Two days in a row of green closes and yet Thursday's session felt nothing like celebration. The Dow Jones and the Nasdaq extended Wednesday's relief rally, but the gains were narrow, the mood was cautious, and half the market was quietly bleeding.

The Rundown

- Wall Street closed higher for a second consecutive day, carried by news of planned Israel-Lebanon talks and easing oil prices, but the ceasefire remains fragile

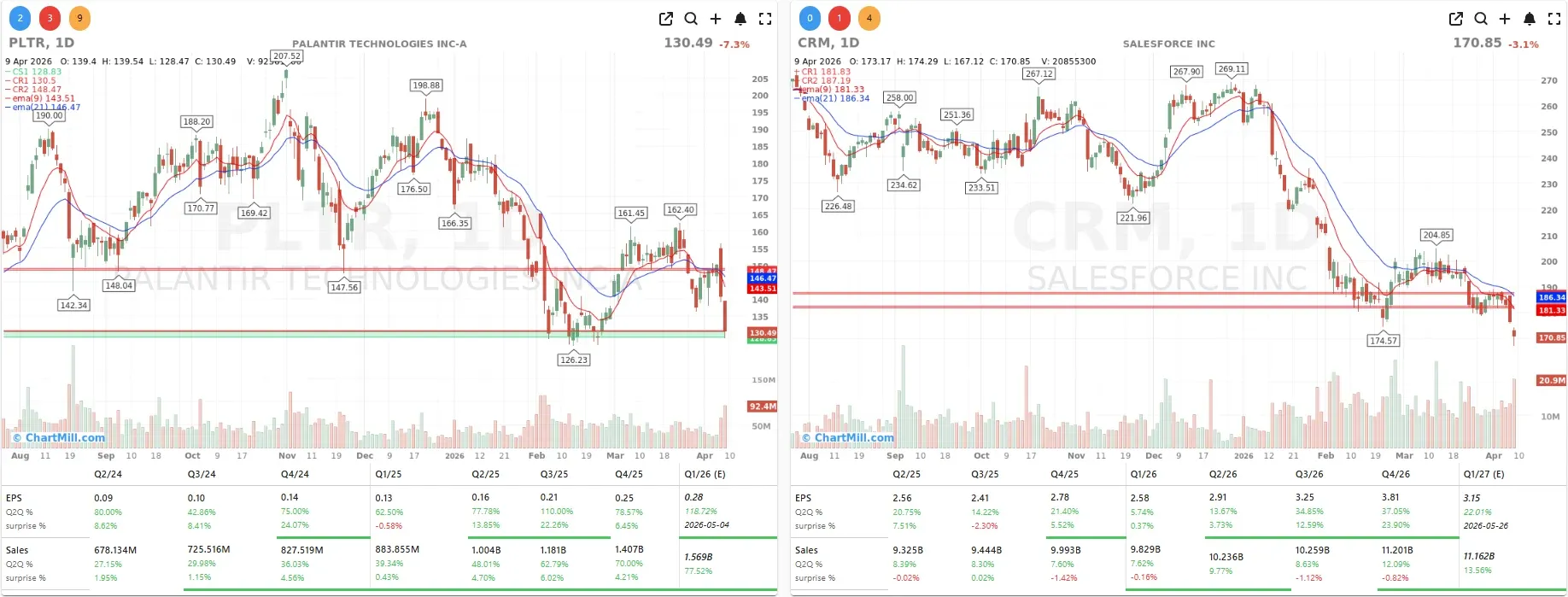

- The software sector was gutted again, with the S&P 500 Application Software subindex dropping 5%, as AI disruption fears showed no sign of letting up

- Amazon revealed $15B+ in annualized AI cloud revenue, the first hard number from the hyperscaler capex cycle

- Friday's US CPI print for March is the next critical test: inflation is expected to jump sharply, and the Fed's next move depends on what comes in

The Ceasefire Is Holding. Barely.

