When it comes to long-term investing, one approach that consistently stands out is quality investing. Unlike pure value strategies that hunt for bargains, quality investing focuses on companies with durable competitive advantages, strong profitability, and solid financial health, the kind of businesses you would be happy to hold for years, if not decades. To identify such candidates, we turned to the Caviar Cruise stock screener, a methodology inspired by the principles laid out in Luc Kroeze’s "The Caviar Formula." This screen filters for companies that demonstrate consistent revenue and earnings growth, high returns on invested capital, manageable debt, and strong cash flow conversion. One name that emerged from this rigorous process is MSA Safety Inc (NYSE:MSA), a specialist in protective equipment and gas detection technology.

Meeting the Core Criteria

The Caviar Cruise screen is built on several non-negotiable pillars, and MSA Safety checks nearly every box with room to spare. Here is how the company stacks up against the key metrics:

- Revenue Growth (5Y CAGR) > 5%: While the exact 5-year revenue CAGR is not available in the provided data, MSA’s historical revenue growth of 6.82% per year over the past years comfortably exceeds the 5% threshold, indicating a steady expansion of its top line.

- EBIT Growth (5Y CAGR) > 5%: MSA’s EBIT has grown at an impressive 14.02% annually over the past five years. This is more than double the minimum requirement and signals that the company’s core operations are scaling efficiently.

- EBIT Growth > Revenue Growth: With EBIT growth of 14.02% outpacing revenue growth of 6.82%, MSA demonstrates improving profitability. This spread often points to economies of scale or pricing power, both hallmarks of a quality business.

- ROICexgc > 15%: The company’s Return on Invested Capital, excluding cash, goodwill, and intangibles, stands at a stellar 28.01%. That is well above the 15% bar and places MSA in the upper echelon of capital allocators. A high ROIC suggests the company is generating strong returns on every dollar reinvested into the business.

- Debt / FCF < 5: MSA’s debt-to-free-cash-flow ratio is just 1.97. This means it would take less than two years of free cash flow to pay off all outstanding debt, a very healthy position that reduces financial risk.

- Profit Quality (5y Average) > 75%: The average profit quality over five years is an extraordinary 208.81%. This figure, which measures free cash flow relative to net income, indicates that MSA converts far more than its reported profit into actual cash. While high CapEx can sometimes drag this number down, in MSA’s case, the company is generating abundant cash, a sign of a mature, well-run operation.

These metrics align directly with the Caviar Cruise philosophy: the screen prioritizes companies that not only grow but do so profitably, with strong cash generation and a conservative debt profile. MSA Safety exemplifies this balance.

Financial Health at a Glance

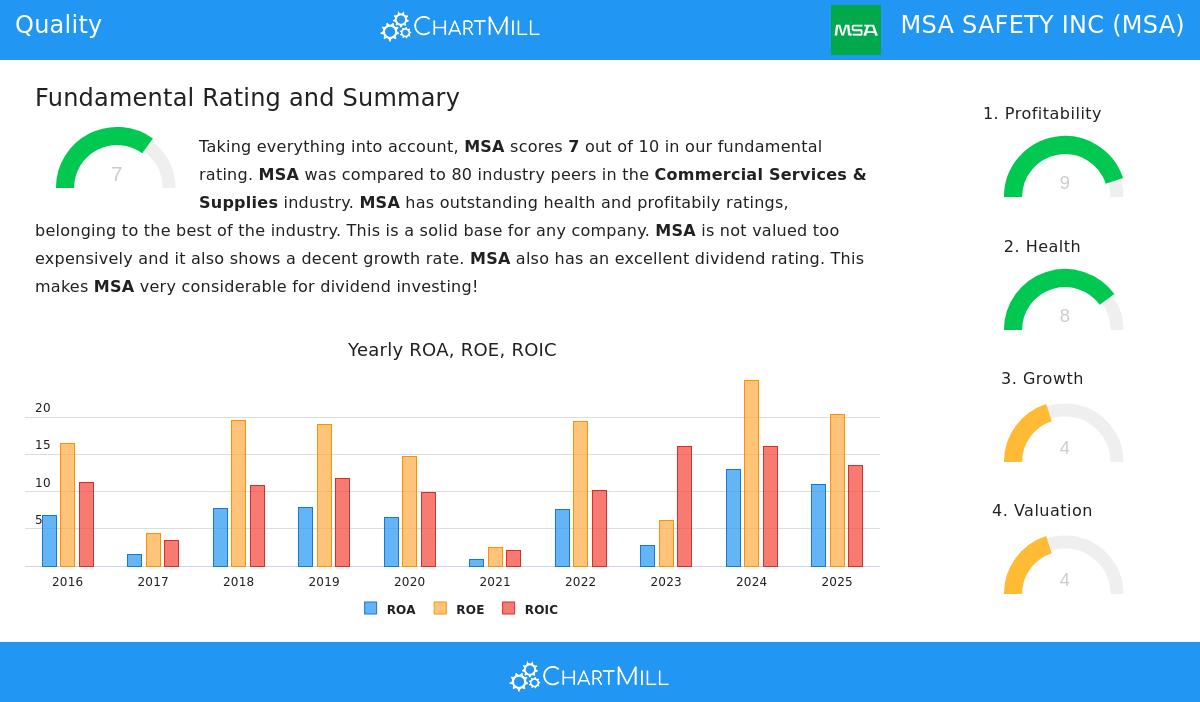

According to Chartmill’s fundamental analysis report, MSA Safety earns an overall rating of 7 out of 10, supported by standout scores in several areas. The company’s profitability rating is excellent, with Return on Assets, Return on Equity, and Return on Invested Capital all ranking among the top 12-17% of its industry peers. Margins are equally impressive: a profit margin of 14.87% and an operating margin of 21.01% place MSA in the top 5% of the Commercial Services & Supplies sector. On the health front, the company has an Altman-Z score of 5.69 (indicating very low bankruptcy risk) and a current ratio of 3.01, pointing to strong liquidity. Dividend investors will also note a 1.23% yield supported by a sustainable payout ratio of just 29.53%.

You can examine the full breakdown of these figures via the detailed fundamental analysis report.

Analyst Outlook and Valuation Considerations

While quality investors are willing to pay a fair price for excellence, valuation still matters. MSA trades at a P/E ratio of 21.42, which is slightly above the industry median but cheaper than roughly 74% of its peers. Its forward P/E of 19.30 also suggests modest expectations for near-term earnings growth. That said, the PEG ratio does raise a concern, the stock’s current price may not be fully justified by near-term growth alone. However, given MSA’s superior profitability metrics, a premium valuation is not uncommon for companies of this caliber. The long-term growth picture remains positive, with analysts forecasting EPS growth of 10.19% annually over the next few years.

Finding More Quality Candidates

The Caviar Cruise screen is designed to surface companies that embody the traits of durable, high-quality businesses, and MSA Safety is a textbook example. But it is by no means the only one. If you want to explore the full list of stocks that pass this rigorous quality filter, you can run the screening criteria yourself and see which other names make the cut.

Disclaimer: This article is for informational and educational purposes only and does not constitute investment advice. Always conduct your own research or consult a licensed financial advisor before making any investment decisions.