For investors looking to balance the search for growth with prudence, the "Growth at a Reasonable Price" (GARP) method presents a practical middle path. This method tries to find companies showing strong and lasting growth, but whose shares are not priced at the high levels common to speculative names. It removes both stagnant value stocks and overly expensive growth options, concentrating on businesses where future earnings growth is not completely reflected in the current market price. One instrument to use this method is an "Affordable Growth" stock filter, which generally searches for good growth scores, firm profitability and financial soundness, and a valuation that is not extreme. A present example from such a filter is Lam Research Corp (NASDAQ:LRCX), an important company in the semiconductor equipment field.

A Profile in Semiconductor Strength

Lam Research is a fundamental part of the global semiconductor supply chain, designing and building the sophisticated equipment used to make integrated circuits. Its tools are necessary for producing the memory chips and logic devices that operate everything from smartphones and data centers to cars. Headquartered in Fremont, California, the company's results are linked to spending cycles within the semiconductor industry, which are now being fueled by long-term trends in artificial intelligence, high-performance computing, and the Internet of Things. This situation provides a basic support for growth.

Assessing Growth Path

The central idea of the GARP method is finding real, quantifiable growth, and Lam Research performs well on this point. The company's fundamental report notes exceptional speed in both its recent results and future outlook.

- Past Performance: Over the last year, Lam Research has recorded notable growth measures, with Revenue rising by 26.85% and Earnings Per Share (EPS) jumping by 45.70%. This shows not just revenue growth but also effective scaling and profitability.

- Sustainable Speed: The growth is not a single-quarter event. The company's average yearly EPS growth over recent years is a solid 21.02%, with Revenue growing at an average of 12.91% per year.

- Future Outlook: Importantly for a growth investor, this speed is anticipated to persist. Analysts forecast average yearly EPS growth of 21.46% and Revenue growth of 12.77% going forward. The consistency between past and expected growth rates points to a steady, rather than irregular, growth trend.

This steady and strong growth description is exactly what the Affordable Growth filter looks for, as it creates the basis for possible future stock price gains.

