For investors seeking opportunities that combine solid growth with a reasonable price tag, the “Affordable Growth” strategy offers a useful framework. This approach screens for companies that demonstrate strong financial momentum—specifically a growth rating above 7 out of 10—while maintaining decent profitability and health, all without carrying an excessive valuation (a valuation score above 5). The goal is to identify stocks that are expanding their earnings and revenues at an attractive clip but haven’t yet been bid up to levels that erase future upside. Booking Holdings Inc (NASDAQ:BKNG) stands out as a strong candidate under this screen, given its solid fundamental profile and reasonable market pricing.

Growth Performance

Booking Holdings earns an impressive growth rating of 8 out of 10, reflecting both strong historical performance and promising forward estimates. Over the past year, earnings per share (EPS) grew by 20.84%, while the five-year average annual EPS growth clocks in at a remarkable 117.82%. Revenue also increased by 14.95% in the last year, with a five-year average of 31.69%. Looking ahead, analysts project EPS will continue expanding at an annual rate of 16.66%, with revenue growth of 8.75% per year.

This blend of past and future growth is a core pillar of the affordable growth strategy: a company that has proven its ability to scale earnings while still offering room for further expansion. The slight deceleration in revenue growth is a natural maturation pattern, but the absolute numbers remain strong compared to most peers in the Hotels, Restaurants & Leisure sector.

Valuation Metrics

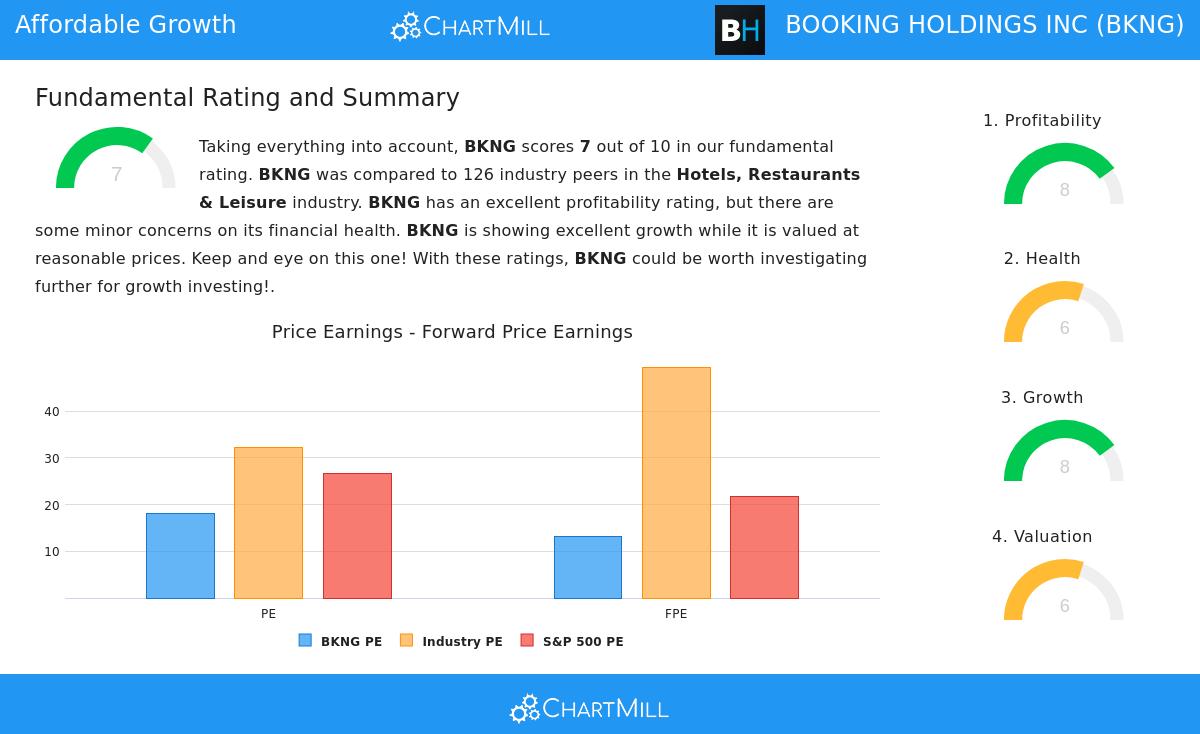

Despite its stellar growth trajectory, Booking Holdings is not priced at an extreme premium. Its current price-to-earnings (P/E) ratio of 18.12 sits below the S&P 500 average of 26.77, and 70.63% of industry peers trade at higher multiples. The forward P/E of 13.19 is even more attractive, indicating that expected earnings growth makes the stock look cheaper relative to near-term estimates.

The PEG ratio—which divides the P/E by the earnings growth rate—points to a reasonable valuation for the growth on offer. Additionally, the price-to-free cash flow ratio is lower than 81.75% of industry peers, further supporting the idea that the market has not fully priced in the company’s cash generation capacity. These valuation signals align with the screen’s requirement for a score above 5 (Booking gets a 6), ensuring that the strong growth doesn’t come at an unreasonably high entry point.

Profitability and Health

A growth stock can only deliver if the underlying business is financially sound. Booking Holdings scores an 8 out of 10 on profitability, supported by a return on assets of 22.20% and a return on invested capital (ROIC) of 97.86%—both among the best in its industry. The profit margin of 22.23% and operating margin of 34.99% also rank well above peers. This profitability is crucial for the affordable growth strategy, as it indicates the company can efficiently convert revenue into earnings, reducing the risk that future growth will be financed by debt or dilution.

The health rating of 6 out of 10 is solid, though not flawless. Booking holds an Altman-Z score of 6.49, far above the danger zone, and its debt-to-free-cash-flow ratio of 2.04 suggests it could pay off all debt in just over two years using available cash flows. However, the company’s debt-to-assets ratio has deteriorated slightly compared to a year ago, and its current and quick ratios are both near 1.06, which is adequate but not strong. For the affordable growth screen, these numbers are acceptable: a healthy but not squeaky-clean balance sheet still leaves room for the company to invest in future growth without being overleveraged.

Putting It All Together

Booking Holdings fits the affordable growth mold because it marries top-tier growth and profitability with a valuation that doesn’t penalize investors for chasing momentum. The business has a demonstrated ability to generate cash and returns, and its forward estimates suggest this trajectory will continue. For those employing the Growth At Reasonable Price approach, BKNG offers a rare combination of scale, efficiency, and reasonable pricing.

For a deeper look into the numbers and the full fundamental breakdown, you can explore the detailed fundamental analysis report.

Screening for More Affordable Growth Ideas

The Affordable Growth screen is a useful tool for identifying other stocks with a similar profile. It applies consistent filters across growth, valuation, health, and profitability to surface names that might otherwise fly under the radar. If you’re interested in discovering additional opportunities beyond Booking Holdings, click here to access the current Affordable Growth screen results and start your own research.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Always conduct your own due diligence or consult a financial professional before making investment decisions.