For investors aiming to find possible opportunities in the market, a disciplined method frequently includes searching for companies that seem to be trading for less than their inherent worth. One typical plan is to filter for stocks that have a mix of good valuation measures together with firm basic business qualities. This approach seeks to sidestep the "value trap", a stock that is inexpensive for a cause, by confirming the company is also fiscally sound, profitable, and able to expand. By concentrating on stocks with a good valuation rating while keeping acceptable ratings in other important categories, investors can create a list of companies that might be briefly priced too low by the market.

A recent filter using this "acceptable value" method has pointed to Adobe Inc. (NASDAQ:ADBE) as a candidate deserving more detailed inspection. As a worldwide frontrunner in digital media and marketing software, Adobe's business is firmly fixed in the processes of creatives and businesses globally. The company's basic report implies it might presently present an interesting blend of sensible price and firm operational soundness.

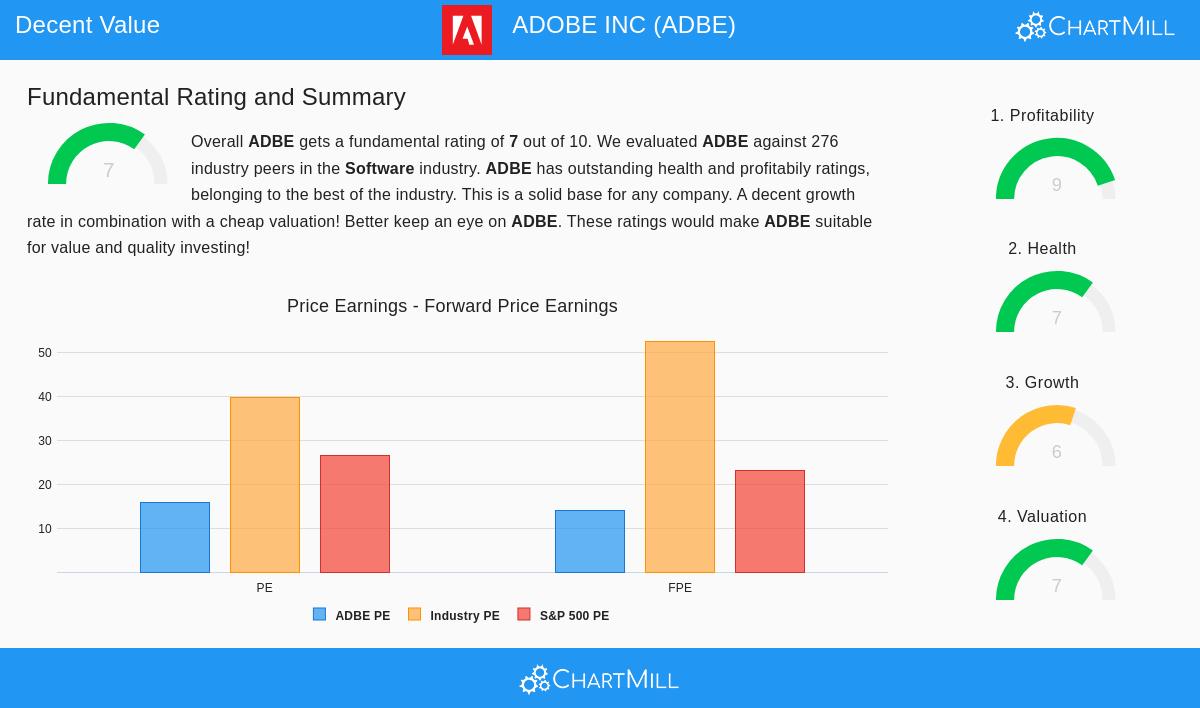

Valuation: A Relative Discount in Software

The central idea of value investing is buying a dollar's worth of assets for fifty cents. For Adobe, the valuation measures show the market might be pricing the company cautiously compared to both its field and its own caliber.

- Price-to-Earnings (P/E) Ratio: At 15.91, Adobe's P/E ratio is viewed as "correct" but rests noticeably under the field average. The report says that 79% of its software field competitors are valued more highly on this measure. Also, it trades for less than the wider S&P 500, which has an average P/E of 26.60.

