For investors looking for steady income, a systematic way to choose dividend stocks is important. One useful method involves looking for companies that provide a good dividend and also show the basic financial soundness to maintain and possibly raise those payments over time. This requires considering more than just a high yield and assessing a company's earnings and general financial condition. A stock that performs favorably in these areas could be a more durable income-producing investment, particularly during volatile market periods.

Travel + Leisure Co. (NYSE:TNL), a notable company in the hospitality and vacation ownership industry, recently appeared from this careful review process. The company's basic financial picture indicates it deserves further examination by investors focused on dividends. The main point of interest is its even performance across important measures for long-term dividend continuity.

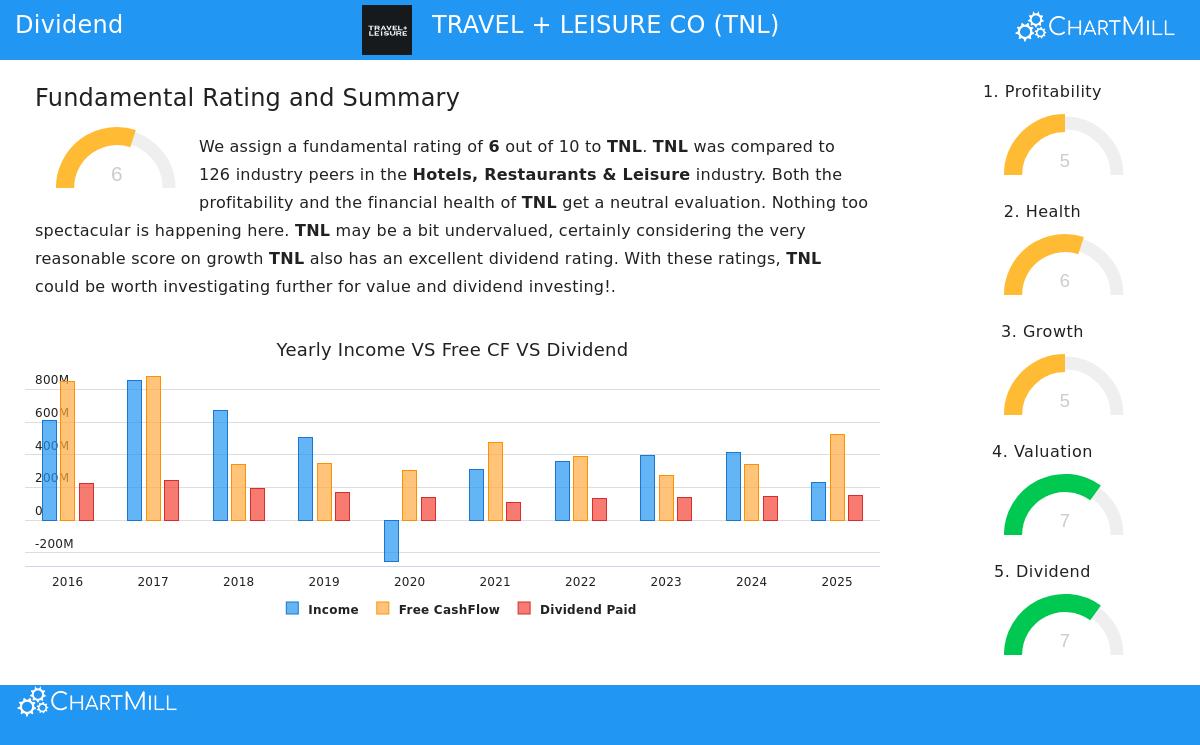

Dividend Profile: A Steady Payer with Potential for Increase

The main draw for income investors is the dividend. Travel + Leisure Co. makes a strong argument based on present income and a record of consistency.

- Good and Higher-Than-Average Yield: The company's present dividend yield is 3.55%. This is a satisfactory yield by itself, but it is more interesting when compared. It is much higher than the average yield of similar companies (1.14%) and also above the present yield of the wider S&P 500.

- History of Increase: Consistency is vital in dividend investing. TNL has paid dividends for at least ten years, creating a reliable history. Significantly, it has regularly raised its payout, reaching a notable yearly dividend growth rate of 7.61% over the last five years.

- Increase Viability: A key test for any rising dividend is if the company's profits can maintain it. For TNL, its earnings per share (EPS) have risen quicker than its dividend. This difference shows the dividend growth is paid for by real business growth, not by an unmanageable rise in the payout ratio, which is good for future raises.

Supporting Basics: Earnings and Financial Condition

A high dividend score needs a solid business base. This is where the review standards for "acceptable profitability and condition" show their value, and TNL satisfies these tests.

Earnings Supply the Support The company's profitability figures, while not extraordinary, are good and supply the needed profits to finance shareholder returns. Its operating margin of 14.47% is better than many rivals, showing efficient main business activities. Also, it has reliably reported positive profits and operating cash flow over the past five years. This reliable profitability is what allows steady dividend payments.

Financial Condition Supplies Security For dividend continuity, a company must manage its debts without difficulty. TNL's financial condition score shows a varied but sufficient situation, with specific good points in cash availability:

- Good Cash Position: The company shows very good short-term financial room. Its current ratio of 3.51 and quick ratio of 2.64 are some of the best in its field, meaning it has enough resources to cover short-term debts.

- Controlled Debt: The assessment points to a high debt-to-free-cash-flow ratio, which is an item to watch. However, it is similar to many industry rivals, and notably, the company has been working to lower its debt-to-assets ratio and repurchase shares, both steps that can improve shareholder value over time.

Price and Expansion: An Extra Positive

While the main goal is income, the total investment argument is improved by TNL's price and expansion outlook. The stock seems fairly valued, with a P/E ratio of 11.2 and a forward P/E of 9.8, making it less expensive than most of its industry rivals and the wider market. This implies the present dividend yield is not due to a high stock price. Also, the company is projected to keep a good EPS growth rate in the low double digits, supporting the chance for ongoing dividend growth.

For a full look at all these basic factors, you can see the entire ChartMill Fundamental Analysis Report for TNL.

Conclusion

Travel + Leisure Co. stands out as a noteworthy option for dividend investors because it meets a multi-part review method. It provides a higher-than-average yield supported by a ten-year history of payments and regular growth. Importantly, this dividend is backed by acceptable profitability from its main vacation ownership and exchange operations and a good cash position that supplies financial security. The method of checking for condition and profitability helps find companies less prone to reduce their dividend during economic slowdowns, and TNL's picture matches this defensive purpose. When joined with a fair valuation, the stock makes an argument for being a core part of an income-focused portfolio.

Interested in finding other stocks that match this careful dividend investment method? You can use the same "Best Dividend" screen that found TNL to find more possible ideas here.

Disclaimer: This article is for information only and is not financial advice, a suggestion to buy or sell any security, or a support of any investment plan. Investors should do their own research and think about their personal financial situation and risk comfort before making any investment choices. Past results do not guarantee future outcomes.