Finding stocks with explosive growth potential is a goal for many investors, and one systematic way to identify them is by following the principles laid out in Louis Navellier's "The Little Book That Makes You Rich." The strategy focuses on eight fundamental rules designed to pinpoint companies with strong earnings momentum, expanding profitability, and solid financial health. In a market where the S&P 500's long-term and short-term trends are both positive, applying this disciplined, growth-oriented approach can help filter out the noise. Below, we examine how Five Below (NASDAQ:FIVE) stacks up against these criteria, using data from our screening process.

Recent Performance and Growth Metrics

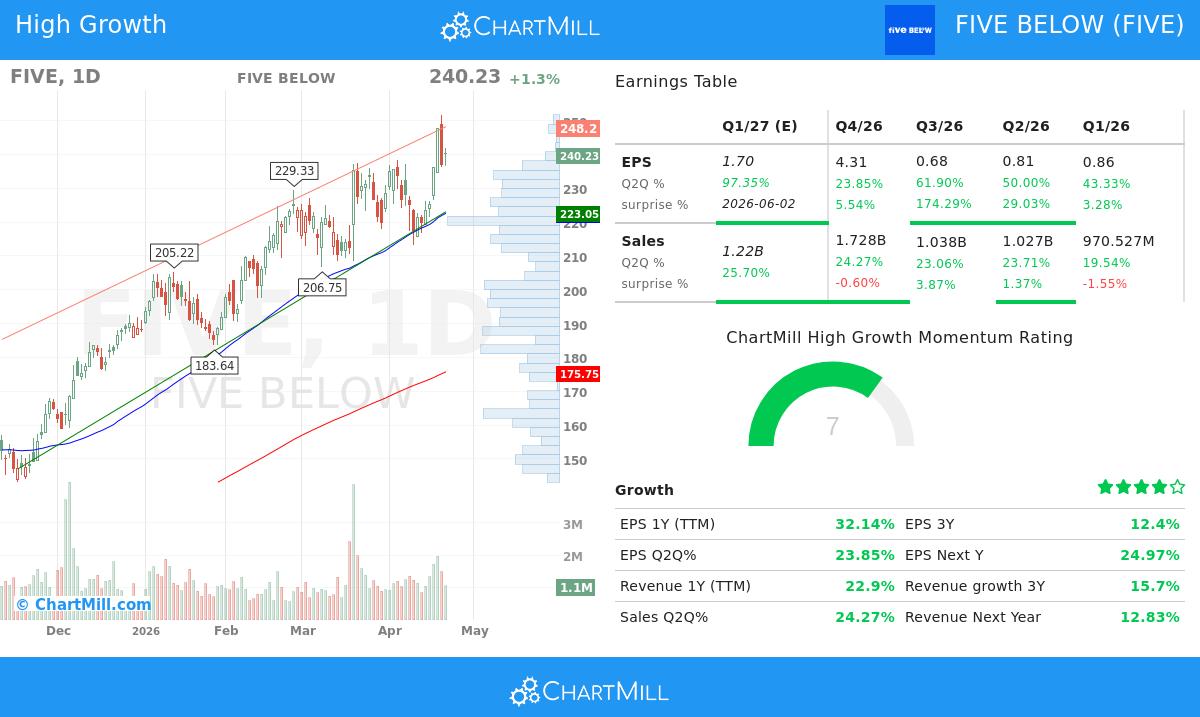

Five Below, a specialty value retailer, has demonstrated impressive growth across several key metrics that are central to the Navellier method. The strategy emphasizes both revenue and earnings growth as core drivers, and the numbers here are striking. The company’s revenue over the past trailing twelve months (TTM) grew by 22.90%, while its quarter-over-quarter (Q2Q) sales growth stood at 24.27%. This aligns directly with the third rule from the book, which requires at least 20% year-over-year and 20% quarter-over-quarter revenue growth.

Earnings performance is equally strong. The EPS over the past TTM grew by 32.14%, and the most recent Q2Q EPS growth was 23.85%. Both figures exceed the 15% thresholds set by the strategy for earnings growth and demonstrate positive earnings momentum. The book’s rule on earnings momentum also requires that the current Q2Q growth rate exceed the previous quarter’s rate. In this case, comparing the current Q2Q EPS growth of 23.85% to the value from four quarters ago (which was -4.66%) shows a clear acceleration, satisfying that requirement.

- Revenue Growth (1Y TTM): +22.90%

- Revenue Growth (Q2Q): +24.27%

- EPS Growth (1Y TTM): +32.14%

- EPS Growth (Q2Q): +23.85%

Earnings Revisions and Surprises

The strategy places heavy weight on positive earnings revisions and surprises, as these signal that analysts are becoming more optimistic about a company’s prospects. Five Below scores exceptionally well here. Over the last three months, analysts have revised the next quarter’s EPS estimate upward by an impressive 93.64%, easily surpassing the 4% hurdle set in the screen. Furthermore, the company has achieved earnings beats in each of the last four quarters, with an average beat percentage of 53.03%, far exceeding the 10% average required.

These figures validate that Five Below is consistently outperforming expectations, which should, in theory, force further upward revisions. As the book notes, when analysts revise estimates upward, it often drives share prices higher.

- EPS Next Quarter Revision (3 months): +93.64%

- EPS Estimate Beats (last 4 quarters): 4 out of 4

- Average EPS Beat (last 4 quarters): 53.03%

Profitability, Margins, and Cash Flow

Strong growth is meaningless if a company can’t control costs or generate cash. The Navellier method checks for expanding operating margins and strong free cash flow growth. Five Below’s operating margin has grown by 14.94% over the past year, well above the 2% minimum required. Free cash flow growth is even more striking, surging by 286% over the trailing twelve months, a massive leap from the 15% baseline. This shows that the company is not just growing sales but doing so with increasing efficiency and translating that into hard cash.

The overall financial health is solid, as reflected in the fundamental analysis report. With a Return on Equity (ROE) of 16.35% (exceeding the 10% minimum) and no outstanding debt, the company is in a strong position. The strategy’s final rule on high return on equity is comfortably met, and the company’s solvency and liquidity scores are top-tier.

Valuation and Analyst Views

While the company meets almost all growth and quality criteria, valuation remains a point of caution. The price-to-earnings (P/E) ratio stands at 36.07, which is expensive compared to the S&P 500’s average of 27.50. However, the forward P/E drops to 28.86, indicating that expected earnings growth may justify the premium. The PEG ratio suggests the price is fairly compensated for growth, and analysts forecast EPS growth of 15.39% per year going forward.

Summary of Fundamental Analysis

Our detailed fundamental analysis report gives Five Below an overall rating of 7 out of 10. The company scores 8 out of 10 for profitability and health, indicating strong margins and a solid balance sheet. Growth also scores 8 out of 10, reflecting past and expected future earnings increases. Valuation is the weak spot, scoring only 3 out of 10 due to a high P/E ratio, though the book’s approach often tolerates higher valuations for companies with superior growth.

Take Action

For investors interested in applying this strategy further, the screen used to find Five Below is available for review. It captures companies with accelerating sales, rising earnings, expanding margins, and strong analyst momentum. To see the full list of stocks currently passing these filters, you can explore the live results of the Little Book screen here.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Always conduct your own research and consider your financial situation before making any investment decisions.