With crude oil surging to its highest level since June 2022 and Donald Trump detonating a late-night pharmaceutical tariff bombshell, Thursday's session was never going to be a quiet one and yet, in a feat of sheer stubborn resolve, Wall Street clawed its way back from a 2% opening crater to close the day marginally in the green.

There's a lot to unpack before the Easter bells ring, so let's get to it.

The Rundown

- The Nasdaq recovered from a -2% open to close up 0.2% as sentiment improved throughout the session.

- WTI crude oil surged after Trump's speech offered no clear timeline for ending the Iran conflict or reopening the Strait of Hormuz.

- Tesla fell sharply after Q1 2026, putting the stock down 20% year-to-date.

- Blue Owl Capital capped redemptions at 5%, rattling the broader private credit space.

- Trump signed two tariff decrees: metal and pharmaceuticals.

- Amazon is reportedly in advanced talks to acquire Globalstar.

- Markets are closed today (Good Friday).

A Wild Ride That Ended Closer to Calm

The Nasdaq shed nearly 2% in the first minutes of trading, and the mood was bleak.

Investors had gone to bed Wednesday night with high hopes pinned on a presidential address about the Iran conflict, and those hopes were promptly dashed when Trump's speech turned out to be long on rhetoric and short on timelines. The initial market reaction was brutal.

But the story of Thursday is really one of recovery. By the closing bell, the Nasdaq had turned positive - up 0.2% - in what I can only describe as a display of quiet determination from buyers who weren't ready to give ground.

It wasn't a triumphant session by any means, but the resilience mattered, especially heading into a long holiday weekend where markets are shuttered today (Good Friday) across most of the Western world.

The Oil Shock That Wall Street Couldn't Shake

WTI crude oil closing at $111 per barrel represents an 11% surge in a single session and a price level not seen since June 2022.

What's more, for the first time in four years, WTI is trading above Brent North Sea oil, a reversal that's partly technical in nature. WTI is currently priced for May delivery while Brent has already rolled to June, meaning markets are pricing in a higher risk of supply disruption in the near term than further out. That's not exactly reassuring.

What shook markets at the open wasn't so much the oil spike itself, but the absence of a roadmap.

Trump's speech had been billed as a potential inflection point, perhaps a ceasefire signal, a negotiation framework, anything concrete. Instead, he indicated the US intends to escalate further.

Reports from CBA's Global Economic & Markets Research noted that Washington has doubled its fleet of A-10 Warthog ground-attack aircraft in the Middle East, raising the probability of a ground or air invasion.

As CBA put it directly: the military build-up increases the likelihood of an invasion, and the dollar should benefit from safe-haven flows as a result. The EUR/USD pair confirmed that view, drifting lower to 1.1540 on Thursday evening.

There was one small thread of diplomacy to hold onto: reports emerged that Iran and Oman are jointly drafting a protocol to regulate shipping traffic through the Strait of Hormuz. It's not a solution, but it's not nothing either.

Options traders, meanwhile, have reportedly been hedging their S&P 500 exposure aggressively in both directions, bracing for either a sudden peace deal that sparks a massive rally, or a further escalation that would tank equities. According to UBS, that two-sided hedging activity has become unusually intense.

