For investors aiming to construct a portfolio using value investing principles, the central method involves finding companies trading for less than their inherent value. This systematic method, established by Benjamin Graham and notably used by Warren Buffett, demands attention to sound basics, solid financial condition, steady earnings, and acceptable expansion, all obtainable at a reduced cost. A "Decent Value" screen puts this into practice by selecting for stocks with high valuation scores, meaning they are priced low compared to their financial numbers, while also keeping acceptable scores in expansion, condition, and earnings. This mix tries to find possible chances where the market might be missing a company's true strength. One stock that recently appeared from this method is Equinor ASA-Spon ADR (NYSE:EQNR).

Valuation: The Foundation of the Idea

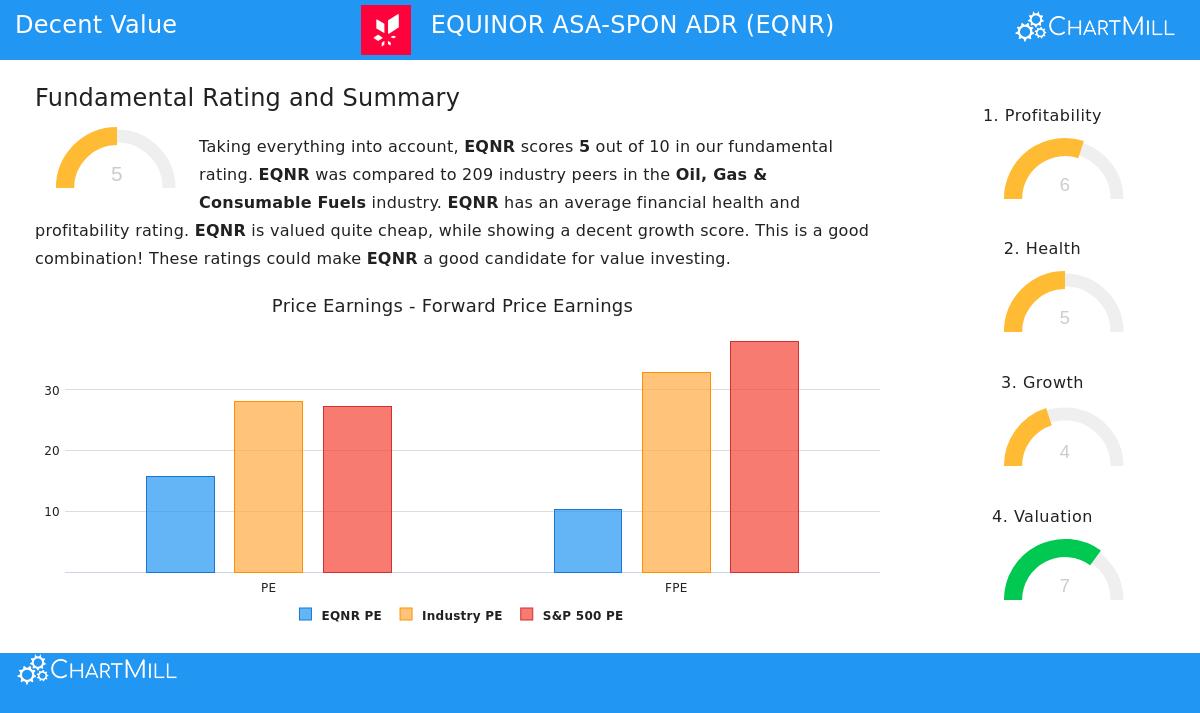

The main attraction of Equinor from a value view is its valuation numbers. The company's ChartMill Valuation Rating of 7 out of 10 shows it is priced well next to similar companies and the wider market. This score is based on several important ratios:

- Price-to-Earnings (P/E): At 15.68, Equinor's P/E ratio is under the industry average and much less expensive than the present S&P 500 average of 27.18.

- Forward P/E: An even more interesting number is the forward P/E of 10.31, which is less than about 82% of its industry rivals.

- Enterprise Value to EBITDA: This ratio, which includes debt, indicates Equinor is valued low in its sector, doing better than 99% of its peers.

For a value investor, these numbers are essential. They represent the "margin of safety" Graham stressed, buying at a cost low enough under a careful estimate of inherent value to allow for mistakes in study or unexpected market changes. Equinor's valuation picture indicates such a cushion may exist.

Financial Condition and Earnings: Evaluating the Base

A low-priced stock is only a sound investment if the company is fundamentally stable. This is where the "decent" ratings in condition and earnings become important, helping to steer clear of the feared "value trap" where a low cost signals lasting damage instead of short-term undervaluation.

Equinor's Financial Condition rating of 5 and Earnings rating of 6 show a steady, operating business. The company produces considerable cash flow, with a positive operating cash flow kept over the last five years. Its Return on Invested Capital (ROIC) of 21.37% is especially good, placing it with the top in the oil and gas industry and showing efficient use of capital. While its debt amounts and liquidity ratios match industry standards, the high ROIC next to its cost of capital confirms the company is producing real economic value, a central idea for any lasting investment.

Expansion and Dividend: The Driver and the Benefit

While pure value stocks occasionally lack active expansion, Equinor displays a varied but acceptable profile. Its Expansion rating of 4 shows a shift. In the past, the company has reported very good average expansion in Revenue and Earnings Per Share (EPS). More recently, however, EPS has declined, and future projections for both revenue and earnings are for small, single-digit expansion.

This tempered view is probably a reason for its low valuation. For a value investor, this is not always a bad point; it means the market is not accounting for strong future growth, possibly lowering downside risk. Also, Equinor adds to this with a good dividend yield of 3.91%, which is above both its industry and the S&P 500 averages. The dividend has a steady history of growth over the last ten years, giving shareholders a real return while they wait for a possible market reassessment.

Conclusion: A Prospect for the Value Portfolio

Equinor presents a case that fits a systematic value method. It is a large, well-known energy company with strong earnings and cash generation, trading at valuation multiples that suggest a notable discount to the market. The company's financial condition is sufficient, and it gives back a good part of its cash to shareholders through a reliable dividend. The screen that found it looked for stocks with good valuation and acceptable basics, exactly to locate chances where price and inherent value may be mismatched.

A full look at Equinor's fundamental study across all five groups, Valuation, Expansion, Earnings, Condition, and Dividend, can be seen in the full ChartMill Fundamental Report.

For investors wanting to use this "Decent Value" method to find similar possible chances, you can run the screen yourself to see the present results.

Disclaimer: This article is for information only and is not financial advice, a suggestion to buy or sell any security, or a support of any investment plan. The study is based on data given and screens run at a specific time. Investors should do their own complete research and think about their personal financial situation and risk comfort before making any investment choices. Past results do not guarantee future outcomes.