Some trading days feel like the market is collectively holding its breath.

Monday was one of those sessions; hesitant, slightly tense, and dominated by one big question: What happens when Nvidia reports on Wednesday? As I watched price screens drift lower throughout the day, it was clear that investors preferred to reduce risk rather than chase momentum.

A Nervous Market Sets the Tone

The major U.S. indices opened the new week in the red, unable to find a catalyst strong enough to push them higher. With the U.S. government finally back at work after the shutdown, fresh economic data is about to hit the tape again and that alone was enough to inject some uncertainty into the markets.

The Dow Jones slipped 1.2%, the S&P 500 lost 0.9%, and the Nasdaq Composite fell 0.8%. Nothing dramatic, but the tone was unmistakably defensive.

The biggest shadow hanging over the market? Nvidia (NVDA | -1.88%), the company at the center of the global AI mania. After a twelvefold stock run since early 2023, expectations are sky-high, perhaps uncomfortably high. The stock dropped another 1.9% on Monday as traders debated whether the valuation still has enough oxygen to climb further. Options markets, according to Jefferies, are pricing in a ±6% post-earnings swing. Buckle up.

Adding to the pressure, both SoftBank and tech investor Peter Thiel have now exited their Nvidia positions. When two high-profile early believers head for the exit at the same time, the market tends to notice.

Fed Officials Add to the Uncertainty

If earnings weren’t enough, the Federal Reserve added another layer of ambiguity. Two senior policymakers - Philip Jefferson and Christopher Waller - gave speeches Monday with slightly different tones.

Jefferson emphasized caution, noting the Fed may not have all the data it wants by the time the December interest-rate decision arrives. Waller, on the other hand, openly supported a 25-basis-point rate cut next month to guard against a sudden weakening of the labor market.

Later this week, new economic reports - including the long-delayed September jobs data - should help clarify the picture. For now, investors are left guessing.

Economic Data: Mixed but Encouraging

The Empire State Manufacturing Index jumped from 10.7 to 18.7, its highest level in a year. New orders climbed sharply as well. A pleasant surprise, though one data point doesn’t make a trend.

Corporate inventories also edged higher for August after delays due to the shutdown, and the euro/dollar settled around 1.1589.

Oil eased slightly, partly due to what analysts called a “technical breather” after last week’s rally, while attention now shifts to Wednesday’s U.S. inventory report.

Meanwhile, gold softened and Bitcoin briefly dipped below $92,000, a reminder that even digital assets aren’t immune to pre-Nvidia nerves.

Alphabet Shines After Surprise Berkshire Move

The one bright spot on Monday’s tape came from Alphabet (GOOGL | +3.11%), which jumped 3.1% after paperwork revealed that Berkshire Hathaway accumulated 17.85 million shares during Q2. That stake was worth nearly $5 billion at the end of last week.

This is noteworthy because Berkshire rarely dips its toes into big tech, apart from its massive long-term position in Apple. Alphabet is now the best-performing member of the "Magnificent Seven" this year, up roughly 46% year-to-date and still trading at a discount compared to the likes of Apple, Microsoft, or Nvidia based on P/E ratios.

Investors love a good “Buffett bought it” headline and Monday showed it still works.

Deal-Making in Healthcare: J&J Strikes

Johnson & Johnson (JNJ | +1.86%) grabbed attention with a $3.05 billion all-cash acquisition of privately held Halda Therapeutics, a biotech specializing in cancer treatments. Its lead candidate, HLD-0915, is targeting prostate cancer and is still early in clinical development.

The market liked the deal. J&J shares rose 1.9%, making it the day’s top performer in the Dow. Sometimes investors simply reward a clean, strategic move without overthinking it.

Corporate Highlights: A Mixed Bag

Several other companies made headlines on Monday, though not all for the right reasons:

-

Amazon (AMZN | -0.78%) fell 0.8% after announcing plans to issue at least $12 billion in bonds. The proceeds will go toward paying down debt and buying back shares.

-

HP Inc (HPE | -7.01%) dropped 6.8% after Morgan Stanley cut its rating and reduced the price target.

- Chinese EV maker Xpeng (XPEV | -10.32%) slumped more than 10% despite doubling revenue year-over-year; profitability remains elusive.