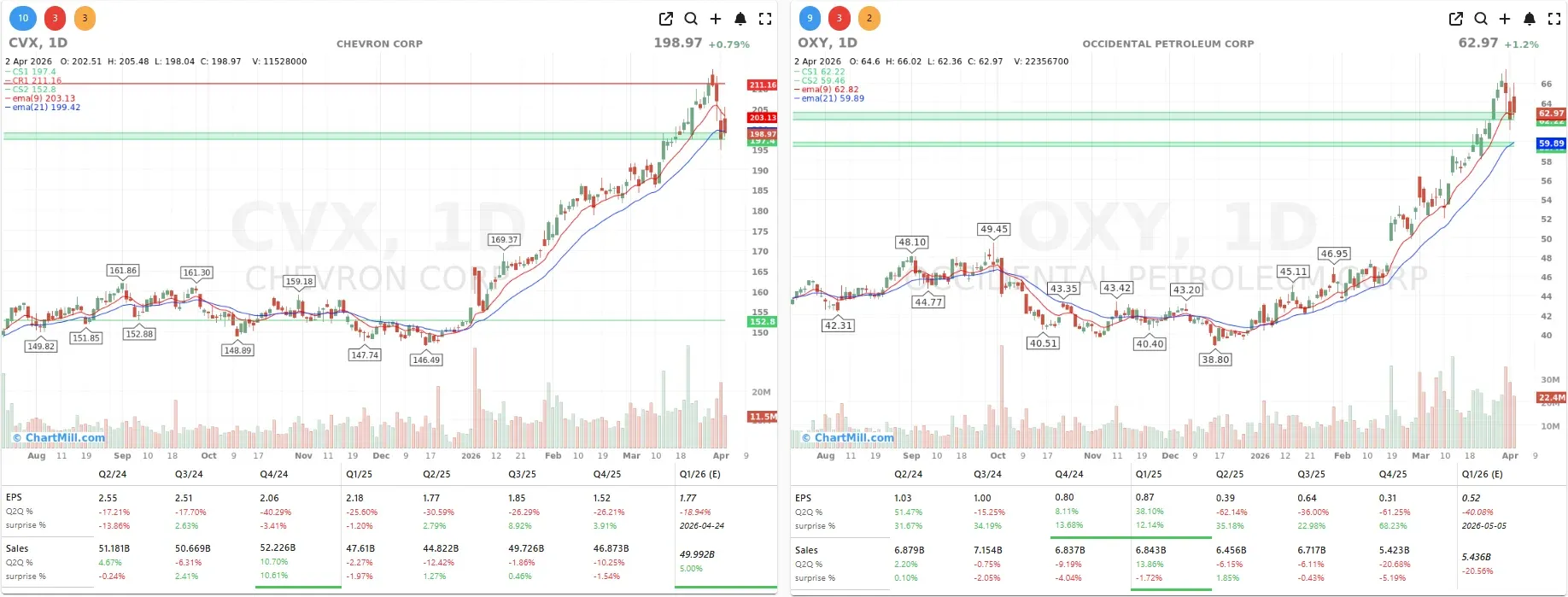

Energy stocks got an initial boost from the oil surge, but ultimately closed only modestly higher.

Chevron (CVX | ▲0.79%) and Occidental Petroleum (OXY | ▲1.19%) gained less than 1.5% combined, a telling sign that investors recognize $111 oil is a double-edged sword for the broader economy.

Tesla's Delivery Miss: Good Enough Isn't Good Enough

Tesla (TSLA | ▼5.42%) delivered 358,023 vehicles in Q1 2026, a number that, on the surface, looks fine. It's 6% ahead of the same quarter a year ago, and after the rough ride Tesla endured throughout 2025, any year-on-year improvement should feel like progress.

The problem is that "progress" was supposed to be 365,000 units. Analysts had pencilled in around 365,000, and missing that mark by roughly 7,000 vehicles was all the excuse the market needed to send the stock down over 5% and hit a fresh 2026 low. Tesla is now down 20% since January 1.

Much of the Q1 recovery in car sales was driven by cheaper, stripped-down versions of the Model 3 and Model Y, Tesla's core volume platforms.

The larger Model S and Model X are being wound down and will exit production in the coming weeks. Cybertruck and the Semi truck are still generating volumes that barely move the needle at the group level.

Elon Musk continues to frame Tesla primarily as an AI and robotics company, but those businesses don't yet generate the cash flow that the car division does.

Investors will have a sharper look at the underlying financials when Tesla reports earnings later this month, and I expect that to be the more decisive moment for the stock.

