Just hours before Trump's deadline to "wipe out Iranian civilization" expired, Washington and Tehran agreed to a two-week ceasefire brokered by Pakistan.

Oil fell off a cliff. Futures surged. And that was before Broadcom decided to steal the spotlight with the most consequential AI chip deal of 2026.

Let me walk you through what happened and why the next two weeks matter more than most people realize.

The Rundown

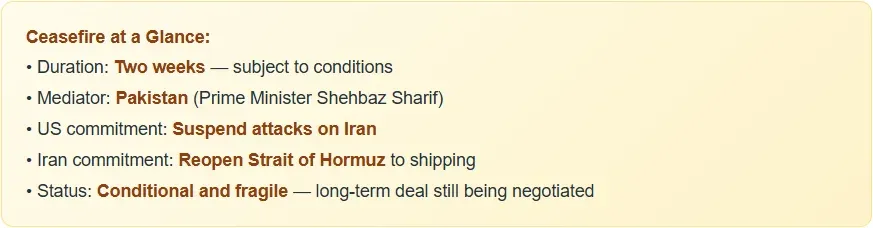

- US-Iran two-week ceasefire agreed via Pakistan, minutes before Trump's deadline. Strait of Hormuz set to reopen.

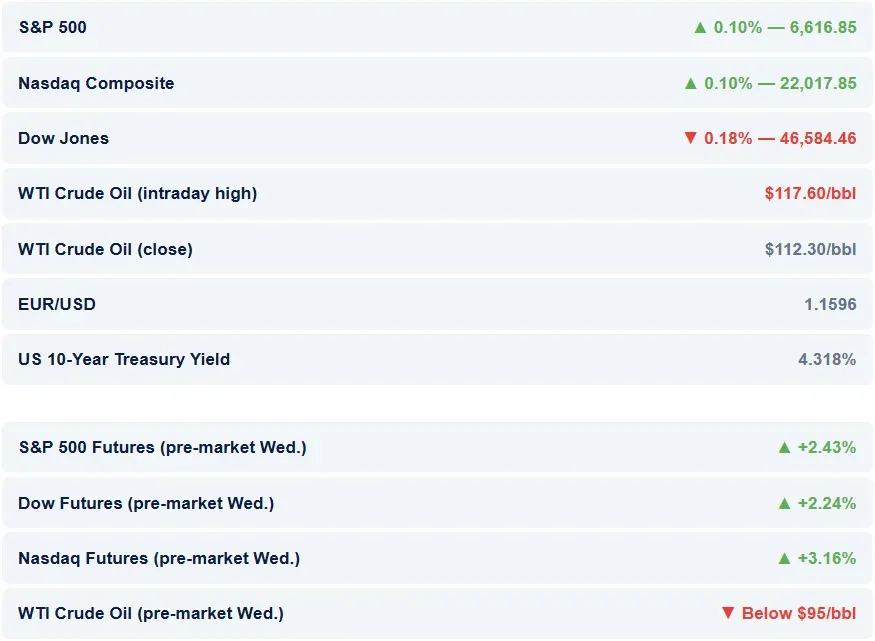

- Tuesday close: S&P 500 and Nasdaq +0.1%, Dow -0.18%. Wednesday pre-market: Nasdaq futures +3.16%, S&P futures +2.43%.

- Broadcom, multi-year AI deals with Google (TPU architecture through 2031) and Anthropic (3.5 GW compute by 2027).

- Healthcare surge: CMS finalized a 2.48% Medicare Advantage rate hike for 2027.

- Apple down on foldable iPhone setbacks. Arm Holdings down on Morgan Stanley downgrade.

- Friday's March CPI is the next key event, headline forecast to jump from 2.4% to 3.4%.

Tuesday Looked Quiet. It Wasn't.

On paper, Tuesday's session was almost boring. The S&P 500 and Nasdaq both closed up 0.1%. The Dow shed 0.18%. You'd look at those numbers and think: nothing happened. The reality is something completely different.

Markets spent the entire session grinding lower as Trump's midnight deadline - his ultimatum to Iran to reopen the Strait of Hormuz or face "unprecedented" military action - loomed larger with every passing hour. WTI crude touched $117.60 intraday. The mood was grim.

Then, around mid-afternoon New York time, Pakistan's Prime Minister Shehbaz Sharif posted on X.

He said diplomacy was progressing "steadily, powerfully, and resolutely." He asked Trump to extend the deadline by two weeks.

He asked Iran to open the Strait for the same period as a goodwill gesture. That single post, from a country that most investors weren't watching, was enough to spark a last-hour recovery. By the closing bell, buyers had clawed back the day's losses. And then, after hours, the actual deal came through.

