Trump and Netanyahu's reassuring remarks on the Iran conflict pulled oil prices back from multi-year highs and gave Wall Street a lifeline on Thursday, but the structural threat to the Strait of Hormuz remains very much alive.

Meanwhile, Micron's blockbuster results were overshadowed by an eye-popping capex pledge, and FedEx delivered a post-market earnings surprise that should have your attention heading into Friday's open.

Thursday told a story of two sessions.

In the morning, U.S. equity indices were tumbling close to 1%, crude was trading north of $100 a barrel, and investors - still digesting Wednesday's Fed rate decision - were bracing for another ugly close.

By the bell, the damage had been largely contained. What changed? A few carefully chosen words from Donald Trump and Benjamin Netanyahu.

Geopolitics Do the Heavy Lifting

The oil market did much of the work in stabilizing equities. WTI crude fell 2.4% to roughly $94 per barrel, triggered by statements from President Trump - who suggested the Iran "excursion" would end sooner than expected - and Israeli Prime Minister Netanyahu, who echoed similar optimism, claiming Iran had lost its capacity to produce rockets and enrich uranium.

That said, WTI had opened the session above $100 and Brent had briefly touched $119, which tells you just how stretched the risk premium had become in energy markets before the diplomatic commentary kicked in.

Netanyahu added that Israel would help the U.S. reopen the Strait of Hormuz, and Treasury Secretary Scott Bessent floated two additional pressure-release valves:

- releasing extra crude from the Strategic Petroleum Reserve

- and potentially lifting sanctions on Iranian oil, moves that could use Iranian barrels against Iran's own economic leverage in the near term.

As strategist Adam Crisafulli at Vital Knowledge put it succinctly,

"The U.S. and Israel may have won in a conventional sense, but there appears to be no military solution to reopening the Strait of Hormuz,"

adding that a diplomatic resolution remains elusive while little effort seems to be going into achieving one.

That is, in my view, the crux of the issue and the single biggest variable overhanging markets right now. The VIX, Wall Street's fear gauge, closed Thursday at 25.09, up 12.2% and marking its highest level in over two years, which tells you that the professional money is far from relaxed.

Indices: Damage Controlled, Not Eliminated

The Dow Jones Industrial Average and the Nasdaq ended the day 0.4% and 0.3% lower, respectively, a dramatically better outcome than the 1% declines markets were nursing in early trade. The S&P 500 slipped 0.28% to close at 6,606, with the Nasdaq Composite mirroring that drop to finish at 22,091.

On the macro data front:

- weekly jobless claims fell by 8,000 to 205,000, well below the 215,000 consensus

- the Philadelphia Fed's manufacturing index expanded further from 16.3 to 18.1

- new single-family home sales dropped nearly 18% month-over-month in January.

- Leading economic indicators also dipped 0.1% in the same period.

- The euro/dollar pair was trading at 1.1580 on Thursday evening

Energy Sector: The Obvious Winner

The sector arithmetic here is straightforward.

When Brent flirts with $119 and WTI tops $100, integrated oil majors print money upstream.

Exxon Mobil (XOM | +0.36%) and Chevron (CVX | +1.42%) have seen their share prices rally as expanding margins on every barrel produced outside the conflict zone flow straight to the bottom line.

Chevron's closing price on Thursday actually represented a new all-time high for the stock. Both energy majors closed up as much as 1.5%, a reasonable gain given the degree of caution prevalent across the rest of the market.

Alibaba: Strong Revenue Growth, Ugly Profit Picture

Alibaba (BABA | -7.09%) saw revenue grow in the most recent quarter but reported a sharp drop in net income. CEO Eddie Wu highlighted continued heavy AI investment, calling it one of the company's core pillars of growth.

The stock closed at $125.61, down from a previous close of $134.43, with intraday lows reaching as far as $121.16. Goldman Sachs and Bank of America, however, reiterated buy ratings, characterizing Thursday's drop as a buying opportunity given Alibaba's longer-term AI positioning and the strength of its underlying platform.

I'd lean toward that view cautiously, but the profit compression is a real concern that deserves monitoring over the next quarter or two.

Rivian: Uber Deal Puts the Stock Back on the Map

Rivian (RIVN | +3.80%) closed at $16.12 after announcing it will receive up to $1.25 billion from Uber to develop robotaxis for the market by 2028.