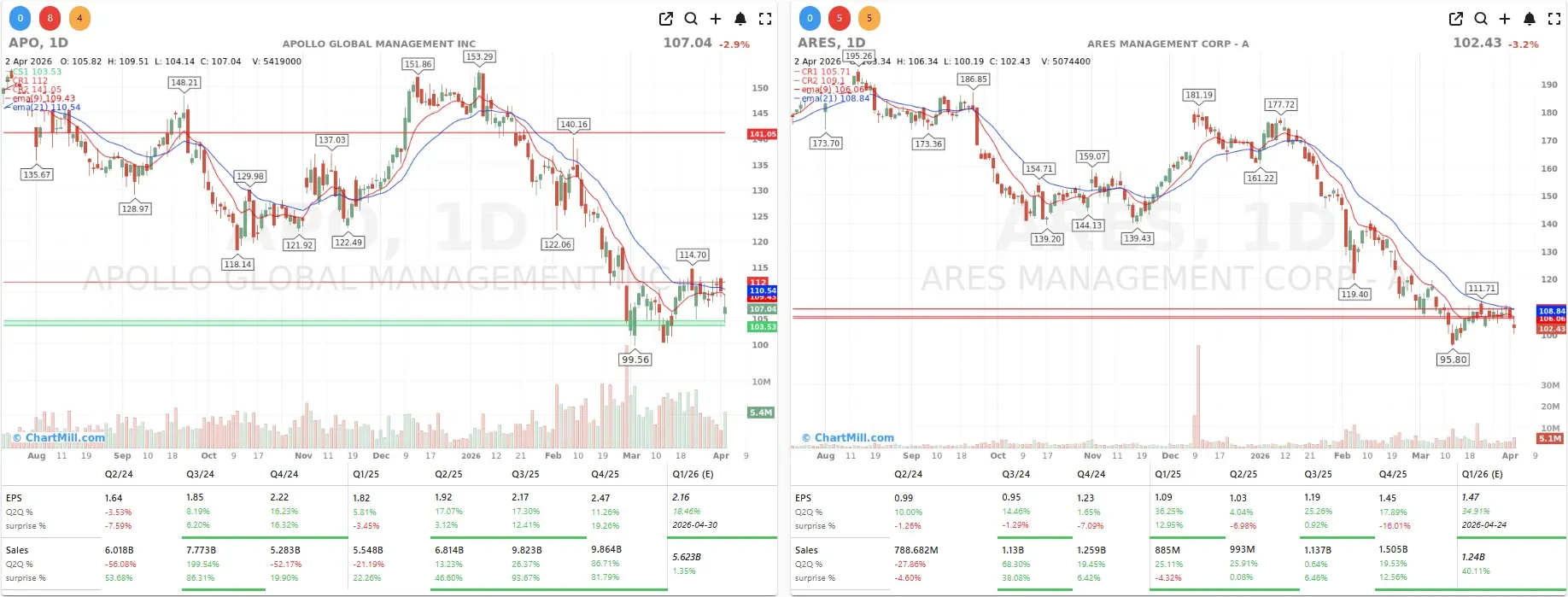

Private Credit's Uncomfortable Moment in the Spotlight

The private credit industry has been navigating turbulence for weeks, but Thursday brought the clearest signal yet that the stress is intensifying.

Blue Owl Capital (OWL | ▼1.61%) announced it would cap redemptions at 5% across two of its private credit funds after investors submitted redemption requests that went far beyond what the funds can normally accommodate.

In the larger of the two - Blue Owl Credit Income Corp., a $36 billion fund - shareholders asked to redeem nearly 22% of their stakes during the most recent quarter, representing roughly $7.9 billion in exit requests against the 5% cap. In the smaller, technology-focused fund, the number was even more alarming: over 40% of investors sought the exit.

To put that bluntly, those funds are seeing a run dynamic that management has now formally moved to contain.

Blue Owl's stock dropped as much as 6% intraday before recovering to close down just 1.6%, but the damage to confidence across the sector was wider.

Apollo Global Management (APO | ▼2.91%) and Ares Management (ARES | ▼3.19%) both fell sharply, as investors recalibrated the risks embedded in private credit exposure.

The combination of Iran-driven risk aversion and growing concern about the concentration of software and tech-adjacent companies in private credit portfolios is proving to be a combustible mix.

Trump Turns the Tariff Screws on Metal and Medicine

Metal Tariff Simplification

The first tariff move of Thursday was a housekeeping exercise by any other name, though the implications for manufacturers are real.

Trump signed a presidential decree revising how import duties on steel, aluminum, and copper products are calculated. The previous regime applied a 50% tariff only to the metal value contained within an imported finished product, a formula that was complex to administer and easy to game.

The new rule replaces that with a flat 25% tariff on the total value of finished products made with imported metals. Commodity-grade raw metals retain their 50% tariff, and any product with less than 15% metal content by weight will instead face the standard 10% minimum global tariff rather than the metal-specific regime.