The Ceasefire That Changed Everything Overnight

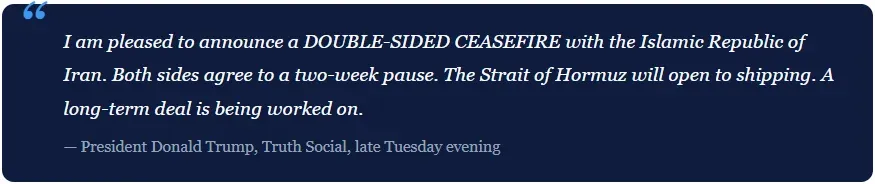

Tuesday on Truth Social, Trump threatened to erase "an entire civilization" by nightfall.

Just hours later, he was announcing a two-week suspension of hostilities. That's how fast the narrative flipped. The deal, mediated by Pakistan, with Iran conditionally agreeing to reopen the Strait of Hormuz, is fragile. But for markets that have been sitting on an oil price above $100 for weeks, "breathing room" is enough to trigger a massive repricing.

The Strait of Hormuz is the world's most important oil chokepoint. Since the US and Israel began military operations against Iran at the end of February, Tehran had effectively closed it. That closure is what sent WTI from $70-something to $111-plus in a matter of weeks.

So when the prospect of reopening it suddenly becomes real, the market reaction isn't subtle: oil futures fell nearly 19% from their intraday peak within hours, dropping below $95 heading into Wednesday's open.

It isn't a resolution. Iran's Foreign Minister Abbas Araghchi confirmed the agreement almost simultaneously with Trump's post, but the underlying dispute about Iran's nuclear program, sanctions, and regional influence hasn't moved an inch.

The ceasefire buys time, for diplomats, for negotiators, and yes, for oil traders to exhale. Whether it holds beyond two weeks is a question nobody can answer yet. The Strait attack on Kharg Island on Tuesday - the US struck but avoided energy infrastructure - shows how razor-thin the margins were. One miscalculation and the whole thing unravels.

Broadcom's Big AI Moment

On a day dominated by geopolitics, Broadcom (AVGO | ▲6.21%) managed to make itself the standout story in the technology sector. The company announced two landmark deals that effectively lock in its position at the center of the AI infrastructure buildout for the rest of the decade.