The US-Iran truce that sent markets soaring on Wednesday is still in place, but the word "fragile" doesn't quite capture it.

Iran continues to threaten closure of the Strait of Hormuz, tanker traffic through the strait is running well below pre-conflict levels, and fighting in southern Lebanon, which falls outside the terms of the US-Iran ceasefire, hasn't stopped.

What calmed oil markets on Thursday was a single Axios report: Israel and Lebanon will hold direct talks in Washington next week. That was enough to push Brent crude from near $100 a barrel back down to around $95. WTI settled at approximately $98.

"We've advised investors to account for the risk of renewed escalation and to diversify with quality bonds, gold, and broad commodities," said Ulrike Hoffmann-Burchardi, global head of equities at UBS Global Wealth Management. That's the kind of measured language that actually says quite a lot. It's an acknowledgement that the situation isn't resolved, just paused.

An American delegation is also expected to travel to Pakistan later this week for a first round of direct talks with Iran. Whether that leads somewhere or goes nowhere, it's at least movement, and markets are pricing it accordingly.

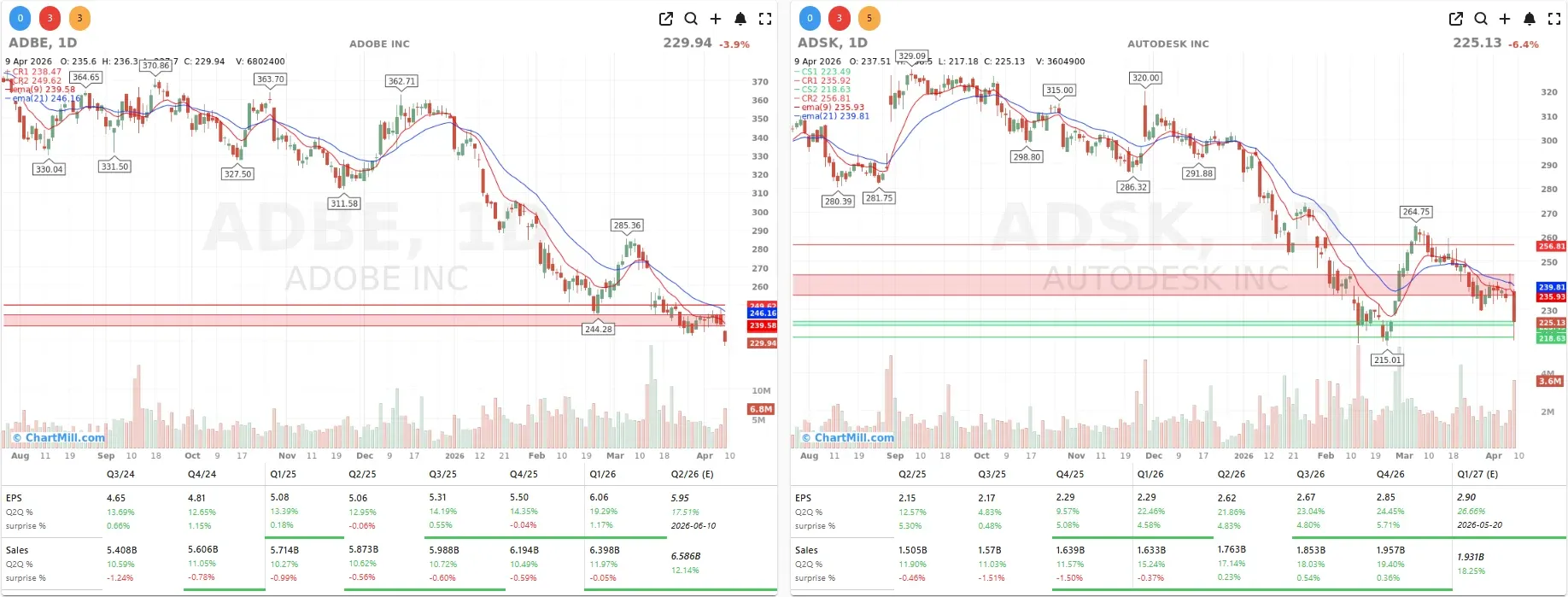

Software Takes Another Hit

If you want to understand what's really happening beneath the surface of this market, the software sector is telling you more than the index levels are.

