Bath & Body Works (NYSE:BBWI) is a specialty retailer known for its extensive range of fragrances for the body and home, including popular collections for candles, hand soaps, and body lotions. With over 1,890 company-operated stores in the U.S. and Canada, plus a growing international franchise network, the company has built a strong brand presence. For dividend-focused investors, the stock presents an interesting case, having been flagged by a screening strategy designed to identify top-tier dividend payers.

The screening method used to identify this security focuses on companies with a high ChartMill Dividend Rating, while ensuring they also possess decent profitability and financial health. The logic is straightforward: a high dividend yield is only attractive if it is sustainable and backed by a sound business. By requiring a minimum Dividend Rating of 7 out of 10, combined with a Health Rating of at least 5 and a Profitability Rating of at least 5, the screen filters out high-yield traps and focuses on stocks that can likely maintain or grow their payouts. Bath & Body Works passes these thresholds with a Dividend Rating of 8, a Profitability Rating of 7, and a Health Rating of 5.

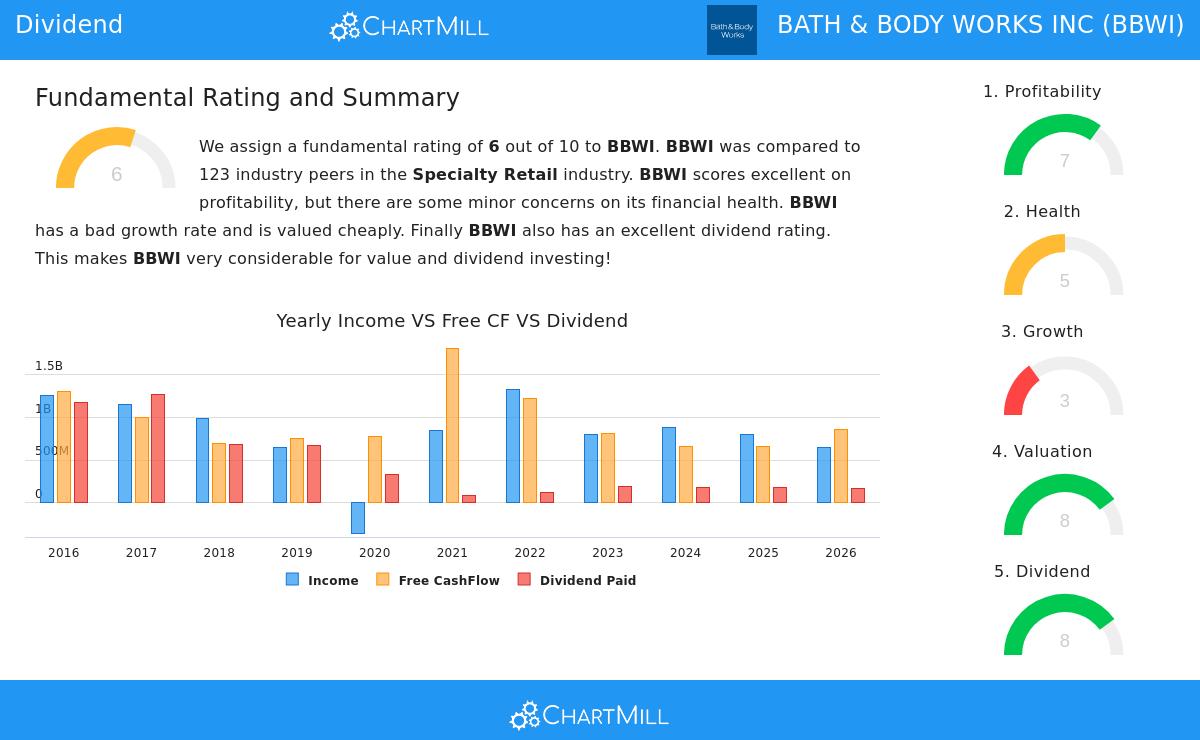

Dividend Strength

The primary appeal for dividend investors lies in the stock's strong dividend profile. Bath & Body Works offers a yearly dividend yield of 4.43%, which is significantly higher than both the industry average of 3.36% and the S&P 500 average of 1.81%. This places BBWI among the top dividend payers in its sector, outperforming nearly 88% of its industry peers in terms of yield.

Beyond the current yield, the company has a reliable history. It has paid a dividend for at least 10 years and has not decreased its payout over the past 5 years. Furthermore, the dividend has been growing at an average annual rate of 21.78%, which is a strong indicator of management's confidence in future cash flows.

A critical aspect of dividend sustainability is the payout ratio. BBWI pays out only 25.73% of its income as dividends, which is a very comfortable and sustainable level. This low payout ratio provides a substantial cushion, meaning the company can easily cover its dividend obligations even if earnings face temporary pressure. However, one cautionary note in the report is that earnings are currently growing slower than the dividend, which is a trend worth monitoring to ensure long-term sustainability.

Profitability and Health

A high dividend is only valuable if the underlying business is profitable and stable. The screening criteria ensures this by requiring a minimum Profitability Rating of 5, which BBWI exceeds with a score of 7 out of 10.

The company shows excellent profitability metrics:

- Return on Assets (ROA): 12.80% – outperforming 90% of industry peers.

- Return on Invested Capital (ROIC): 24.80% – outperforming 95% of industry peers.

- Operating Margin: 15.65% – among the best in the industry.

- Profit Margin: 8.90% – also well above the industry median.

These figures indicate that the company is highly efficient at turning its capital and assets into profit, which is a strong foundation for continued dividend payments. On the health front, Bath & Body Works scores a 5 out of 10, meeting the screen's minimum requirement. While not stellar, the company shows positive signs such as a decreasing debt-to-assets ratio and a healthy reduction in shares outstanding, which can boost per-share metrics over time. The Altman-Z score of 2.28 places it in the "grey zone," suggesting some risk but not immediate distress. The debt-to-free cash flow ratio of 4.50 is reasonable, indicating the company could pay off all its debt in about 4.5 years using its free cash flow.

Valuation Perspective

For value-conscious dividend investors, the valuation adds another layer of appeal. Bath & Body Works trades at a Price/Earnings (P/E) ratio of 6.16, which is substantially cheaper than the industry average of 23.34 and the S&P 500 average of 27.42. This low multiple, combined with a high dividend yield, creates an attractive value proposition. The stock is cheaper than nearly 96% of its industry peers based on the P/E ratio, and its Price/Forward Earnings ratio of 7.48 confirms a very cheap forward valuation.

You can review the full detailed breakdown of these fundamental scores in the Fundamental Analysis Report for Bath & Body Works.

Looking Ahead

While the current yield and valuation are attractive, investors should note the mixed growth picture. The company has experienced a slight decline in earnings per share over the past year (-2.10%) and a flat revenue trend. However, analysts expect a turnaround, with EPS projected to grow by 8.92% annually in the coming years, while revenue is expected to increase modestly by 2.25%. If these projections materialize, the dividend growth trajectory could become more sustainable.

For investors seeking a high current income stream from a well-known consumer brand at a cheap valuation, Bath & Body Works merits a closer look.

More Dividend Opportunities

This stock is just one example from a broader screening strategy designed to uncover top dividend stocks. The screen applies filters for a minimum average volume, a price above $10, and strong ratings for health, profitability, and dividend quality.

To explore the full list of stocks that pass this dividend-focused screen and to customize the filters to your own preferences, visit the Best Dividend Stocks Screener for more results.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Always conduct your own research and consider your financial situation before making any investment decisions.