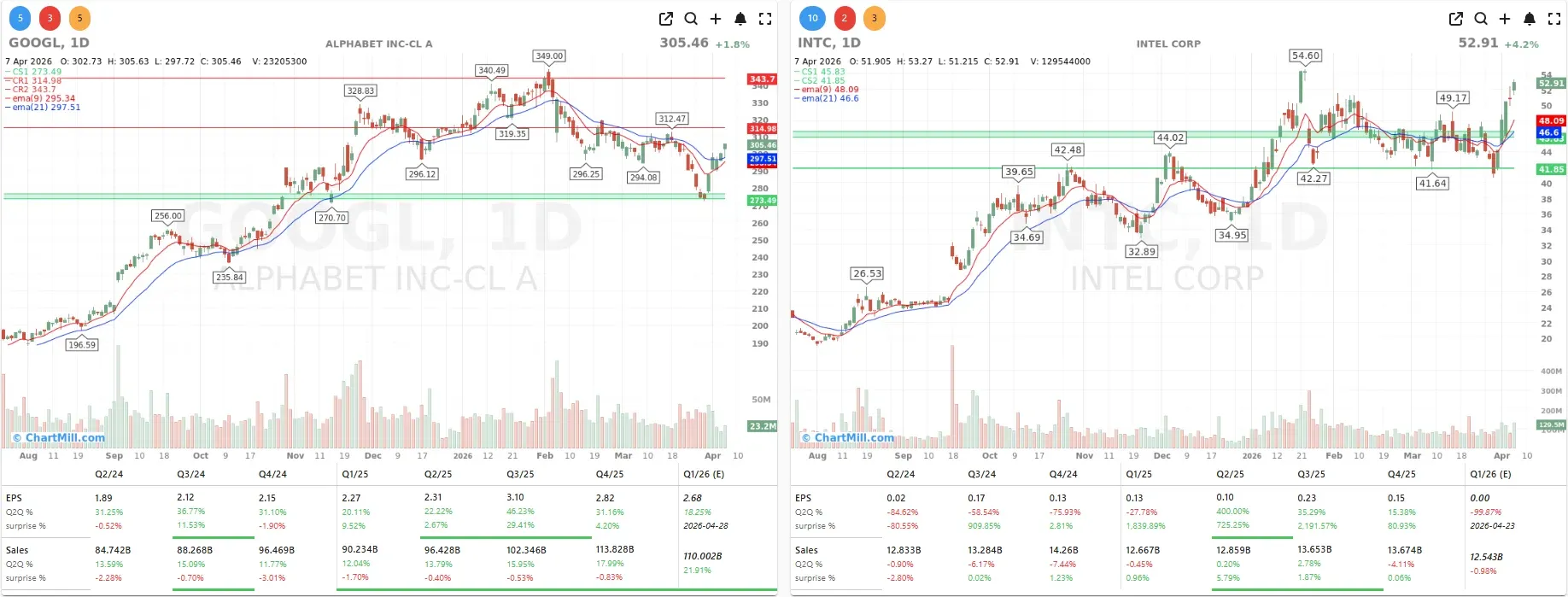

The first deal is a multi-year agreement with Alphabet to design and supply Google's next-generation custom Tensor Processing Units (TPUs) - its seventh and eighth generations - through at least 2031. Broadcom is essentially Google's exclusive chip architect for AI workloads, an alternative to buying off-the-shelf Nvidia hardware.

The current TPU v7, codenamed "Ironwood," is already in full production using a 3nm process. The deal also covers networking hardware and other components for Google's next-generation AI data centers. Both agreements run to 2031.

The second deal involves Anthropic, the AI company behind Claude, gaining access to roughly 3.5 gigawatts of AI compute capacity, to be delivered via Broadcom and Google's infrastructure by 2027. It's contingent on Anthropic's commercial success, which introduces some uncertainty, but given Anthropic's recent trajectory, few analysts seem particularly worried about that condition.

JPMorgan analyst Harlan Sur called it a visibility improvement that few semiconductor companies can point to.

Bloomberg Intelligence's Kunjan Sobhani was slightly more cautious, noting that "the good news may already be priced into consensus expectations", a fair point given that Broadcom has been on a tear.

Alphabet (GOOGL | ▲1.82%) gained modestly on the back of the announcement. Intel (INTC | ▲4.19%) also caught a bid on broader AI infrastructure enthusiasm, though Nvidia and AMD moved only marginally.

