For investors aiming to assemble a portfolio of durable, well-managed companies for the long term, the principles of quality investing offer a useful framework. This method centers on finding businesses with lasting competitive strengths, solid profitability, sound financial condition, and the capacity for steady growth. The "Caviar Cruise" stock screen is built to methodically filter for these characteristics, using measurable data to locate companies that display the signs of quality. The screen highlights continued revenue and profit growth, strong returns on invested capital, reasonable debt, and high-quality earnings that become free cash flow.

One company that now meets this strict screen is ALLEGION PLC (NYSE:ALLE), a worldwide supplier of security products and solutions for homes, businesses, and institutions. Allegion's collection includes well-known brands such as Schlage, Von Duprin, and LCN, establishing it as a top participant in its sector. We will look at how Allegion matches the main elements of the Caviar Cruise quality investing method.

Matching the Central Standards for Quality

The Caviar Cruise screen uses several basic filters, and Allegion's financial picture meets or passes these marks.

-

Continued Growth: The method needs a minimum 5% compound annual growth rate (CAGR) for both revenue and EBIT (earnings before interest and taxes) over five years. This confirms the company is not static and is enlarging its main operations profitably.

- Allegion's 5-year revenue CAGR is 6.42%, showing steady top-line increase.

- More significantly, its 5-year EBIT CAGR is 8.89%, meaning that profits are increasing more quickly than revenue—a signal of better operational effectiveness and possible pricing strength.

-

Outstanding Capital Effectiveness: A core idea of quality investing is evaluating how effectively a company uses its capital to produce profits. The screen requires a Return on Invested Capital (excluding cash, goodwill, and intangibles) over 15%.

- Allegion's ROICexgc is a notable 52.96%. This high number implies the company produces significant profit from each dollar put into its business, a clear sign of a lasting competitive edge and very good management.

-

Sound Financial Condition and Cash Flow: Quality companies should not be weighed down by debt and must turn accounting profits into actual cash. The screen searches for a Debt-to-Free Cash Flow ratio below 5 and a 5-year average Profit Quality over 75%.

- Allegion's Debt/FCF ratio is 2.89, indicating it could pay off all its debt with under three years of present free cash flow, showing a very workable debt level.

- Its 5-year average Profit Quality is 95.55%, meaning almost all its reported net income becomes real free cash flow. This gives the financial freedom to put money back into the business, pay dividends, or buy back shares without needing outside funding.

A Summary of Allegion's Fundamental Picture

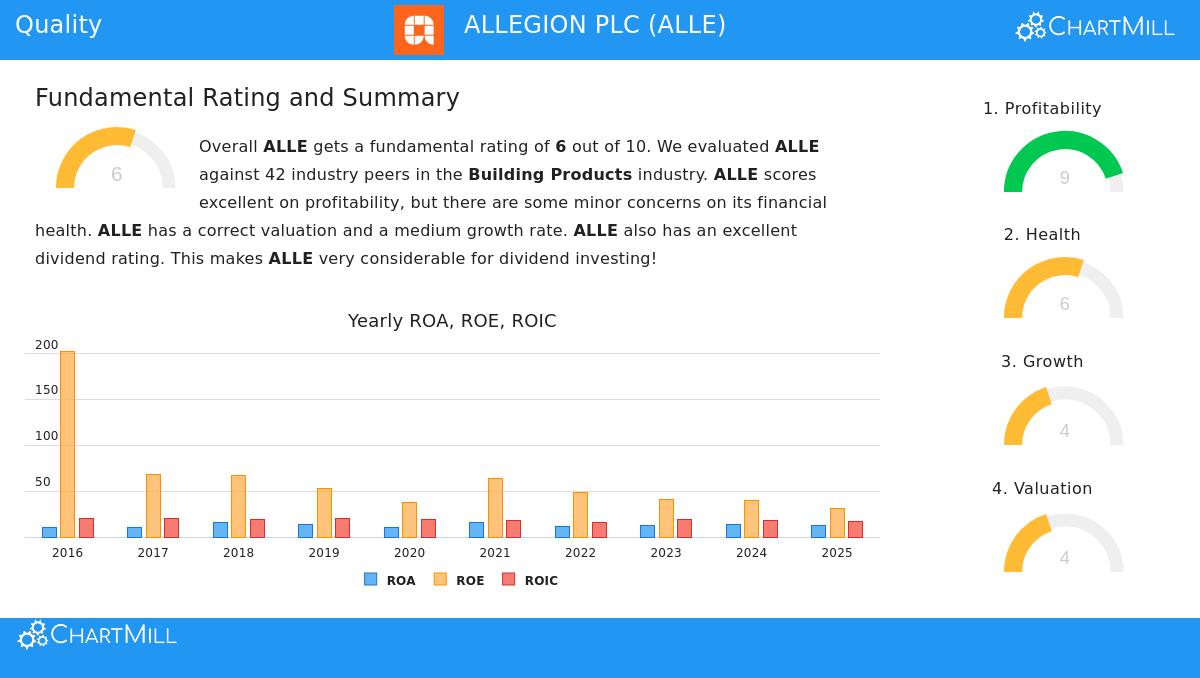

An examination of Allegion's detailed fundamental analysis report supports the results from the screen. The report gives Allegion a total score of 6 out of 10, with specific high points in profitability and dividends.

- Profitability is a clear high point, scoring a 9 out of 10. The company has sector-leading margins, with a Profit Margin of 15.83% and an Operating Margin of 21.13%, doing better than over 90% of similar companies in the Building Products industry. Its high Return on Equity (31.14%) further highlights effective use of shareholder capital.

- Dividend policy is consistent and increasing. Allegion has a 10-year history of reliably paying and raising its dividend, which now yields 1.51%. The yearly dividend growth rate of 9.79% is a good sign for income-focused quality investors.

- Financial Condition is good, with a score of 6. The company's Altman-Z score shows low bankruptcy risk, and its Debt-to-FCF ratio, as mentioned, is a positive. The primary point of attention is a Debt-to-Equity ratio of 0.96, which shows some use of debt financing, though it remains lower than many industry counterparts.

- Valuation and Growth are seen as average. With a P/E ratio near 17.5, the stock is not inexpensive but seems fairly priced compared to both the market and its own high profitability. Growth is anticipated to continue at a moderate speed, though analysts forecast a small slowdown from past rates.

Is Allegion a Quality Investment Prospect?

For investors using a quality-centered, buy-and-hold method, Allegion PLC makes a strong argument. It successfully passes a numerical screen created to find companies with better business models: it increases revenue and profits at a good rate, reaches very high returns on capital, keeps a solid balance sheet, and produces high-quality cash flows. These are the signs of a company with competitive strengths—in Allegion's situation, probably coming from its collection of reliable brands, technological advances in security and access control, and worldwide reach.

While price is always a factor and not a main filter in this screen, Allegion's present cost seems reasonable considering its solid profitability and financial soundness. It represents the kind of company a quality investor would aim to know well and possibly own for the long term.

Interested in reviewing other companies that meet the Caviar Cruise quality screen? You can locate the present list of passing stocks and use the screen yourself here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation to buy or sell any security, or an endorsement of any investment strategy. Investors should conduct their own research and consider their individual financial circumstances and risk tolerance before making any investment decisions.