For investors looking for a dependable source of passive income, a methodical screening process is important. One useful tactic is to look for companies that provide an appealing dividend and also have the fundamental financial soundness to maintain and possibly increase those payments. This method focuses on quality and longevity rather than pursuing the largest available yield, which can sometimes indicate company trouble. A practical technique is to use a multi-factor screen that finds stocks with good dividend ratings while also demanding reasonable scores in profitability and financial condition. This aids in finding companies where the dividend is backed by a solid business operation, not supported by high debt or temporary earnings.

One company that appears from this kind of methodical screen is The Timken Company (NYSE:TKR), a worldwide maker of engineered bearings and industrial motion products. For investors focused on dividends, Timken offers an interesting example of balanced, quality income creation.

Dividend Dependability and Longevity

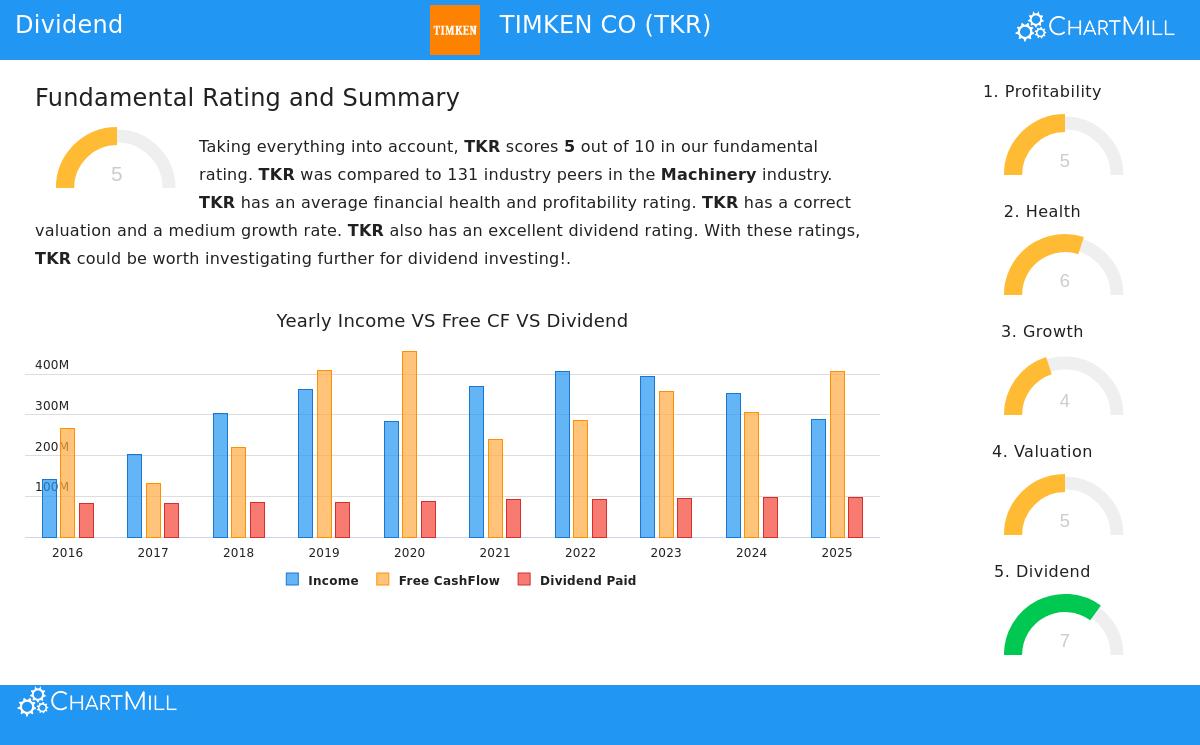

The foundation of any dividend investment idea rests on the payment's dependability and possibility for increase. Timken performs solidly here, receiving a good ChartMill Dividend Rating of 7 out of 10. This rating combines several important elements dividend investors need to examine.

- History: Timken has built a dependable record, having paid a dividend for at least 10 straight years without a cut. This steadiness across different economic periods is a sign of dividend reliability.

- Maintainable Payment: The company's payout ratio, the part of earnings given as dividends, is a low 34.08%. This conservative figure shows that only around one-third of profits are given to shareholders. This safety margin means the dividend is easily supported and leaves significant money for the company to put back into its operations, reduce debt, or handle short-term challenges without putting the payment at risk.

- Increase and Yield: While its present dividend yield of 1.44% is moderate next to some high-yield stocks, it is useful to see this in comparison. The yield is better than the average for other companies in its machinery industry. Also, the dividend has increased at a yearly rate of about 4.13% over the last five years, and importantly, analysts think future earnings growth will be faster than this dividend growth. This link is important for making sure future raises stay maintainable.

Supporting Business Basics: Profitability and Financial Condition

A good dividend cannot stand alone; it must be supported by a profitable and financially stable company. This is exactly why looking for acceptable profitability and condition ratings is a key step in the method. Timken's business basics give this needed support.

The company gets a neutral but satisfactory ChartMill Profitability Rating of 5. Important measures show a business that performs adequately:

- An operating margin of 13.53% is good, doing better than many others in its industry.

- The company has recorded positive earnings and operating cash flow in every one of the past five years, showing basic earning ability.

Maybe more important for long-term dividend safety is financial condition, where Timken gets a rating of 6. The balance sheet displays clear positives:

- Good Liquidity: A current ratio of 2.82 and a quick ratio of 1.47 show the company has sufficient short-term assets to cover its short-term debts, giving protection from operational issues.

- Controlled Debt: With a debt-to-equity ratio of 0.59, the company employs a reasonable amount of debt. While this ratio is larger than some similar companies, it is offset by good cash flow creation. The company's debt-to-free-cash-flow ratio of 4.73 matches the industry, indicating a feasible schedule for debt payment.

Price and Growth Setting

For investors thinking about a purchase price, valuation is important. Timken seems fairly valued in its sector. Its forward P/E ratio of 16.70 is lower than both the wider S&P 500 average and most of its industry peers. Also, its enterprise value-to-EBITDA ratio indicates a somewhat low valuation compared to the industry.

Regarding growth, the situation is varied but indicates an upward direction. While recent year-over-year earnings per share (EPS) had a small decrease, the five-year pattern shows slight growth. More significantly, analysts forecast EPS to rise by over 12% each year in the next few years. If this growth happens, it would create a firmer base for future dividend raises and possibly help share price growth along with the income.

A Choice for Quality Income

The Timken Company shows the kind of stock a methodical dividend screening process tries to find. It is not the biggest yielder available, but it offers a balanced combination: a dependable and well-supported dividend with a history of increase, supported by a profitable operation and a financially sound balance sheet. For investors creating a portfolio aimed at lasting income, such traits are frequently more important than a large but uncertain yield.

For investors wanting to examine other companies that fit similar standards of good dividend quality, acceptable profitability, and stable financial condition, you can see the complete screen results here: Best Dividend Stocks Screen.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The analysis is based on current data and past performance, which is not indicative of future results. Investors should conduct their own research and consult with a qualified financial advisor before making any investment decisions.