For investors looking for steady income, a methodical screening process is important. One useful technique focuses on companies that provide a good dividend and also have the basic financial soundness to maintain and possibly raise those payments. This method focuses on a high ChartMill Dividend Rating, which looks at yield, growth, and sustainability, while also setting minimum scores for earnings power and balance sheet condition. This multi-step method aids in finding stocks where a good yield is backed by a solid business, instead of indicating trouble.

Travel + Leisure Co (NYSE:TNL) results from this kind of screen, making a strong case for dividend investors. The company, a leading name in vacation ownership and travel services, works in a field focused on consumer leisure and experiences.

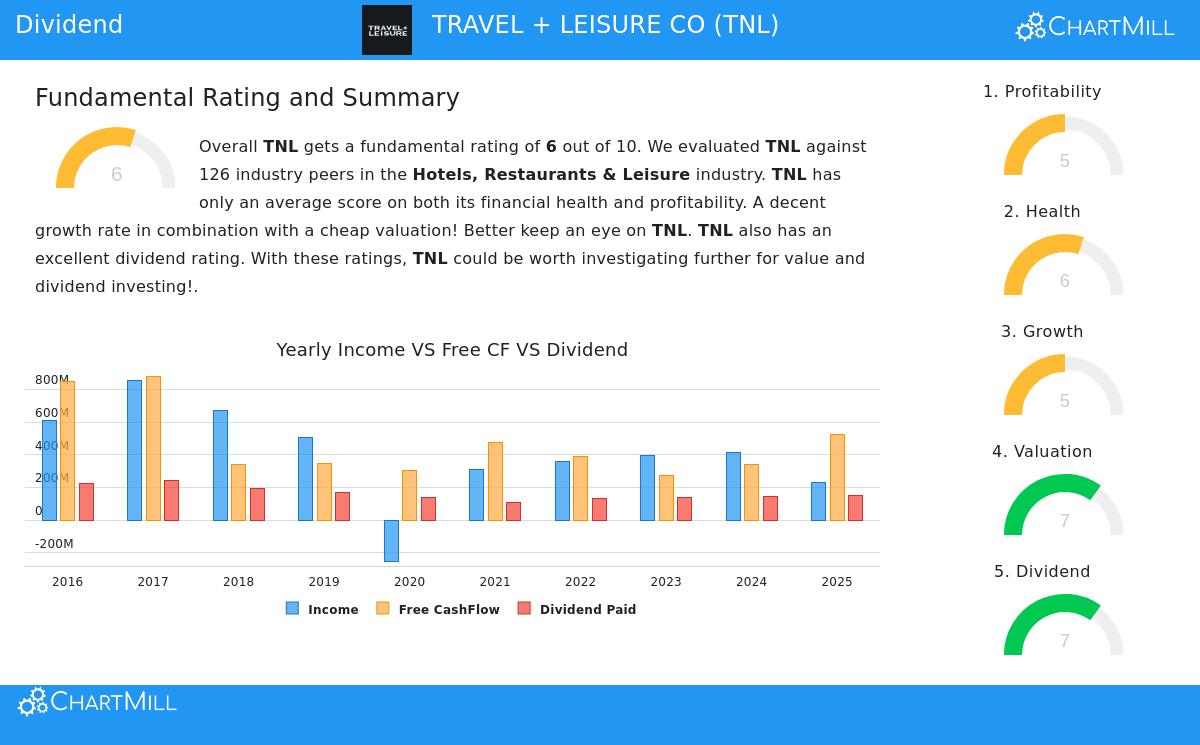

Dividend Profile: A Steady and Increasing Payout

The main attraction of TNL for income investors is its dividend profile, which earns a good 7 out of 10 in the ChartMill rating system. This score shows a mix of yield, past consistency, and growth potential.

- Good Yield: The stock now provides a yearly dividend yield of 2.97%. This is higher than the industry average of 1.10% and also above the present S&P 500 average yield of about 1.82%. For investors, this means more immediate income compared to similar companies and the wider market.

- History of Increase: Consistency is important in dividend investing. TNL has paid dividends for at least ten years, creating a reliable history. Also, the company has regularly increased its payout, with a good yearly dividend growth rate of 7.61% over the last five years. This increase helps counter inflation and raises the investor's income on their initial investment over time.

- Sustainability Factors: A vital check for any dividend stock is the payout ratio. TNL pays roughly 64.5% of its earnings as dividends. While this is above a cautious level and shows the dividend uses a notable part of profit, it is balanced by a good pattern: the company's earnings are increasing quicker than the dividend. This situation implies the present payout level is workable and the growth path can continue, if earnings keep rising.

Supporting Basics: Earnings Power and Balance Sheet Condition

A high dividend yield can sometimes be misleading if the company's basics are weakening. The screen's standards of adequate earnings power and condition are made to prevent this issue. TNL's scores in these areas give important background for its dividend appeal.

Earnings Power (Rating: 5/10): The company shows steady profit from operations. It has been profitable every year for the past five years and has produced positive operating cash flow each year in that time. Important margins are good; its operating margin of 14.47% is better than about two-thirds of its industry competitors and has been improving. While the overall earnings power rating is middling, the consistency and cash flow creation are good signs that the business can pay for its dividend.

Balance Sheet Condition (Rating: 6/10): TNL's financial condition rating shows a stable, though not outstanding, balance sheet. The company's advantage is clear in its liquidity. With a Current Ratio of 3.51 and a Quick Ratio of 2.64, TNL has a solid ability to meet its near-term debts, doing better than over 90% of its industry rivals. This strong liquidity offers a cushion for ongoing dividend payments during possible economic slowdowns or seasonal cash changes.

Regarding long-term debt, the situation is average. The company has a notable amount of debt, shown by a debt-to-free-cash-flow ratio of 10.72 years. However, this amount is typical for the industry. The Altman-Z score, a gauge of bankruptcy chance, is acceptable at 2.30, showing little near-term chance and putting the company in the stronger part of its industry.

Price and Growth Background

From a price standpoint, TNL seems fairly valued, which helps the dividend investment case. Its Price-to-Earnings (P/E) ratio of 11.18 and Forward P/E of 9.78 are viewed as low compared to both the S&P 500 and most of its industry peers. This valuation hints the market may not completely account for the company's income-producing ability or its growth.

Regarding growth, TNL has shown a solid past revenue growth rate of over 13% on average each year. While future revenue growth is predicted to slow, earnings per share are forecast to keep increasing at a good rate near 12% each year. This expected earnings growth is the basic driver that can support future dividend raises.

A Candidate for More Study

Travel + Leisure Co stands for the kind of stock a methodical dividend screening process tries to find: one with a better-than-average and rising yield, supported by a profitable operation and a financially sound base. The company's solid liquidity, good margins, and fair price add reasons for confidence for an income-focused investor.

For investors wanting to examine other companies that meet similar standards of high dividend quality, adequate earnings power, and balance sheet condition, the fully set "Best Dividend Stocks" screen is a good beginning point for more study. You can also see the detailed ChartMill Fundamental Analysis Report for TNL for a full look at all ratings and measures.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. The analysis is based on current data and ratings, which are subject to change. Investors should conduct their own thorough research and consider their individual financial situation and risk tolerance before making any investment decisions.