Thursday was the second consecutive record close for the S&P 500 and the Nasdaq, and for most of the session the driver was straightforward: TSMC's quarterly numbers were the kind of print that leaves the semiconductor bulls feeling vindicated. Then Netflix reported after the bell, and within minutes the stock was down 8% on two pieces of news the market clearly hadn't priced in, a softer forward outlook and the departure of Reed Hastings from the chairman's seat.

The Rundown

- The S&P 500 and Nasdaq notched fresh record closes, with chip stocks doing the heavy lifting after a blowout quarterly report from Taiwan Semi

- PepsiCo pulled off something it hasn't managed in years: actual volume growth in its snacks business, on the back of aggressive price cuts

- Oil pushed higher on Pentagon comments about keeping the Strait of Hormuz blockade in place, even as Trump repeated that an Iran deal is "close"

- After-hours fireworks from Netflix capped the session, with a weaker-than-expected forecast landing at the same moment as the co-founder's surprise exit announcement

Another Record, This Time With a Taiwanese Accent

The Nasdaq (COMPX | ▲0.36%) added another 0.4% to extend Wednesday's all-time high, and the Dow Jones (DJI | ▲0.24%) tacked on 0.2%. The S&P 500 also closed at a new peak. Two sessions in a row of record closes, and the tone this time came almost entirely from one earnings report out of Taiwan.

TSMC (TSM | ▼3.13%) delivered Q1 numbers that are hard to overstate in scale.

Revenue grew more than 40% year-on-year to 1,134 billion Taiwanese dollars (roughly 30 billion euros). Net profit jumped 58% to 572 billion Taiwanese dollars, which works out to a net margin around 50%. Read that again. A company this size, at this stage of its cycle, running 50% net margins. The company also nudged its 2026 outlook higher, now guiding to "more than 30%" revenue growth for the full year.

The stock itself actually closed 3.13% lower, a reminder that when expectations are already sky-high and the shares have run ahead of the print, even a blowout can be sold.

But the read-through to the rest of the chip complex was immediate. AMD (AMD | ▲7.80%) ripped almost 8% higher. ON Semiconductor (ON | ▲10.35%) added more than ten.

The message being priced in across those names is clear: the AI datacenter build-out is not slowing, it's accelerating, and TSMC's capacity book confirms it.

PepsiCo Finds Its Volume Back

PepsiCo (PEP | ▲2.28%) put up a quarter that will get more attention than the headline numbers suggest.

Organic revenue growth came in at 2.6%, ahead of expectations, and adjusted EPS also beat. The story sits in the snacks business. Volumes in the unit that houses Doritos and Lay's grew 2% in the quarter, the first time in years that division has shown actual volume expansion, not just price-led growth.

What made it work: price cuts of up to 15%, which clearly moved product off shelves faster than the previous "push price, absorb the volume loss" playbook was allowing.

Operating margin rose despite pressure on gross margin, which is the tell. The company kept its 2026 guidance intact.

JPMorgan analyst Andrea Teixeira flagged a structural point that's worth holding onto: PepsiCo is hedged against commodity price increases roughly six to nine months out. That means if Iran-driven input cost pressure does materialize, the bill doesn't show up until Q4 at the earliest.

Investors pricing the stock as if the worst-case inflation scenario is already in the numbers might be too pessimistic on the near-term; they might also be too complacent on what's coming next year.

Oil Moves the Wrong Way Again, and the Iran Dance Continues

Trump told reporters Thursday that he expects an Iran deal to be announced "fairly soon" and that the outcome would deliver what he called "free oil and a free Strait of Hormuz" for the United States. He also announced that Israel and Lebanon are prepared to agree to a ten-day ceasefire.

On the same day, Secretary of War Pete Hegseth told a Pentagon gathering that the blockade of the Strait of Hormuz will remain in place "as long as necessary." Those two statements do not sit comfortably in the same news cycle. Oil markets picked the more cautious signal. WTI rose nearly 4% to $95 a barrel, a meaningful move that interrupts the steady drift lower in crude prices we've been watching for weeks.

