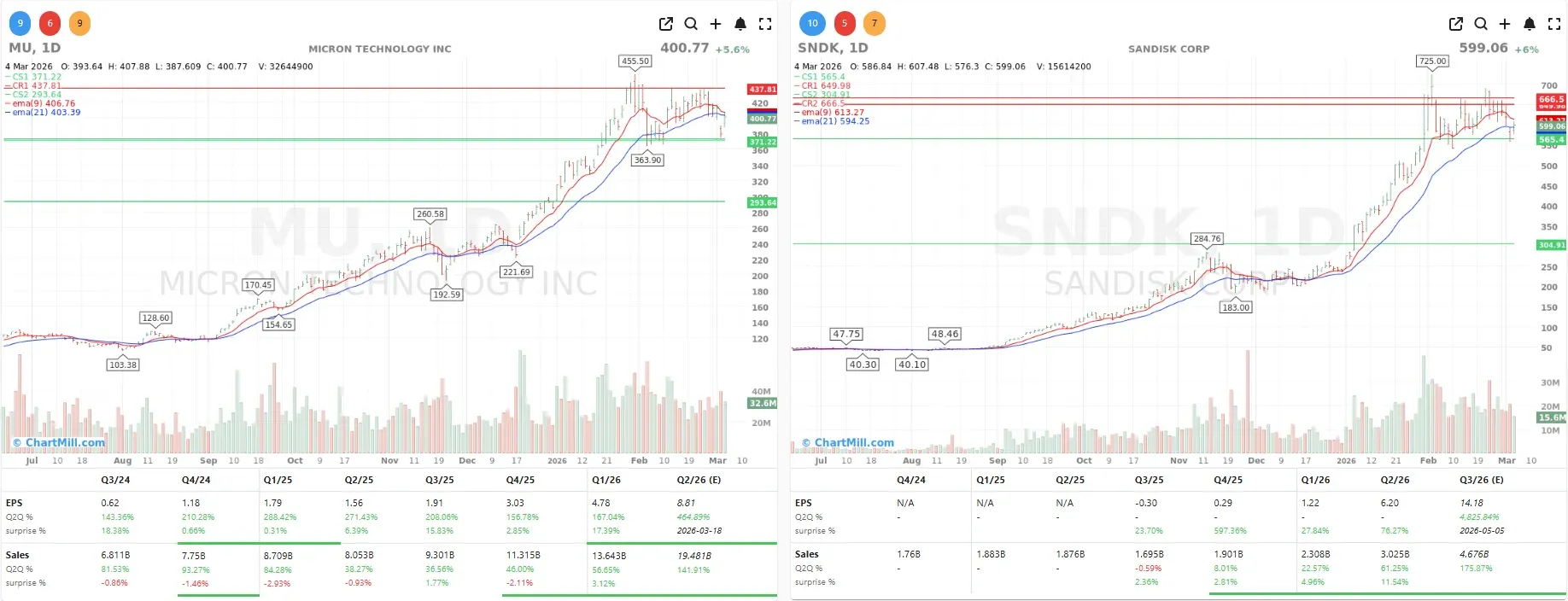

Memory chipmakers led the way: Micron Technology MU | +5.55% and SanDisk SNDK | +5.95% continued to attract strong buying interest as investors remain enthusiastic about the structural shortage in memory chips, a direct consequence of the insatiable demand for AI data center buildout.

Micron has now gained roughly 27% since January 1st, and I think there's a reasonable case that this is more than just momentum. The underlying demand driver - trillion-dollar AI infrastructure investment - isn't reversing anytime soon.

The megacap tech names piled in too.

Nvidia NVDA | +1.66% gained during the regular session, assisted by a Reuters report that CEO Jensen Huang hinted the company may pull back from its $30 billion OpenAI investment should the AI lab proceed with its planned IPO. That's a notable signal of where Nvidia sees its capital allocation priorities.

Amazon AMZN | +3.88% and Meta Platforms META | +1.93% also charged higher by 1–4%, collectively confirming that large-cap tech remains the sector of choice when risk appetite returns.

Broadcom: The After-Hours Story That Sets the Tone

The real headline of the day may well be what happened after the closing bell.

