For investors looking for reliable income, a disciplined screening process is needed to separate strong dividend payers from possible value traps. One useful method uses filters for stocks that have a high dividend rating and also show good basic profitability and financial condition. This method tries to find companies able to maintain and possibly raise their payments over time, not those with high yields because of a worsening business or share price. A stock that recently appeared from this kind of screen is UNITED PARCEL SERVICE-CL B (NYSE:UPS), a global logistics leader whose basic profile deserves attention from income-focused investors.

Dividend Profile: A Notable Yield with a Dependable History

The foundation of any dividend investment is the income it provides, and UPS makes a notable case here. The company’s present dividend yield is a main point of interest.

- Notable Yield: With a yearly dividend yield of 6.79%, UPS provides a large income stream. This number is much higher than both the industry average of about 1.17% and the wider S&P 500 average of near 1.89%.

- Good Growth History: Maybe more important than the present yield is the steadiness of its growth. UPS has raised its dividend at an average yearly rate of 10.10% over the last five years, showing a clear commitment to giving capital back to shareholders. The company has a dependable history, having paid and not cut its dividend for at least ten years.

- A Point on Sustainability: While the yield and growth history are notable, a key measure needs watching. The company’s payout ratio, the part of earnings paid as dividends, is presently high at 96.88%. This shows that almost all its trailing twelve-month earnings are being paid out, which could reduce financial room if earnings see pressure. However, it is seen that the dividend is growing at a rate nearly matching earnings growth, which, if kept, would help the sustainability of future raises.

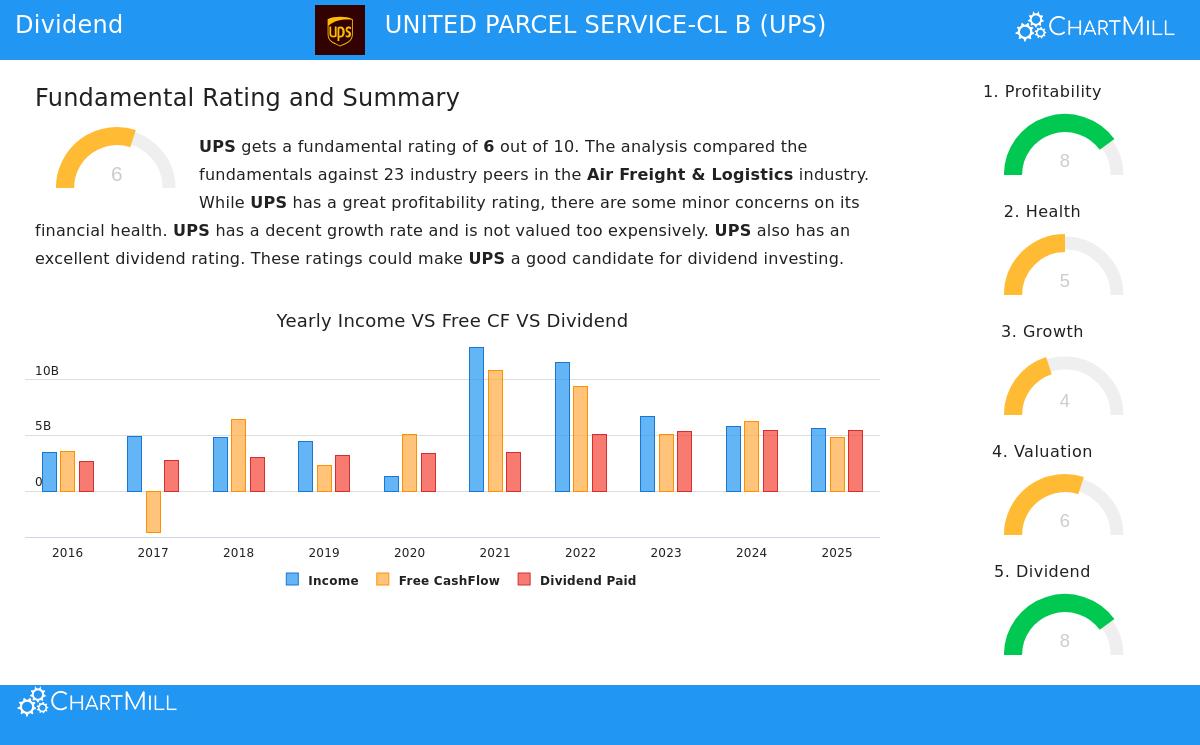

Profitability and Health: The Base for Payments

A high dividend is only as good as the business behind it. The screening rules of acceptable profitability and health are key because they check the company’s ability to create the cash required to pay those dividends. UPS’s scores in these areas give background for its dividend strength.

Profitability Strength: UPS gets a solid ChartMill Profitability Rating of 8 out of 10. The company is regularly profitable with good cash flow from operations. Main efficiency measures are industry-best:

- A Return on Equity (ROE) of 34.34% is better than 95% of similar companies in the Air Freight & Logistics industry.

- Its Profit Margin of 6.28% and Operating Margin of 8.91% also sit in the top group of the industry.

This high level of profitability is what funds dividend payments and share buybacks, which UPS has also been doing.

Financial Health Points: The company gets a ChartMill Health Rating of 5, pointing to an average but steady financial state. There are different signs:

- Good Points: UPS creates value, as its Return on Invested Capital is above its cost of capital. The company has also been lowering its share count over recent years.

- Points to Watch: The balance sheet holds a noticeable amount of debt, with a Debt/Equity ratio of 1.45. While this is normal in capital-heavy industries, it needs watching. Also, liquidity ratios (Current and Quick Ratio) are enough for meeting near-term duties but are below many industry peers.

For dividend investors, this health profile suggests the company is not in trouble, but the high payout ratio together with its debt level shows the need for steady future earnings to keep its financial balance and dividend policy.

Valuation and Growth Setting

From a valuation view, UPS seems fairly priced, which is a good sign for investors thinking about a new position. The stock trades at a Price/Earnings (P/E) ratio of 13.75, which costs less than 91% of its industry peers and under the S&P 500 average. This valuation, combined with its high yield, presents a good "value and income" case.

Growth has been difficult lately, with small drops in both Earnings Per Share and Revenue over the past year. However, analyst forecasts point to a pickup, with EPS expected to grow over 10% yearly in the next few years. This expected recovery is key, as it would help ease pressure from the high payout ratio and aid continued dividend growth.

Is UPS a Dividend Stock to Think About?

UNITED PARCEL SERVICE-CL B presents a detailed case for dividend investors. It offers a high, well-supported yield backed by a ten-year history of dependable and growing payments, all supported by a basically profitable and settled global business. The high payout ratio and moderate financial health rating are not warning signs alone but are important factors that highlight the company’s need to return to earnings growth as analysts forecast.

For investors using a plan that focuses on sustainable income, UPS fits the main rules of high dividend quality paired with acceptable profitability. The stock acts as a clear example of the kind of chance a planned screening process can find. A closer look at the company’s full basic analysis is in its detailed ChartMill report.

Find More Dividend Ideas The study of UPS came from a planned screen for high-quality dividend payers. This method can be used to find a wider set of possible income investments. You can view the present results of this "Best Dividend Stocks" screen and change the filters to fit your own rules by using this link.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer to buy or sell any security. Investors should do their own study and think about their personal financial situation before making any investment choices.