I've written before about the gap between what equity markets are pricing (Iran resolution coming) and the actual state of the Strait (still blockaded, still disrupting roughly a fifth of global supply). Thursday's oil move is the kind of session where that gap narrows briefly. One more Hegseth-style comment, or one failed round of talks, and the war premium starts finding its way back into risk assets.

The Netflix After-Hours Bombshell

Netflix (NFLX | ▲0.07%) barely moved during regular trading. The action came after the close, and it came in two parts.

Part one: the numbers.

- Revenue rose 16% to $12.3 billion, beating the $12.2 billion consensus.

- EPS came in at $1.23, versus the $0.76 the Street was expecting. That's a meaningful beat, helped substantially by a $2.8 billion break fee from the abandoned Warner Bros. Discovery acquisition (Paramount Skydance won that bidding war in late February).

- Viewing hours up,

- engagement at a company-record level,

- advertising on track for $3 billion this year,

- ongoing conversations with the NFL about expanding their partnership. The quarter itself read clean.

Part two: the forward guide, and the seat change.

Netflix is guiding to $0.78 EPS for Q2, against a consensus of $0.84. That stands out when the stock has been running hot. And in the same release, Reed Hastings announced he is stepping down as chairman in June to focus on philanthropy and personal interests.

Hastings co-founded the company with Marc Randolph in 1997 as a DVD-by-mail service. He became CEO in year three, turned Netflix into the streaming business we know, handed day-to-day control to Ted Sarandos and Greg Peters in early 2023, and has been executive chairman since.

The company insists there is no link between his departure and the failed Warner bid. Management went out of its way to note Hastings was a strong supporter of that deal. Maybe. The timing is still awkward, and the market doesn't love awkward.

The stock dropped roughly 9% in after-hours trading. That number will mature overnight and into Friday's open.