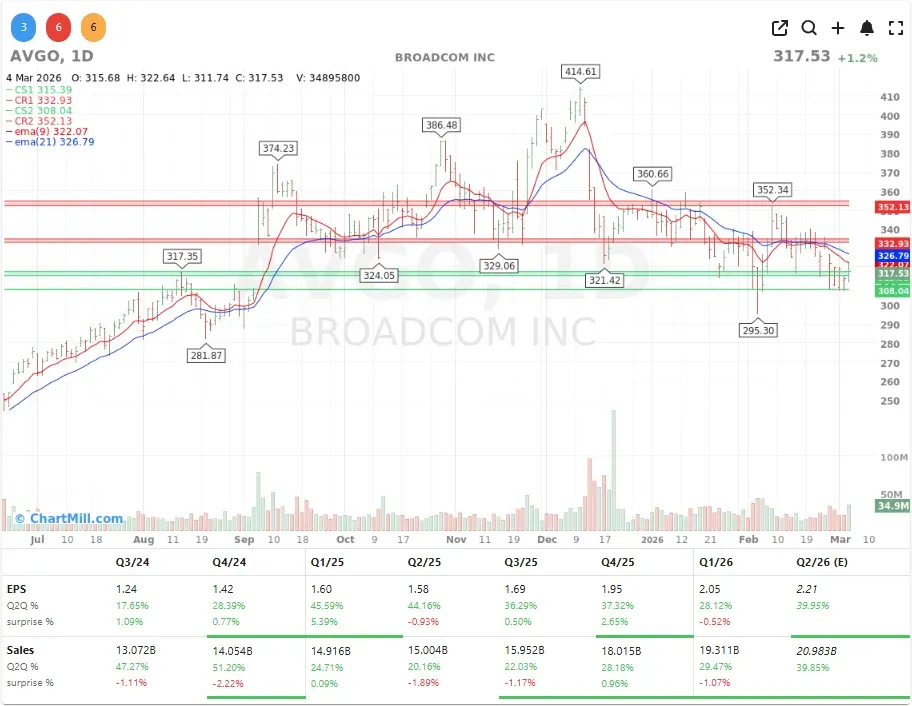

Broadcom AVGO | +1.18% released its fiscal Q1 2026 results (November–January period), and the numbers were hard to argue with. Revenue came in at $19.3 billion, in line with estimates, but the earnings beat caught attention: EPS of $2.05 versus the $2.03 consensus.

More importantly, Broadcom guided Q2 revenue at approximately $22 billion, a significant step up from the $20.5 billion analysts had modeled. AI-specific revenue is expected to climb to $10.7 billion, again above expectations. To cap it off, the company announced a $10 billion share buyback program through end of 2026.

Read our full Q1 - 2026 update here

Moderna's $950M Deal Clears a Major Overhang

Away from chips, the day's most dramatic individual move belonged to Moderna MRNA | +15.99%. The biotech agreed to pay $950 million to settle all worldwide patent disputes with Arbutus Biopharma and Genevant Sciences over the lipid nanoparticle (LNP) delivery technology that underpins its COVID-19 vaccine.

Critically, the settlement structure means Moderna pays no ongoing royalties on current or future vaccines. That is a meaningful removal of legal uncertainty, the kind of overhang that can quietly suppress a stock's multiple for years. At 16% in a single session, the market's verdict on that clarity is pretty unambiguous.

CrowdStrike Delivers; Abercrombie Disappoints

Cybersecurity firm CrowdStrike CRWD | +4.15% added 4% after reporting strong Q4 results. Revenue reached $1.31 billion, and the company posted its first-ever positive GAAP net income, a maturity milestone that analysts took positively.

Given the geopolitical backdrop with heightened state-level cyber threats during the Iran conflict, demand for enterprise cybersecurity is likely to remain structurally elevated.

On the other end of the spectrum, Abercrombie & Fitch ANF | -3.6% paid the price for a cautious outlook.

While Q4 same-currency revenue growth of 5% wasn't bad, CEO Fran Horowitz's 2025 guidance of just 1–3% growth came in well below the 4.5% analyst consensus.

Throw in margin compression worries - the full-year operating margin is expected to dip slightly to 12–12.5% from 12.5% - and you have a recipe for disappointment. Import tariffs are clearly adding a layer of cost uncertainty that management is reluctant to gloss over.