-

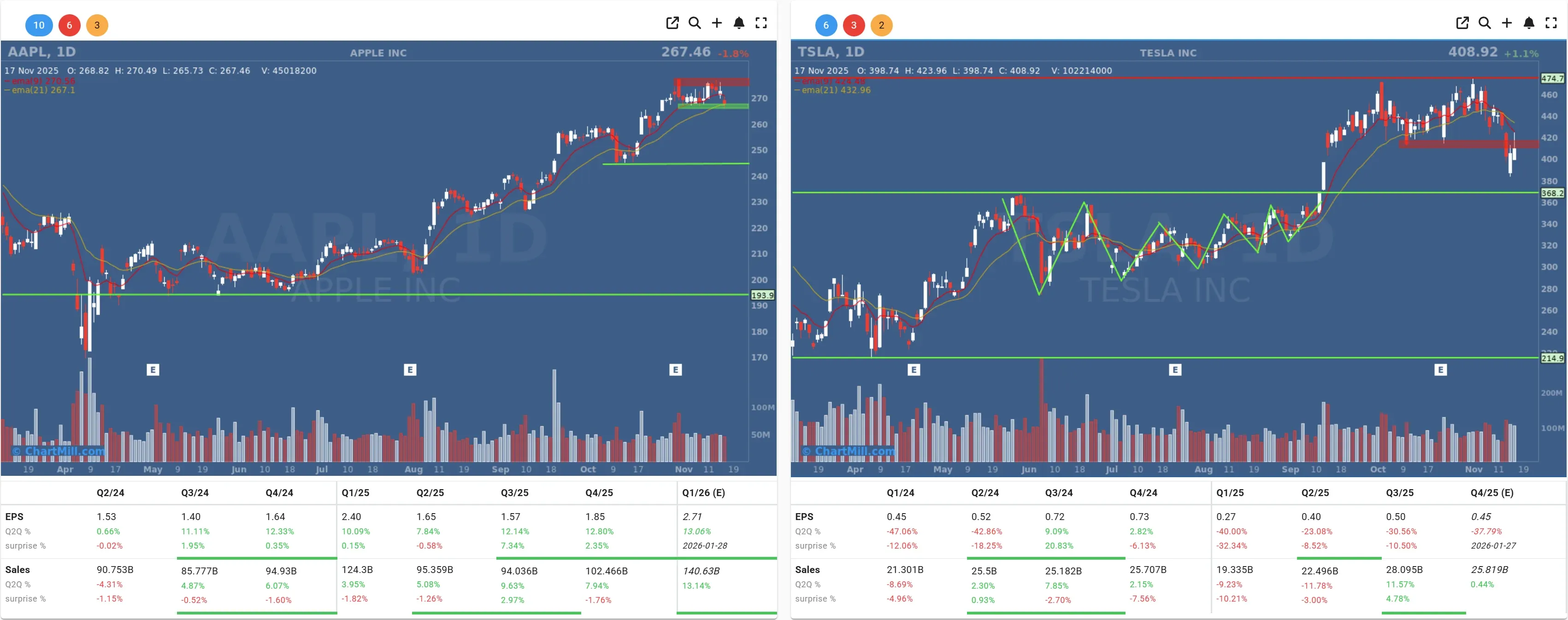

Tesla (TSLA | +1.13%) bucked the weakness, closing 1.1% higher. The company is now pressuring suppliers to avoid sourcing components from China, a development that could become significant if it spreads across the EV supply chain.

-

Apple (AAPL | -1.82%) slipped 1.8% as Berkshire trimmed more than $10 billion of its holdings in the tech giant during Q3.

Looking Ahead: All Eyes on Wednesday

The narrative for the rest of this week is already set. Tomorrow brings more economic data, but Wednesday evening’s Nvidia earnings will dominate the landscape. Given how heavily the entire AI-complex trades around Nvidia’s guidance, the results could influence market sentiment well into December.

For now, markets are cautious and I can’t blame them. When expectations fly too close to the sun, even a small disappointment can burn.

Kristoff - ChartMill

Next to read: Breadth Weakens Again as Selling Pressure Broadens