For a company that has faced persistent profitability concerns, this kind of strategic capital injection from a major mobility platform is exactly what the doctor ordered. It validates both Rivian's technology and its manufacturing roadmap and it keeps the autonomous vehicle narrative firmly in play.

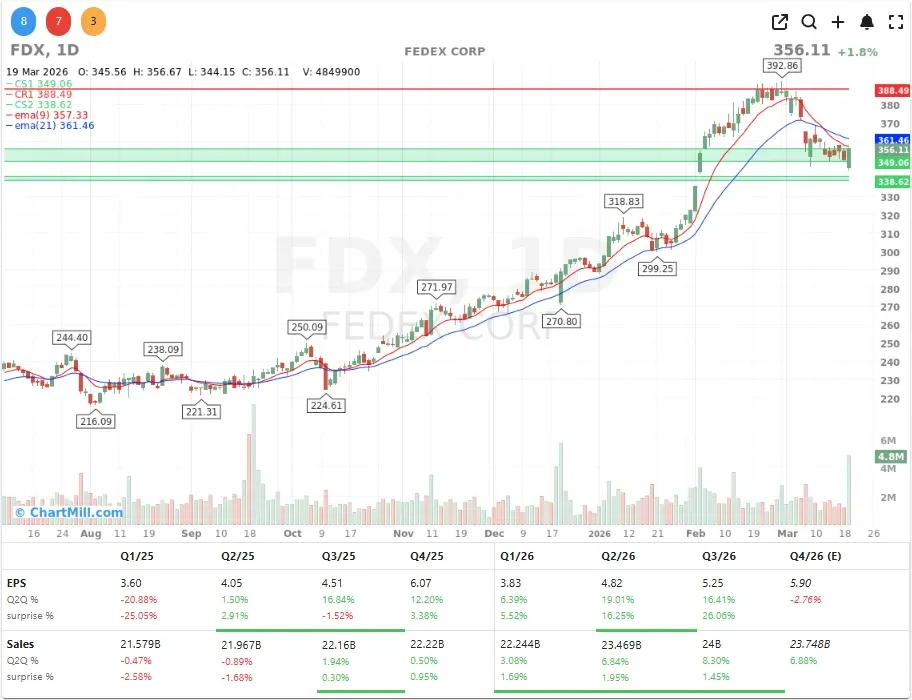

FedEx: The Post-Market Headline You Don't Want to Miss

Leave the best for last.

FedEx (FDX | +10.03% after-hours) posted strong Q3 results after the close, with revenue climbing from $22.2 billion to $24.0 billion year-over-year, beating the $23.5 billion consensus estimate.

Operating profit improved from $1.29 billion to $1.35 billion, and net income rose from $910 million to $1.06 billion. Adjusted earnings per share came in at $5.25, well above the $4.15 expected by the market.

For the full fiscal year 2026, FedEx raised its revenue growth outlook to 6.0–6.5% from the previous 5.0–6.0%, and increased its adjusted EPS guidance range to $19.30–$20.10, up from $17.80–$19.00. The stock had already gained close to 2% in the regular session but surged more than 10% in after-hours trading following the release, a move that deserves close attention at Friday's open.

On a side note, FedEx is part of a consortium that has bid €15.60 per share for Dutch-listed parcel locker company InPost, and the company expects the minority stake to be earnings-accretive from the first year. The Freight segment spin-off, set to list on the NYSE under the ticker FDXF, remains on schedule for June 1, 2026.

Conclusion

Thursday was a day where the headline narrative - geopolitical de-escalation talk - did most of the heavy lifting to prevent a meaningful market decline. But I remain skeptical that a few press conference soundbites are enough to structurally resolve what is a deeply complex situation around the Strait of Hormuz.

The VIX above 25 tells the real story: volatility is not going away quietly. For Friday's session, three names deserve your full attention: FedEx, which enters the day with serious post-market momentum; Micron, which may attract bargain hunters after Thursday's capex-driven pullback; and the energy sector, which continues to print new highs while the diplomatic picture remains murky at best.

ChartMill Market Desk - Kristoff

This daily update is prepared by ChartMill for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.

Next to read: Market Breadth Rebounds, But Conviction Is Still Missing