The Pharmaceutical Bombshell

The second tariff announcement landed late Thursday evening and carries far more market-moving potential, though investors will have to wait until Easter Monday to fully price it in.

The Trump administration confirmed it will impose tariffs of up to 100% on patented brand-name pharmaceutical products imported by companies that have not yet struck pricing deals with Washington. The measure covers both finished drugs and their active pharmaceutical ingredients.

The logic behind the levy is the administration's "most-favored-nation" framework: if you're selling your drug cheaper abroad than in the US, you either lower US prices or face a punishing import duty. Companies that have already signed pricing agreements with the Health and Human Services Department, a list that includes Pfizer (PFE), Eli Lilly (LLY), and Novo Nordisk (NVO), makers of the blockbuster GLP-1 drugs Ozempic, Wegovy, and Mounjaro, are exempt from the new tariffs for three years under their existing deals.

For those that haven't yet come to the table, the clock is ticking: larger companies have 120 days before the 100% tariff kicks in; smaller manufacturers get 180 days.

This is a policy with significant global ramifications. European and Asian pharma companies without US pricing agreements face a potential tripling or quadrupling of their effective cost to serve the American market.

The announcement was framed as a national security measure, which gives the White House legal cover to act without Congressional approval. I expect this to be one of the dominant market narratives for the next several weeks.

Amazon Takes Aim at Starlink

One of the more intriguing stories of the day came via the Financial Times: Amazon (AMZN | ▼0.38%) is reportedly in advanced acquisition talks to buy satellite communications operator Globalstar (GSAT | ▲13.42%) for approximately $9 billion.

The strategic rationale is obvious, Amazon's Leo (low-earth orbit) internet constellation needs infrastructure, and acquiring Globalstar would give it a meaningful shortcut in the race to compete with Elon Musk's SpaceX Starlink, which has a significant head start in deployed satellites and market penetration.

GSAT surged more than 13% on the news, which is a rational response to a reported bid at or above market cap. What's less clear is how the Apple dimension plays out.

Cupertino's stake isn't just financial, it's strategic, tied to the satellite emergency SOS feature on recent iPhone models. Getting Apple to the table, or buying them out, adds both cost and complexity to any deal.

Still, if Amazon pulls this off, it would represent a significant escalation in the space internet wars.

Macro Watch: Jobs Report Today, Market Reacts Monday

Thursday's macro data offered a few moments of relative comfort amid the noise.

Weekly initial jobless claims came in at 202,000, a decline of 9,000 versus the prior week and a figure that suggests the US labour market, while slowing, is not in freefall.

That said, the trade deficit for February widened by nearly 5% to $57.3 billion, as both exports (+4.2%) and imports (+4.3%) expanded. The deficit with China stood at $13.1 billion for the month; with the European Union, $5.1 billion.

The data point that really matters drops this morning, however: the March non-farm payrolls report.

Economists are pencilling in 59,000 net new jobs for March, which would be a significant rebound from the 92,000 decline recorded in February. The context is sobering regardless: over the past ten months, the US economy has created a net total of just 34,000 jobs.

A print significantly below or above consensus today will shape the narrative into next week, but since US markets are closed for Good Friday, the reaction will have to wait until Easter Monday.

Bottom Line

Thursday was, in short, a day where markets chose resilience over retreat but the problems haven't gone away.

Oil at $111 is a tax on the entire economy. Iran remains the single biggest wildcard, and Trump's escalatory posture means the situation could tip in either direction with little warning.

Tesla's delivery miss, while not catastrophic, confirms that even the year's tentative recovery in EV demand is fragile.

Private credit is showing genuine stress. And two fresh tariff volleys, one simplifying metal duties, one threatening to upend global pharmaceutical trade, land into a market that was already stretched thin.

Heading into Easter weekend, I'd summarise the mood as cautiously on guard. The jobs number today will either add to the anxiety or provide a brief reprieve but either way, Wall Street won't be able to act on it until Monday.

Have a good Easter!

ChartMill Market Desk - Kristoff

This daily update is prepared by ChartMill for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.

Next to read: Breadth Keeps Repairing, But Long-Term Damage Is Not Gone Yet