AutoDesk (ADSK | ▼6.45%), Adobe (ADBE | ▼3.92%), Salesforce (CRM | ▼3.13%), and Palantir (PLTR | ▼7.30%) all took significant hits.

The common thread isn't a bad earnings report or a guidance cut. It's something more structural: the market is starting to reprice the competitive position of established enterprise software against a new generation of AI-native platforms.

Michael Burry, the man who shorted the housing market before the 2008 crisis and became the subject of The Big Short, added fuel to the fire on Thursday.

In a post that circulated widely, he argued that Anthropic is eating Palantir's lunch. His logic: Anthropic's annualized recurring revenue has reportedly jumped from $9 billion to $30 billion, partly because businesses are finding it cheaper, easier, and more intuitive than legacy enterprise AI solutions.

Palantir holds government contracts, he concedes, but those are small and come with thin margins.

It's a credible argument, and the timing is pointed. Anthropic launched "Claude Managed Agents" this week, a platform designed to let companies build and deploy autonomous AI systems at scale.

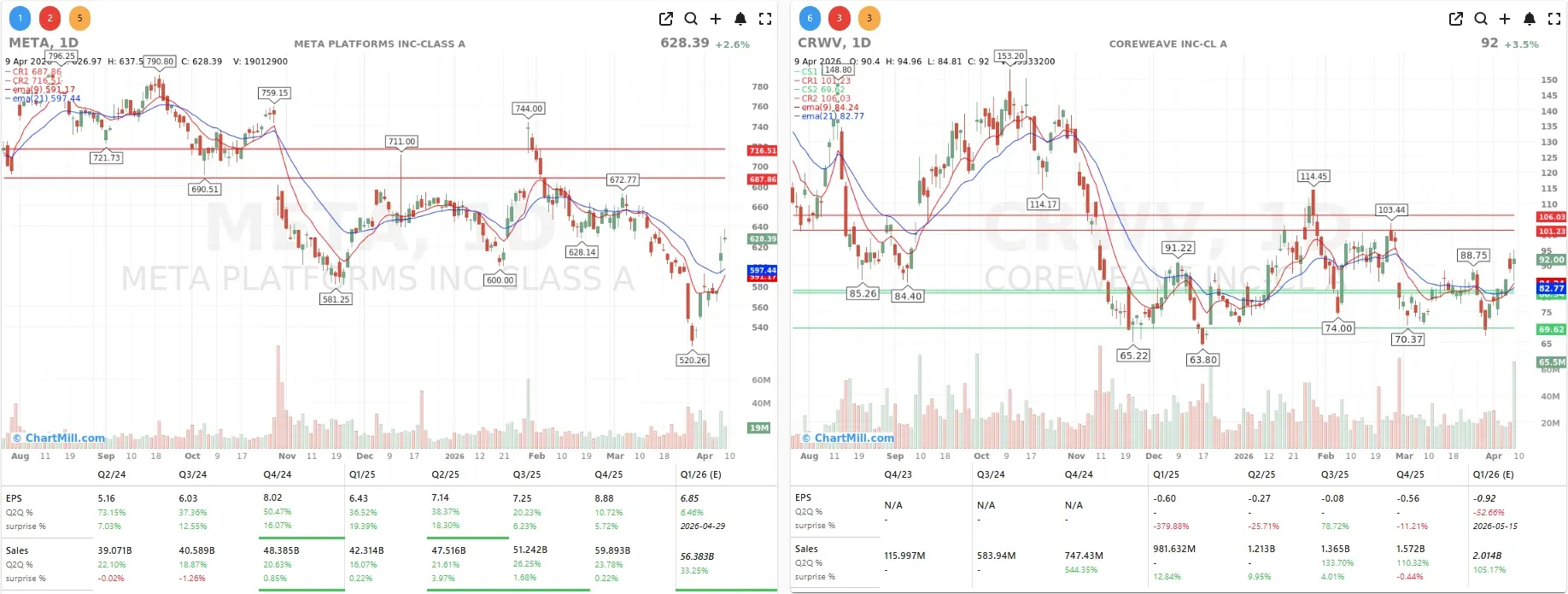

That's a direct move into territory that enterprise software companies have owned comfortably for years. And Meta (META | ▲2.61%) simultaneously introduced its Muse Spark AI model, adopting a closed strategy that points toward premium paid applications. The competitive pressure on traditional software is coming from multiple directions at once.

I don't think this is irrational market panic. It's the market doing math, and the math is getting harder for software companies to argue with.