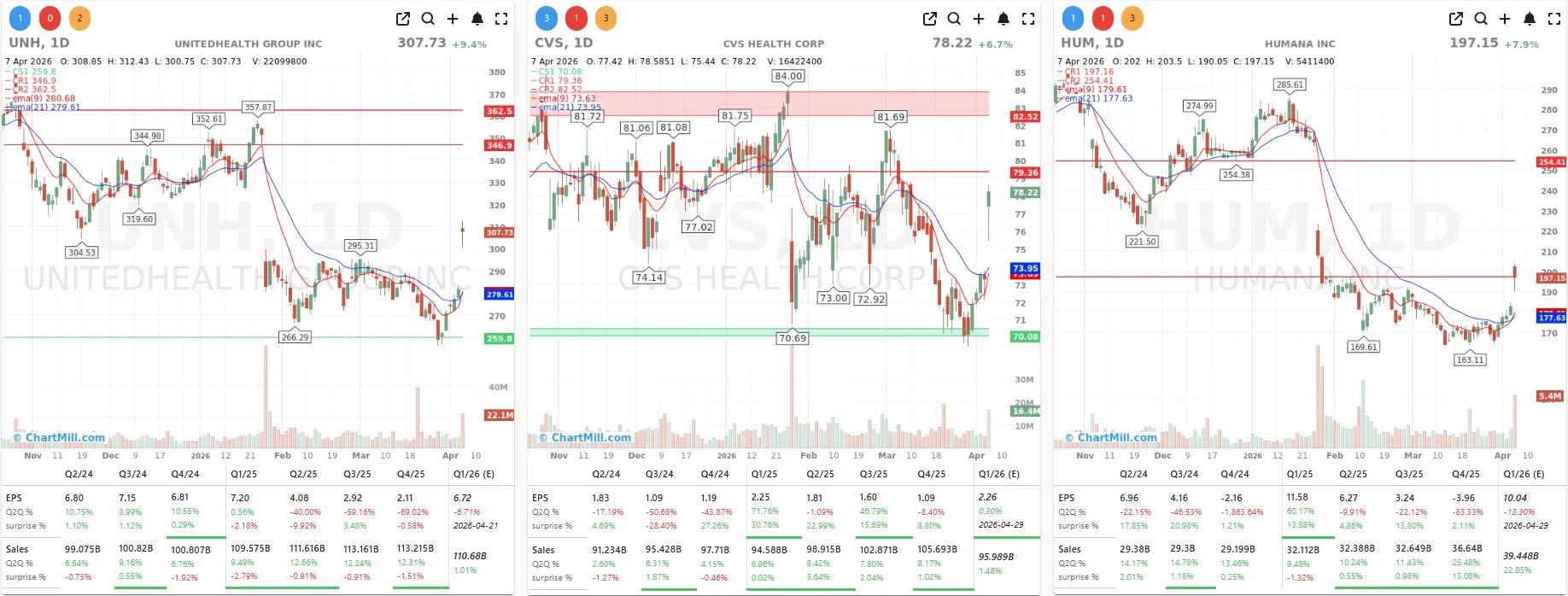

Healthcare Insurers Get an Unexpected Windfall

While all eyes were on geopolitics and chips, the healthcare sector quietly had one of its best sessions in months.

The catalyst was straightforward: the Trump administration's Centers for Medicare & Medicaid Services (CMS) finalized a 2.48% increase in Medicare Advantage payment rates for 2027, adding more than $13 billion in total payments to an industry that has been under significant financial pressure from rising medical utilization among seniors.

To put that number in context: back in January, the government had proposed a mere 0.09% increase. The final figure of 2.48%, which works out to an effective 4.98% when you account for risk-score adjustments, was well ahead of even the most optimistic industry estimates.

The market reacted accordingly. UnitedHealth (UNH | ▲9,37%), Humana (HUM | ▲7.94%), and CVS Health (CVS | ▲6.74%) all surged. Together these three companies cover close to 60% of all Medicare Advantage enrollees, so this isn't a niche story.

Insurers have spent most of the past two years absorbing higher-than-expected post-pandemic medical costs, a phenomenon known as elevated utilization, that squeezed margins hard.

This rate increase doesn't solve everything overnight, but it does give the sector a meaningful financial cushion heading into 2027. I'll be watching to see whether the momentum carries into Wednesday's open now that the ceasefire has added another tailwind to risk sentiment.

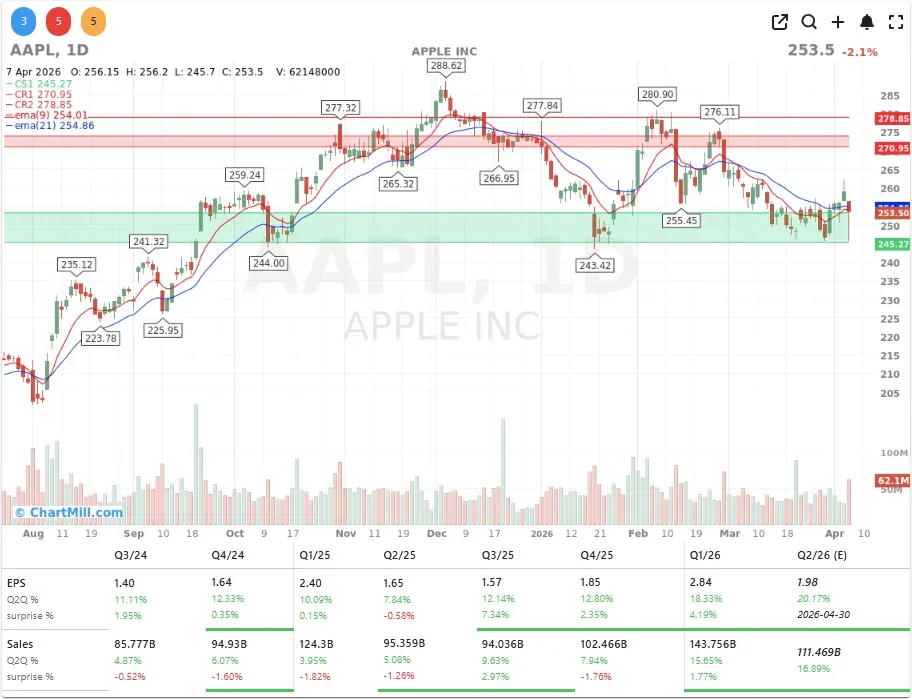

Apple Stumbles, Arm Gets Clipped

Apple's Foldable Problem

Apple (AAPL | ▼2.07%) fell after Nikkei Asia reported that the company is running into engineering setbacks during the testing phase of its first-ever foldable iPhone.

According to Nikkei's sources, the issues are more complex and time-consuming to resolve than Apple had anticipated and in a worst-case scenario, the initial delivery could slip by several months. The stock dropped 2.1% on the news.

