For investors looking to balance the search for high-growth companies with fiscal discipline, the "Growth at a Reasonable Price" (GARP) method offers a middle ground. This method tries to find companies with strong and sustainable growth, but whose shares are not trading at very high prices. It avoids the high risks of speculative growth stocks and the potential traps of stagnant companies. One practical way to use this screen is with fundamental ratings that judge stocks on five main areas: Growth, Valuation, Health, Profitability, and Dividend. A stock like Alnylam Pharmaceuticals Inc (NASDAQ:ALNY), which recently appeared in an "Affordable Growth" screen, deserves a closer review under this method.

Notable Growth Measures

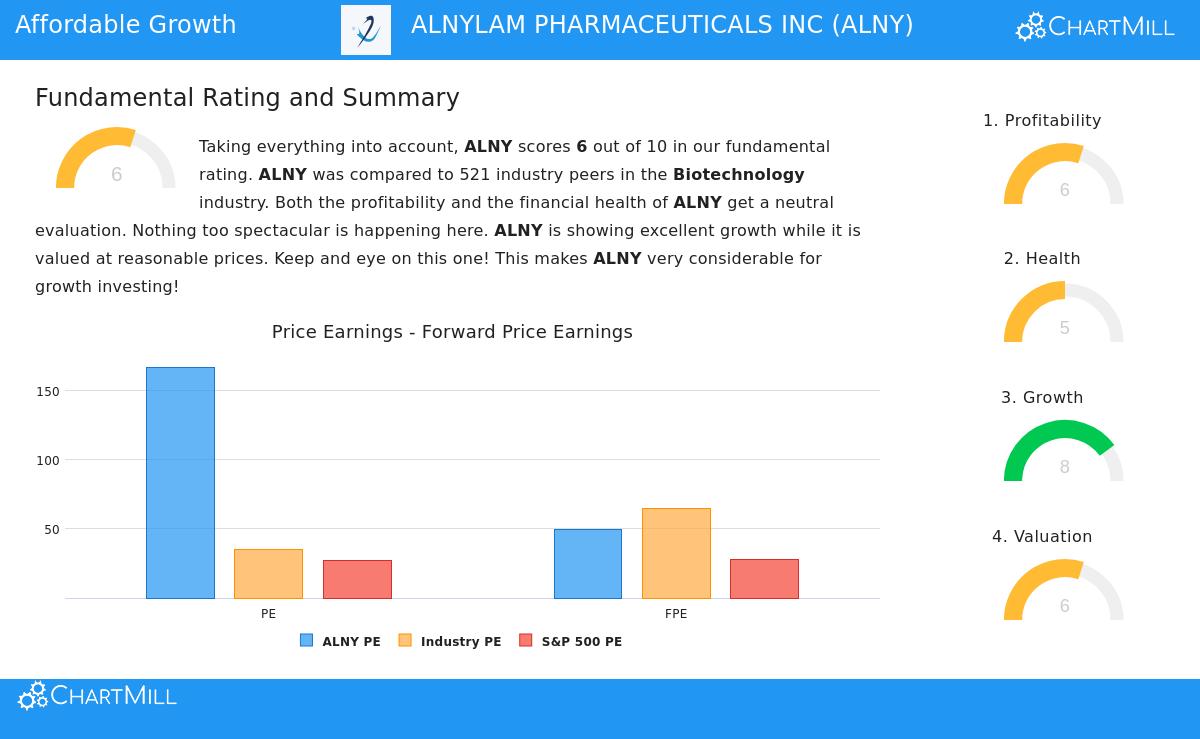

The central idea of any GARP method is growth. Alnylam’s fundamental report shows notable strength here, receiving a high Growth rating of 8 out of 10. The company is not just promising future potential; it is showing large expansion now.

- High Earnings Growth: Over the past year, Alnylam’s Earnings Per Share (EPS) rose by 191.24%, a clear sign of moving top-line success to the bottom line.

- Strong Revenue Growth: Revenue growth is also strong, increasing 65.19% in the last year and keeping a high compound annual growth rate of nearly 50% over recent years.

- Positive Forward View: Analyst expectations support this trend continuing, with predicted average annual EPS growth of over 70% and revenue growth above 23% for the next years.

This mix of recent performance and a positive forward view is what growth-focused investors look for. It shows a company successfully commercializing its pipeline and growing its business.

A Fair Valuation with Perspective

While growth is needed, the "reasonable price" part is what defines the GARP method and reduces risk. Alnylam’s Valuation rating of 6 shows a detailed picture that is clearer upon review. On the surface, traditional measures like a Price-to-Earnings (P/E) ratio of 167 look very high, especially compared to the S&P 500 average. However, biotechnology investing often needs a different view.

- Industry Comparison: Compared to other biotech companies, Alnylam’s valuation looks more fair. Its P/E ratio is lower than nearly 88% of the industry, and its forward P/E ratio of 49 is lower than almost 90% of others.

- Growth-Considered Measures: More important is the Price/Earnings-to-Growth (PEG) ratio, which includes expected earnings growth. Alnylam’s low PEG ratio suggests the current share price may be fair payment for its high projected growth.

- Cash Flow and EBITDA: Valuation numbers based on Enterprise Value to EBITDA and Price to Free Cash Flow also indicate Alnylam is priced more attractively than over 90% of its industry, pointing to efficiency in making cash from its operations.

For a GARP investor, this perspective is key. The valuation, while high alone, can be explained by the company's excellent growth rates and its position in a high-multiple sector.

Supporting Basics: Profitability and Financial Condition

A lasting growth story needs a solid base. Alnylam’s Profitability and Financial Condition ratings, both at a neutral 5 and 6, show there is space for progress but no clear warnings that would oppose the growth story.

- Profitability Positives: The company does well in key margin and return measures. Its Profit Margin (8.45%), Operating Margin (13.51%), and Return on Invested Capital (11.32%) all rank in the top ten percent of the biotechnology industry. This shows an ability to turn revenue into profit well.

- Financial Condition Notes: The company’s Altman-Z score shows low near-term bankruptcy risk. However, a Debt-to-Equity ratio above 3 shows a large use of debt financing, which is typical for capital-intensive biopharma companies but stays a point to watch. Liquidity ratios are enough to cover short-term needs.

These scores show why the screening rules require "decent" health and profitability. They work as a filter to make sure the growth is backed by operational efficiency and a balance sheet that can support it, stopping the choice of financially weak companies.

Summary and Next Steps

Alnylam Pharmaceuticals presents a strong example for the Growth at a Reasonable Price method. The company’s high revenue and earnings growth form the main investment thesis, while its valuation, though high alone, seems explainable compared to its industry and future outlook. The supporting basics in profitability and financial condition, while not perfect, give an adequate base for the growth story to go on.

For investors wanting to review other companies that match this balanced profile of strong growth, fair valuation, and decent underlying basics, more results from the "Affordable Growth" screen can be found here.

Disclaimer: This article is for information only and is not financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The analysis uses data and ratings from ChartMill, and investors should do their own research and talk with a qualified financial advisor before making any investment choices. Past performance does not show future results.