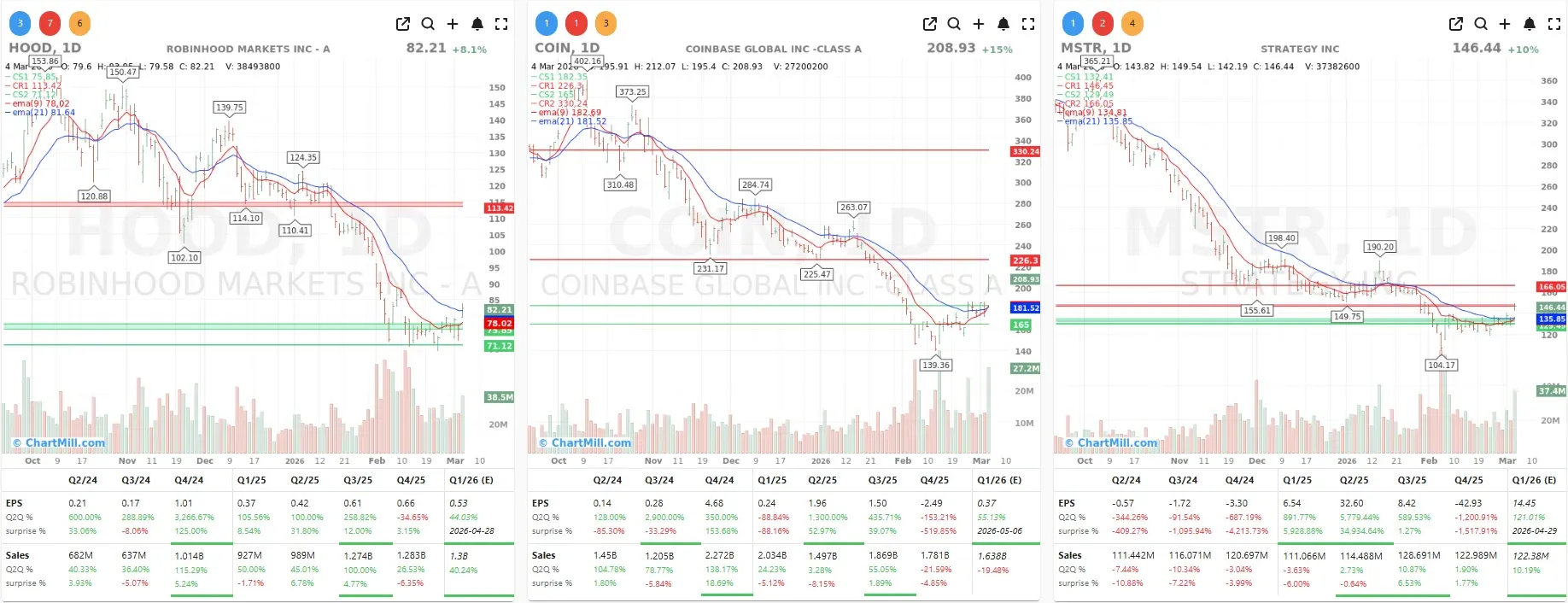

Crypto Surges on Clarity Act Optimism

Wednesday's session also delivered a sharp crypto-driven rally in exchange and fintech names.

Following a social media post by President Trump emphasizing the urgency of passing the Clarity Act - which establishes a regulatory framework for the crypto industry and interlocks with the already-passed Genius Act for stablecoins - Bitcoin surged 7%.

The spillover into listed crypto proxies was swift: Coinbase COIN | +14.57% exploded 14.6%, Strategy MSTR | +10.37% gained 10%, and Robinhood HOOD | +8.07% added 8%.

Macro Backdrop: Iran, Hormuz, and a New Fed Chair

The Iran conflict continues to cast a shadow, even if markets shook it off on Wednesday. The US confirmed sinking Iranian naval vessels, and an Iranian minister reportedly reached out through back channels to the CIA to discuss ceasefire terms.

Analysts at Sparta Commodities remain cautious, noting that elevated energy prices reflect lingering doubts about whether the US Navy can keep the Strait of Hormuz fully open for Gulf oil tankers. Brent crude settled near $81.40 and WTI around $74.66, elevated but stable on the day. President Trump confirmed that US warships will escort oil tankers if needed.

On the monetary policy front, Trump formally nominated Kevin Warsh as the next Federal Reserve Chair, to succeed Jerome Powell when his term expires in May. Warsh, a former Fed Governor, is viewed by some as more hawkish than Powell, a nomination that could matter enormously if inflation pressures from energy costs and tariffs persist into mid-year. The Senate must still confirm the nomination.

Speaking of tariffs: Treasury Secretary Scott Bessent signaled Wednesday that the global import tariff rate would likely rise to 15% this week, up from the 10% baseline implemented on February 4th, after courts struck down several sector-specific levies. The euro/dollar pair was trading at 1.1639 on the news.

The Bottom Line

Wednesday was a textbook example of the market's selective memory: one strong ISM print and a compelling ADP report were enough to push the geopolitical noise to the background. The real story is the after-hours Broadcom beat, which should reinforce confidence in the AI infrastructure spending cycle heading into Thursday.

With Friday's payrolls report looming and the Iran situation far from resolved, I wouldn't get too comfortable with the rally just yet. But for investors with exposure to quality semiconductor names and crypto-adjacent equities, Wednesday offered a useful reminder that the underlying themes remain intact.

Stay disciplined, watch the Hormuz headlines, and keep an eye on how the market digests Broadcom's guidance in Thursday's session.

ChartMill Market Desk

This daily update is prepared by ChartMill for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.

Next to read: Breadth Bounces, But the Damage Isn’t Repaired Yet