- Forward P/E and Cash Flow: The view stays positive. With a forward P/E of 13.91, Adobe costs less than 83% of its field. Its Price-to-Free Cash Flow ratio is also good, rating better than 86% of rivals.

- Growth Compensation: While the standard P/E is low, the company's anticipated earnings growth of almost 13% each year is included in its PEG ratio, which shows a fair valuation. The report mentions that Adobe's superior profitability might even support a higher multiple.

This valuation view is key for the plan because it spots a possible mismatch: a high-caliber, field-leading business is not getting a premium price. This difference between market price and seen inherent worth is the beginning place for value investors.

Financial Health: A Firm Base

An inexpensive stock is only a sound investment if the company is fiscally stable. Adobe's health score of 7 out of 10 shows a mostly strong balance sheet with some detailed points.

- Solvency is Superior: The company's Altman-Z score of 8.61 shows no bankruptcy danger and does better than 86% of the field. Importantly, its Return on Invested Capital (ROIC) of 36.51% is much higher than its cost of capital, meaning it is producing major shareholder value.

- Controlled Debt: Adobe's Debt-to-Equity ratio of 0.53 shows some use of debt financing, rating poorer than two-thirds of its peers. However, the report gives key detail: the total amount of debt is very low. Its Debt to Free Cash Flow ratio of 0.63 is superior, meaning it could clear all debt in under eight months using its present cash flow.

- Liquidity Measures: The current and quick ratios are both at 1.00, which is lower than many peers and implies a strict working capital situation. However, the basic examination finds that given Adobe's better profitability and solvency, these ratios do not always signal near-term liquidity problems for a business of its type.

For a value plan, this health check is important. It verifies that the low valuation is not because of a worsening balance sheet or fiscal trouble, lowering the danger of a value trap.

Profitability: Top-Tier Results

Adobe's notable basic feature is its profitability, which gets a top score of 9. This is the driver that creates inherent value.

- Superior Returns: The company produces excellent returns on its assets (24.17%) and equity (61.34%), doing better than over 97% of the software field. Its ROIC of 36.51% is not only among the best but has also been rising.

- Strong Margins: Adobe works with top-tier margins. Its Gross Margin of 89.27% and Operating Margin of 36.63% show strong pricing ability and efficient operations, doing better than 96% and 95% of the field, in that order. While the net profit margin has fallen a little, it stays very firm at 30%.

This degree of profitability is a key filter in the "acceptable value" filter. A very profitable company trading at a sensible valuation is often more interesting than a barely profitable company trading at a large discount, as it signals a lasting competitive edge.

Growth: An Established But Consistent Path

With a growth score of 6, Adobe is not a very high-growth story but shows dependable, above-average increase.

- Firm Past Record: Over the last year and five-year average, Adobe has given double-digit growth in both Earnings Per Share (13.74% and 15.87%) and Revenue (10.53% and 13.06%).

- Maintainable Future View: Experts think this pace will continue, though at a somewhat slower rate, with future EPS and revenue growth estimated near 10% and 8% each year. The report mentions that while the growth rate is slowing from past peaks, it stays "quite firm."

For value-focused investors, this outline is often perfect. It suggests the company has moved past its most unstable growth time into a phase of established, foreseeable increase, which can be simpler to value and often has less speculative excess in the share price.

Conclusion

The "acceptable value" filter that found Adobe Inc. looked for stocks where good valuation meets basic quality. Adobe's situation is interesting: it trades for less than its field and the wider market even though having top-tier profitability, a fiscally sound operation, and a steady growth outline. This mix implies the market might be pricing too low a software franchise with a wide moat and consistent cash production. It represents the value investor's aim of finding a high-caliber business at a fair or improved price.

Interested in examining other stocks that match this outline? You can use the same "Acceptable Value" filter used to find Adobe to find more possible opportunities. View the filter and results here.

For a full breakdown of all the measures talked about, you can see Adobe's complete basic examination report.

Disclaimer: This article is for information only and does not form financial guidance, a suggestion to buy or sell any security, or a support of any investment plan. Investors should do their own study and think about their personal fiscal situation and risk comfort before making any investment choices.