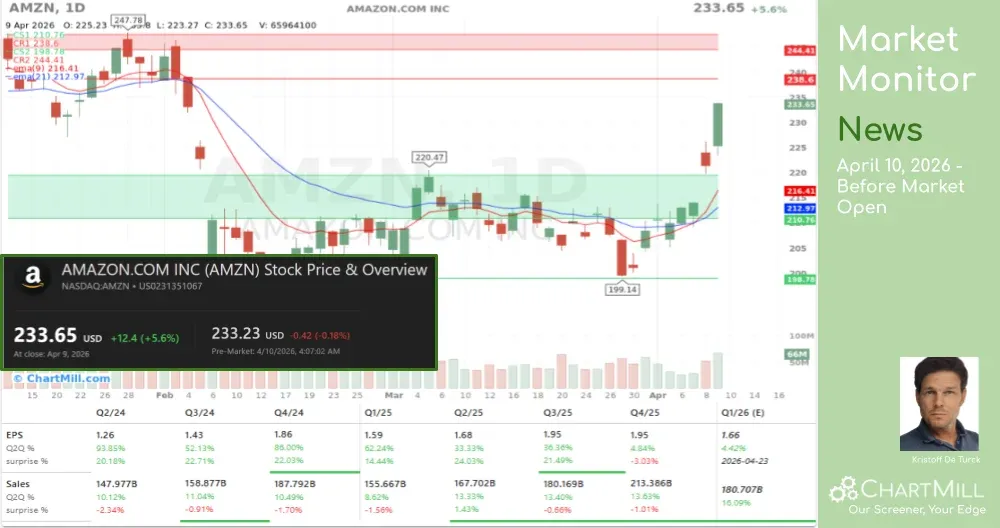

Amazon Puts a Real Number on AI

Against all that, Amazon (AMZN | ▲5.60%) had a genuinely good Thursday.

CEO Andy Jassy used his annual shareholder letter to reveal, for the first time, that Amazon's AI services within AWS generated over $15 billion in annualized revenue during Q1 2026. The stock rose 5.5%.

Why does this number carry so much weight? Because until now, the AI investment story has been running almost entirely on capital commitments and belief. Amazon alone is planning $200 billion in capital expenditure this year, a significant portion of it going into AI infrastructure. Investors have been patient, but they've been asking the same question quietly for months: where's the revenue?

Jassy answered it. "$15 billion, annualized, Q1 2026" is not a projection. It's not a narrative. It's a number from an actual running business.

And it reframes the entire hyperscaler capex debate. "AI is a once-in-a-lifetime opportunity," Jassy wrote. "Current growth is unprecedented and future growth even larger." You could normally file that under CEO optimism, but when it comes attached to a nine-figure revenue figure, it lands differently.

The Macro Data Is Quietly Concerning

Here's where I'd push back on the optimism a little. Thursday's economic data releases were, taken together, not good.

The final Q4 2025 GDP reading came in at 0.5% annualized, revised down from a prior estimate of 0.7%, and well below the growth rate a healthy economy should be producing.