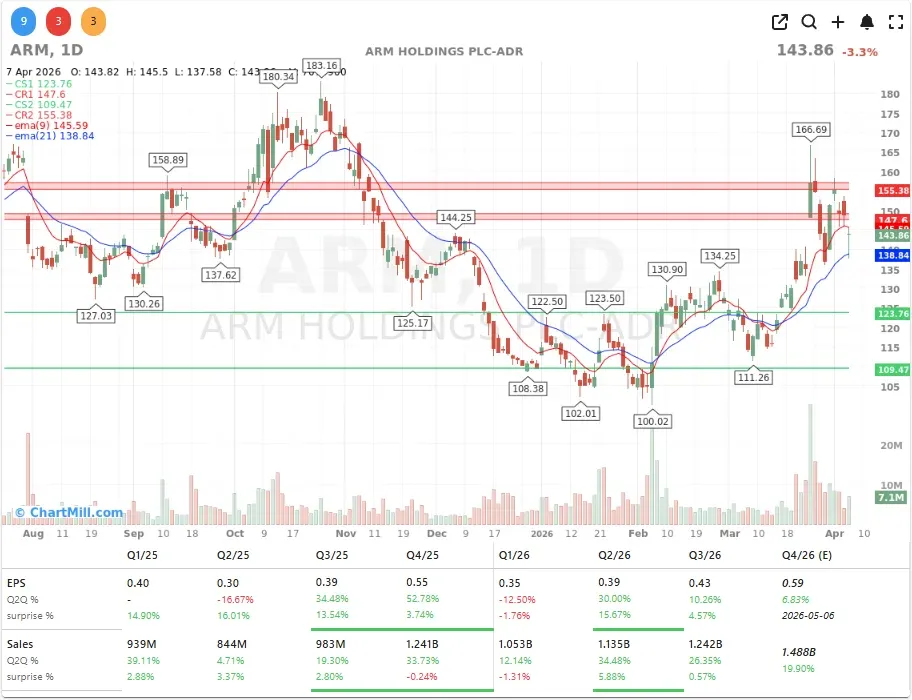

Arm Holdings: Morgan Stanley Pulls the Rip Cord

Arm Holdings (ARM | ▼3.3%) had a rougher session after Morgan Stanley downgraded the stock from Overweight to Equal-Weight. The bank's core concern is Arm's strategic pivot: it's transitioning from a pure intellectual property licensor toward manufacturing its own AI CPUs and merchant silicon.

That move brings Arm into direct competition with its own biggest customers, including Apple and Qualcomm, which Morgan Stanley warns could push them toward RISC-V alternatives and erode the royalty base that underpins Arm's entire valuation.

The bank did raise its price target to $150 (from $135), which is something. But the market focused on the margin dilution argument. Gross margins in merchant silicon typically sit between 40% and 50%, a long way below the IP licensing model. If Arm wins the AI CPU race but sacrifices its margin profile to do it, the math gets complicated fast.

Macro Watch: Inflation Expectations Are Moving and Friday Is Coming

The geopolitical drama tends to drown out everything else, but there's a macro story building underneath that deserves attention.

Tuesday's New York Fed consumer survey showed that 12-month inflation expectations among US households jumped from 3.0% to 3.4%, the sharpest single-month move in some time. Respondents also expect gasoline prices to rise 9.4% over the next year. Oil above $100 for an extended period will work its way through the economy, and people know it.

Friday's March CPI report is where this narrative gets real. Economists are forecasting a headline print of 3.4%, a full percentage point above February's 2.4% reading, with the Iran conflict's effect on energy prices already baked in.

The ceasefire announced overnight may take some edge off future oil-driven inflation, but March's numbers were already locked in before any of this week's diplomacy. That report will land into a market that will be scrambling to re-price both the inflation trajectory and the Fed's next move simultaneously.

The February durable goods miss and the slightly higher consumer credit reading don't add urgency to the picture, but they confirm the economy isn't exactly firing on all cylinders either.

Bottom Line

Wednesday's open is going to feel very different from anything we've seen in weeks. Futures are up sharply, oil is in freefall, and the ceasefire gives markets the excuse they've been looking for to buy.

But I'd encourage some caution before reading this as a turning point. A two-week ceasefire is not a peace deal. The Strait of Hormuz still needs to physically reopen. Iran's internal politics are complicated. And even if the oil shock eases, the inflationary damage it's done to consumer expectations doesn't reverse overnight.

The real stories to watch this week: whether the ceasefire holds past its first 48 hours, how badly Friday's CPI reading surprises to the upside, and whether Broadcom's AI momentum can sustain the wider semiconductor sector through whatever comes next.

Tuesday was a day that ended better than it started. Wednesday could extend that recovery or remind us that geopolitical ceasefire announcements have a habit of lasting exactly as long as both sides find them convenient.

ChartMill Market Desk - Kristoff

This daily update is prepared by ChartMill for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.