For investors looking for a dependable source of passive income, a systematic screening process is needed to distinguish secure dividend payers from hazardous yield traps. One useful technique uses filters for stocks that have a high dividend rating, indicating good yield, growth, and sustainability, and also possess firm basic profitability and financial soundness. This layered method aids in finding companies able to maintain and raise their distributions over many years, instead of those presenting high yields because of a falling stock price or weak foundations. Using this tactic with a set stock screener recently identified pharmaceutical leader Eli Lilly and Co (NYSE:LLY) as a prospect for more detailed review.

Dividend Profile: A Focus on Growth and Reliability

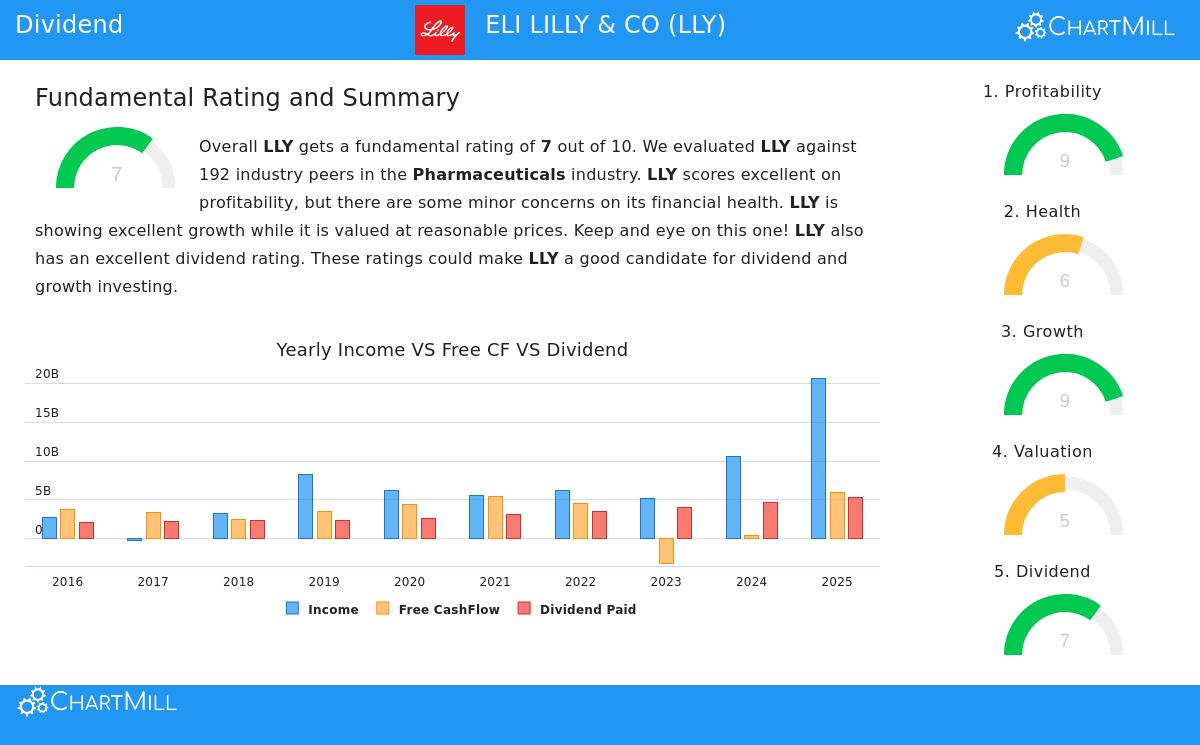

While Eli Lilly’s present dividend yield of about 0.77% is low, particularly next to the wider S&P 500 average, the company’s dividend profile is set apart by its remarkable growth and reliability, important supports for a long-term dividend growth plan. As stated in its fundamental analysis report, Lilly’s dividend story is persuasive for a few organized reasons:

- Notable Dividend Growth: The company has raised its dividend at an average yearly rate of 15.17% over the last five years. This steady and large growth is a clear sign of management’s belief in the firm’s future cash flows and dedication to giving capital back to shareholders.

- Excellent History: Lilly has a dependable record, having paid and, importantly, not reduced its dividend for at least ten straight years. This long history offers a degree of predictability that income-focused investors greatly appreciate.

- Maintainable Payout Ratio: Sustainability is where Lilly does very well. The company uses only around 26% of its earnings for dividend payments. This low payout ratio gives a large buffer, making sure the dividend is safe even if earnings encounter short-term challenges. Also, the report states that earnings are rising quicker than the dividend, supporting the maintainability of future raises.

This mix fits well with a dividend growth plan. The aim is not to pursue the greatest immediate yield, which can frequently be a caution signal, but to find companies with the monetary ability to dependably increase their distributions over time, thus raising an investor’s effective yield on cost.

Supported by Outstanding Profitability

A rising dividend is only as safe as the profits that pay for it. Here, Eli Lilly’s foundations are very firm, giving it a top ChartMill Profitability Rating of 9 out of 10. This high score is the driver that runs its dividend policy. Important profitability measures consist of:

- Better Returns: The company shows fine capital efficiency with a Return on Invested Capital (ROIC) of 31.47%, which places in the top group of its pharmaceutical industry counterparts. A high ROIC shows the company is skilled at creating profits from its investments, a direct origin of money for dividends and reinvestment.

- Growing Margins: Lilly’s profit margin is at a firm 31.66%, and its operating margin is a notable 45.56%. Importantly, these margins have been getting better in recent years, proposing not just firm profitability but also increasing operational efficiency and pricing strength.

For a dividend investor, this degree of profitability is key. It confirms the low payout ratio, showing that the dividend is not a pressure on resources. It gives plenty of space for the company to at the same time fund growth projects, manage debt, and compensate shareholders, a stable method that aids long-term dividend maintainability.

Evaluating Financial Health

The last support of the screening tactic is financial health, which works as a balance sheet security test. Eli Lilly gets a ChartMill Health Rating of 6, showing a basically sound but not perfect financial state. The examination shows a varied image:

- Strength in Solvency: The company has a firm Altman-Z score of 7.76, which shows a very small short-term risk of financial trouble and does better than most of its industry.

- Points to Observe: The report mentions a somewhat high Debt/Equity ratio of 1.54 and a Current Ratio of 1.58 that is lower than many industry peers. While the debt level is workable given the company’s large cash flow creation (shown by a good Debt-to-Free-Cash-Flow ratio compared to the industry), it is a point for investors to note. The health rating verifies the company is not in peril, but points out that its active growth and shareholder returns are partly funded through borrowing.

For the dividend plan, this health evaluation is important. It verifies the company is not on unstable footing, but also gives a clear look at the capital structure. The firm profitability and growth help balance the borrowing worries, but it shows the need to watch balance sheet patterns together with dividend payments.

A Prospect for Dividend Growth Portfolios

Eli Lilly and Co makes a strong case for investors using a dividend growth plan. It does very well in the central areas the screen was made to point out: a high dividend rating led by dependable, quickly growing distributions with a maintainable base; outstanding profitability that feeds those payments; and acceptable financial health that, while having some debt, is backed by excellent cash creation. The stock is more about the strong mix of dividend growth and company growth than about a high present yield.

For investors wanting to use this same systematic screening approach to find other possible prospects, the fully set "Best Dividend Stocks" screen is ready to examine. You can see and change the filters yourself through this link to the stock screener.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The information presented is based on data provided and should not be the sole basis for any investment decision. Investors should conduct their own independent research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results.