At the same time, core PCE inflation for February printed at 3.0% year-over-year, with a monthly increase of 0.4%. That combination - slowing growth, sticky inflation - is exactly the scenario the Fed is least equipped to handle.

Weekly jobless claims added to the picture: 219,000 new claims, up 16,000 from the prior week, and above the 210,000 consensus expectation.

Personal income in February fell 0.1% when a small rise was expected, while spending rose 0.5%, slightly below forecasts. Americans are spending more, earning less, and doing so in a slowing economy with elevated inflation. That's not a comfortable equation.

The futures market expects the Fed to leave rates unchanged for the rest of the year, not because the inflation problem is solved, but because the growth slowdown limits how aggressively the central bank can act.

The euro, for its part, climbed to $1.1707 as the dollar lost its safe-haven premium from the ceasefire, and the 10-year US Treasury yield fell to 4.297%. The ECB is now expected to raise rates twice before year-end, down from three hikes priced in before the ceasefire took hold.

Company News Worth Tracking

Intel (INTC | ▲4.7%) extended its gains for a second consecutive session, reaching its highest level in five years. There was no specific catalyst, the stock has simply been building momentum, and the market is noticing.

Memory chip makers broadly outperformed. Sandisk (SNDK | ▲9%) led the group after a positive analyst note from Cantor Fitzgerald. Marvell Technology (MRVL | ▲4.79%) added nearly 5% following a Barclays upgrade.

With AI infrastructure spending accelerating, semiconductor companies that supply memory and compute are in a good position structurally.

CoreWeave (CRWV | ▲3.49%) announced a $21 billion cloud infrastructure deal with Meta (META | ▲2.61%), running through December 2032. That's a seven-year contract at scale, the kind of arrangement that signals hyperscalers are not treating AI infrastructure as a temporary spending cycle.

BlackBerry (BB | ▲8.22%) reported better-than-expected quarterly results and issued an optimistic outlook, gaining about 8%.

Constellation Brands (STZ | ▲8.53%) delivered a beat on earnings but disappointed with its guidance. The market chose to focus on what actually happened rather than what management warned about, and the stock gained nearly 9%.

Tesla (TSLA | ▲0.7%) picked up a modest gain after Reuters reported the company is developing a smaller, cheaper electric SUV. The news moved the stock only marginally, which says something about where expectations and attention currently sit.

Bitcoin held near $72,000, while gold and silver continued to attract buying interest despite the easing geopolitical risk. The safe-haven trade hasn't fully unwound.

Friday's CPI Is the Next Test

Everything that happened Thursday could look very different by Friday afternoon.

March CPI data for the US is due, and the consensus is expecting a significant move: monthly inflation is forecast to jump from 0.3% in February to 0.9% in March, a sharp acceleration. On an annual basis, the headline rate is expected to rise from 2.4% to 3.3%, with core CPI moving from 2.5% to 2.7%.

If those numbers land in line with expectations, or worse, above them, the conversation about rate cuts gets pushed further into the future, the dollar strengthens, and the equity rally of the past two days faces a direct challenge. The ceasefire might hold and oil might stabilize, but an inflation print that runs hot rewrites the monetary policy story in a way that market optimism can't simply absorb.

The setup going into Friday is fragile in the best sense of the word: everything is pointing in roughly the right direction, but it's pointing there on thin ice.

Bottom line

The ceasefire relief trade has legs, but it's not the kind of conviction rally you build a portfolio around.

Amazon's $15 billion AI revenue disclosure is the most significant fundamental development of the week, it validates the capex story in a way that analyst projections never could. The software sector's pain, meanwhile, looks structural: the repricing isn't done. And with March CPI coming Friday, anyone who extended risk into the rally is about to find out whether that was early or simply wrong.

ChartMill Market Desk - Kristoff

This daily update is prepared by ChartMill for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.

Next to read: Breadth Holds Its Ground as Participation Improves Beneath Resistance