Stories That Added Their Own Weight

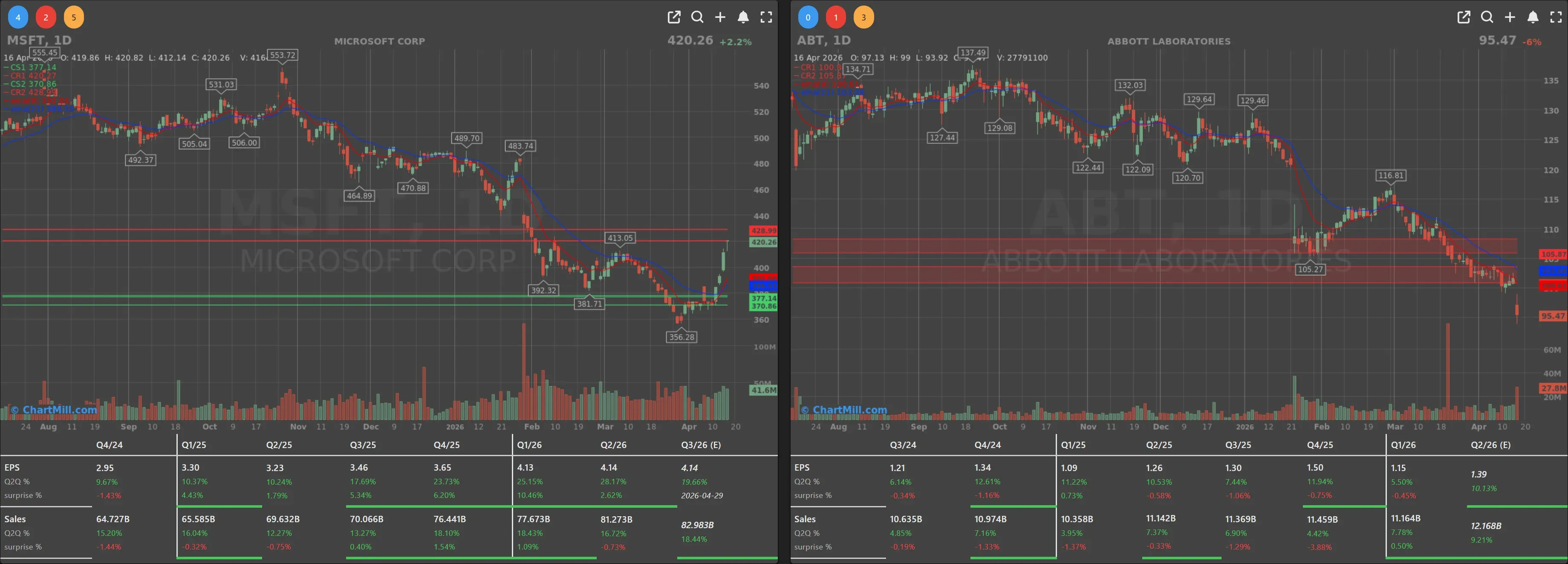

Stellantis has hired Microsoft (MSFT | ▲2.20%) to accelerate its AI rollout. The two companies will jointly build more than 100 AI projects across sales, customer service, and operations. Microsoft up 2.2% on the day, which for a company that size is not a throwaway move.

Abbott Laboratories (ABT | ▼6.00%) dropped 6% after its Q1 showed continued softness in medical devices revenue. A reminder that "earnings season is going well" is a statement with exceptions in every direction.

Voyager Technologies (VOYG | ▲8.79%) jumped 8.5% after NASA selected the company for an astronaut mission. Small-cap, specific-catalyst move, but worth noting for the space-exposed corners of the market.

Nvidia (NVDA | ▼0.26%) drifted slightly lower. Broadcom (AVGO) closed with a modest gain. Not every chip name moved the same way on TSMC's print — and that selectivity is healthy. When the entire sector moves in lockstep on a single earnings release, it's usually a sign that not enough stock-picking is happening underneath the tape.

The Macro Pieces, and the Fed Question That Won't Leave

Thursday's data was mostly supportive.

- Jobless claims came in 11,000 lower.

- The Philly Fed index jumped from 18.1 in March to 26.7 in April, where the consensus was actually looking for a decline. Both of those point to an economy that is not rolling over, while a lot of the bull case for equities right now assumes resilience into the second half.

- Industrial production fell 0.5% in March after a 0.7% gain in February, and capacity utilization ticked down from 76.1 to 75.7. Not catastrophic, but the kind of print that says the industrial side of the economy isn't participating in the broader optimism.

- Euro/dollar closed at 1.1786.

The thing I keep coming back to is the Fed.

On Wednesday, Trump again leaned on Jerome Powell, this time threatening to remove him from the chair if he doesn't step down when his term ends in May. Powell can technically remain as a governor past that date.

The Senate hearing on Kevin Warsh's nomination to replace him is scheduled for next Tuesday, though Senate Democrats are trying to delay it. Senator Thom Tillis has threatened to block any Fed nominee until the judicial review of Powell's tenure is complete.

Markets have been shrugging at this noise for weeks. Either investors don't believe the threats will translate into action, or they've decided the institutional structure around the Fed is strong enough to absorb the pressure. I don't think either conclusion is fully correct, the shrug is the market's position and it's the one you have to trade against.

Bottom Line

Thursday was a quietly impressive session in the main tape and a loud one in the after-hours window.

The records are extending, chip stocks are leading, consumer staples are quietly finding volume again, and the earnings season continues to deliver more beats than misses. That's the constructive read, and it's the honest one.

The risks are the same risks I keep flagging because they keep being true: the Strait of Hormuz is still blockaded, oil can flip higher on a single Pentagon soundbite, and the Fed is operating under political pressure that no equity market has really tried to price.

Add Netflix's after-hours move to that list, when a $400 billion name drops 9% in thin trading on a guide and a chairman exit, it usually ripples for a session or two.

ChartMill Market Desk - Kristoff

This daily update is prepared by ChartMill for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.

Next to read: Breadth Extends the Breakout