Valuation in Context

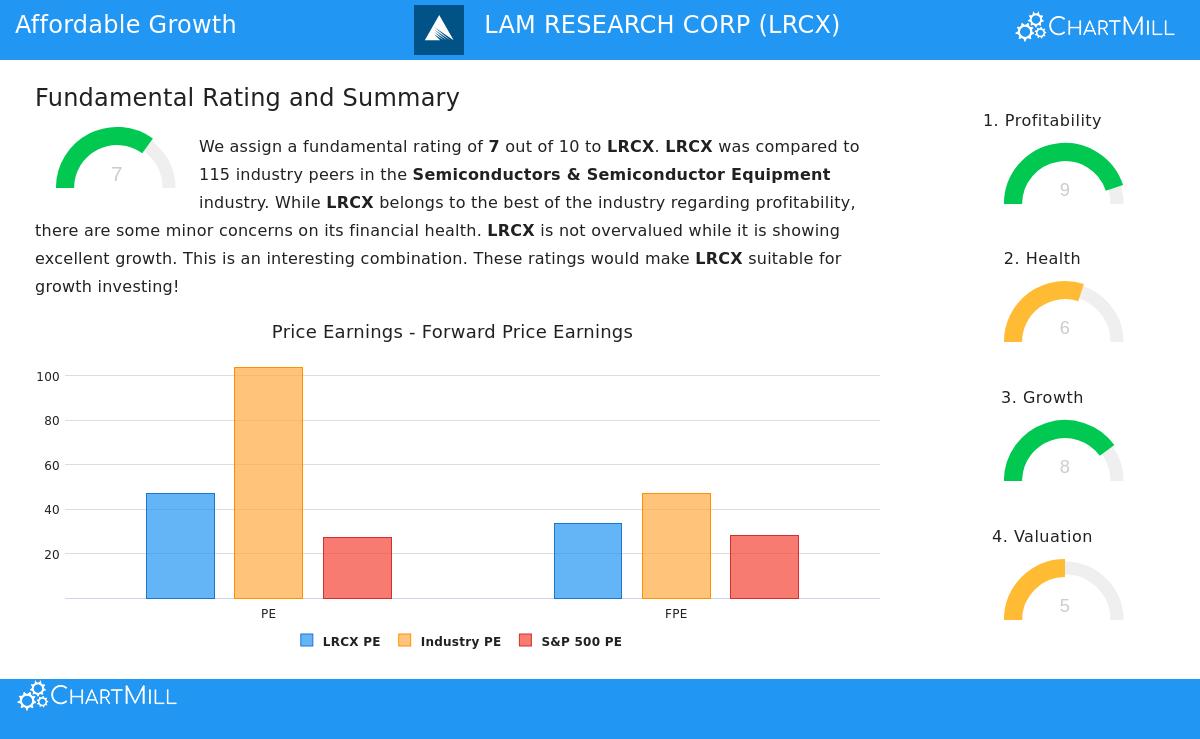

While growth is necessary, paying a fair price for it is what describes the GARP method. Lam Research offers a detailed valuation view. On its own, its Price-to-Earnings (P/E) ratio of 47.14 seems high compared to the wider S&P 500 average. However, valuation must be judged relative to both its growth speed and its industry competitors.

- Industry Comparison: Within the high-growth semiconductor equipment sector, Lam Research is not unusual. Almost 70% of its industry competitors trade at a higher P/E ratio. Its Forward P/E of 33.59 is less expensive than over 60% of the industry and matches the S&P 500 average closely.

- Growth Adjustment: The important measure here is the PEG ratio, which modifies the P/E for expected earnings growth. For Lam Research, this points to a fair valuation, indicating the market price fairly accounts for its growth outlook. The report states that its very good profitability may support a higher price.

- Other Measures: The company also looks good on other valuation checks, trading as less expensive than most competitors on Enterprise Value-to-EBITDA and Price-to-Free Cash Flow ratios.

This context is important. The filter's need for a valuation score above 5 tries to avoid the most overpriced names. Lam Research's valuation, while not "low" in simple terms, can be seen as fair within its high-performing sector and compared to its strong growth path.

Supporting Fundamentals: Profitability and Health

Lasting growth cannot exist without a profitable business model and a firm financial base. Lam Research does very well in profitability, which backs its growth and supports its valuation. Its financial health, while good overall, has some small points to note.

Profitability Strengths: The company's profitability measures are very good, rating among the top in its industry.

- Very Good Returns: It has a Return on Invested Capital (ROIC) of 40.64%, doing better than 99% of its competitors, showing highly efficient use of capital to create profits.

- Firm Margins: With an Operating Margin of 33.76% and a Profit Margin of 30.22%, Lam Research shows significant pricing ability and operational efficiency.

Financial Health Description: The company's financial health is good, with enough ability to fund growth and return capital to shareholders.

- Good Solvency: It has a low Debt-to-Free Cash Flow ratio of 0.72, meaning it could pay off all debt in under a year with its cash flow. Its Debt/Equity ratio is a workable 0.37.

- Sufficient Liquidity: Its Current Ratio of 2.26 shows no problem covering short-term debts, although this ratio is in the lower part of its industry, a minor point mentioned in the analysis.

These supports of profitability and health are essential for the Affordable Growth method. They make sure the company's growth is built on a stable foundation and lower the risk linked to purely speculative expansion.

Conclusion

Lam Research Corp shows the features looked for by the Growth at a Reasonable Price method. It presents a practical and well-supported growth story, both in history and in its projected future. While its simple P/E ratio is high, its valuation becomes more acceptable when considered against its industry and, most significantly, its growth speed, as seen in its PEG ratio. This is combined with top-level profitability and a basically sound balance sheet. For investors filtering for "affordable growth," LRCX stands as a candidate where strong business results are not completely outweighed by a too-high market price. A complete breakdown of these fundamental ratings is found in the full Lam Research fundamental analysis report.

The search for good growth stocks at fair valuations is a continuous process. Investors wanting to examine other companies that pass similar filters can perform their own study using the Affordable Growth stock screener.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation to buy or sell any security, or an endorsement of any investment strategy. The information presented is based on data provided and should not be the sole basis for an investment decision. Investors should conduct their own thorough research and consider their individual financial circumstances and risk tolerance before making any investment.