The Caviar Cruise screen is a stock screener designed to identify companies that fit the quality investing mold. Rather than hunting for the cheapest stocks, this methodology focuses on businesses that demonstrate consistent growth, strong profitability, efficient use of capital, and a healthy financial structure. The idea is to find companies with durable competitive advantages that can be held for the long term, paying a fair price for the quality they offer.

Howmet Aerospace Inc. (NYSE:HWM) has emerged from this screen as a candidate worth a closer look. The company, a specialist in lightweight metal products for jet engines, aerospace fastening systems, and airframe structural components, displays many of the quantifiable traits that quality investors prize.

Recent Performance and Growth

A core requirement of the Caviar Cruise screen is that a company must show solid historical growth, and not just in revenue. The screen demands a 5-year compound annual growth rate (CAGR) of at least 5% for both revenue and EBIT (earnings before interest and tax). Furthermore, it requires the EBIT growth to outpace revenue growth, which signals improving profitability and pricing strength.

Howmet meets these criteria decisively:

- Revenue Growth (5Y CAGR): 10.38% (well above the 5% threshold)

- EBIT Growth (5Y CAGR): 21.39% (significantly above both the 5% threshold and the revenue growth rate)

This combination is a strong indicator. It suggests that as Howmet has grown its top line, it has become more efficient, benefiting from economies of scale or strong pricing strength that allows more of each dollar of sales to flow down to operating profit.

Profitability and Capital Efficiency

The screen puts a heavy emphasis on how well a company uses its capital, which is central to the quality investing philosophy. The key metric here is the Return on Invested Capital (ROIC), specifically calculated to exclude cash, goodwill, and intangibles to get a pure look at operational efficiency.

- ROIC (Excluding Cash, Goodwill & Intangibles): 42.09%

This figure is extraordinarily high and far exceeds the screen’s minimum requirement of 15%. A ROIC of this magnitude indicates that Howmet has a formidable competitive moat and is extremely effective at turning its invested capital into profitable growth. It’s the hallmark of a business that does not just grow, but grows profitably.

The screen also looks at profit quality, which measures how much of the net income is converted into free cash flow.

- Profit Quality (5-Year Average): 96.49%

This is a very strong score, well above the 75% minimum. It shows that Howmet is excellent at turning its accounting profits into real, spendable cash, which is the lifeblood of any long-term investment.

Financial Health and Stability

For a long-term holding, financial stability is non-negotiable. The Caviar Cruise screen assesses this by looking at the company's debt relative to its free cash flow.

- Debt to Free Cash Flow (FCF): 2.13

This means that at its current free cash flow generation, Howmet could pay off all its debt in just over two years. This is comfortably within the screen’s target of 0 to 5 years, indicating a very manageable debt load and low financial risk.

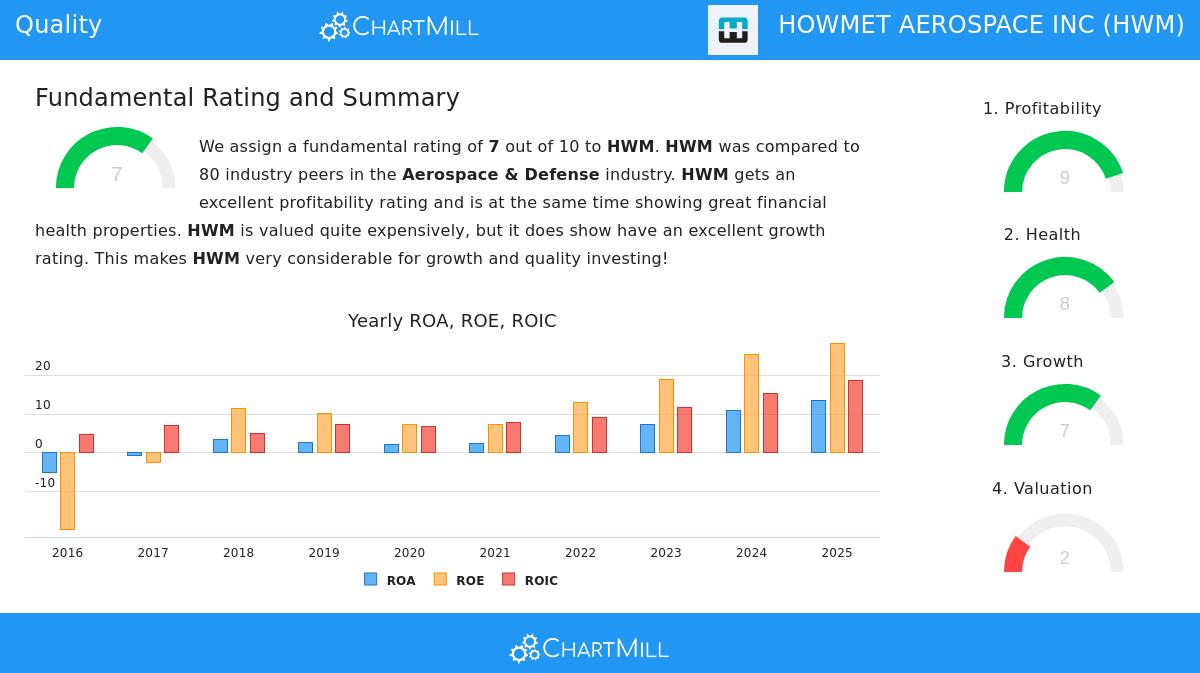

Summary from the Fundamental Report

Our detailed fundamental analysis, which you can view in detail here, gives Howmet a rating of 7 out of 10. The report highlights that its profitability and financial health are among the best in the Aerospace & Defense industry. Growth is also excellent. The main caveat, typical for high-quality companies, is its valuation. With a trailing P/E ratio of 65.71, the stock is considered expensive. This aligns with the quality investing principle that one must be willing to pay a fair, if not cheap, price for enduring quality, but it also highlights the need for careful valuation work before making a commitment.

Analyst Views

While not a direct filter in the screen, the market’s forward-looking expectations are relevant. Analysts expect Howmet’s earnings per share to grow by an average of 16.59% annually over the next few years, with revenue growing at 10.38% per year. This future growth, if realized, could help to justify the current premium valuation over time.

A Final Look at the Data

For a quick overview of how Howmet stacks up against the screen’s key metrics:

- Revenue Growth (5Y): 10.38% (Threshold: >5%)

- EBIT Growth (5Y): 21.39% (Threshold: >5% and > Revenue Growth)

- ROIC (Excl. Goodwill & Intangibles): 42.09% (Threshold: >15%)

- Debt / Free Cash Flow: 2.13 (Threshold: <5)

- Profit Quality (5Y Avg.): 96.49% (Threshold: >75%)

Conclusion

Howmet Aerospace presents a strong case for the quality investor. It demonstrates a rare combination of strong and profitable growth, exceptionally high returns on invested capital, and a rock-solid balance sheet. The major challenge is its high valuation, which requires a long-term perspective and a conviction that its competitive advantages will continue to drive growth. It is not a stock for bargain hunters, but for those who seek to own a piece of a high-quality business.

This screen is just one starting point. For more results and to build your own quality-focused portfolio, you can find the complete list of companies from this screen by following this link: Caviar Cruise Screen Results.

Disclaimer: This article is for informational and educational purposes only and does not constitute investment advice. All investments carry risk. You should conduct your own research or consult with a qualified financial advisor before making any investment decisions.