For investors looking for a structured method for long-term wealth creation, the ideas presented by legendary fund manager Peter Lynch in One Up on Wall Street remain a relevant guide. His method, often described as Growth at a Reasonable Price (GARP), centers on finding companies with consistent, durable growth, sound financials, and a stock price that does not overvalue that future prospect. It is an approach that values fundamental business quality over short-term market movements, supporting a steady, long-term ownership mindset within a varied portfolio.

A recent filter using Lynch's essential measures has identified XPEL INC (NASDAQ:XPEL), a maker of paint protection films, window tints, and other automotive surface products. The company’s profile, which involves long-lasting, functional products for vehicles and buildings, matches Lynch’s liking for comprehensible businesses in possibly "ordinary" but necessary fields. Let's look at how XPEL measures up to the specific checks of the Lynch-inspired filter and what it could present for GARP-focused investors.

Matching the Lynch Measures

The filter uses a number of numerical rules meant to select for sound, expanding, and fairly valued companies. XPEL's present numbers show a solid match:

- Sustainable EPS Growth: Lynch wanted companies increasing earnings per share (EPS) between 15% and 30% each year over five years, thinking extremes on either side were troublesome. XPEL's five-year EPS growth rate of 23.0% rests well inside this preferred band, pointing to a strong and possibly maintainable expansion path.

- Fair Valuation via PEG: Maybe the central part of the GARP method is the Price/Earnings to Growth (PEG) ratio. A PEG at or under 1 implies the market is not overvaluing the company's expansion. XPEL's PEG ratio, calculated from its past five-year growth, is 0.94, meeting Lynch's condition and indicating a fair price relative to its historical growth.

- Sound Financial Health: Lynch stressed a very strong balance sheet. The filter demands a Debt/Equity ratio under 0.6, with Lynch himself favoring even smaller numbers. XPEL does very well here with a Debt/Equity ratio of 0.0, meaning it functions with no interest-bearing debt. Also, its Current Ratio of 3.25 is much greater than the filter's lowest acceptable figure of 1, showing sufficient cash to meet near-term needs.

- High Profitability: To confirm effective use of shareholder money, the strategy requires a Return on Equity (ROE) above 15%. XPEL's ROE of 18.3% passes this test, showing management is creating good profits from the equity put into the business.

A Broad Fundamental Look

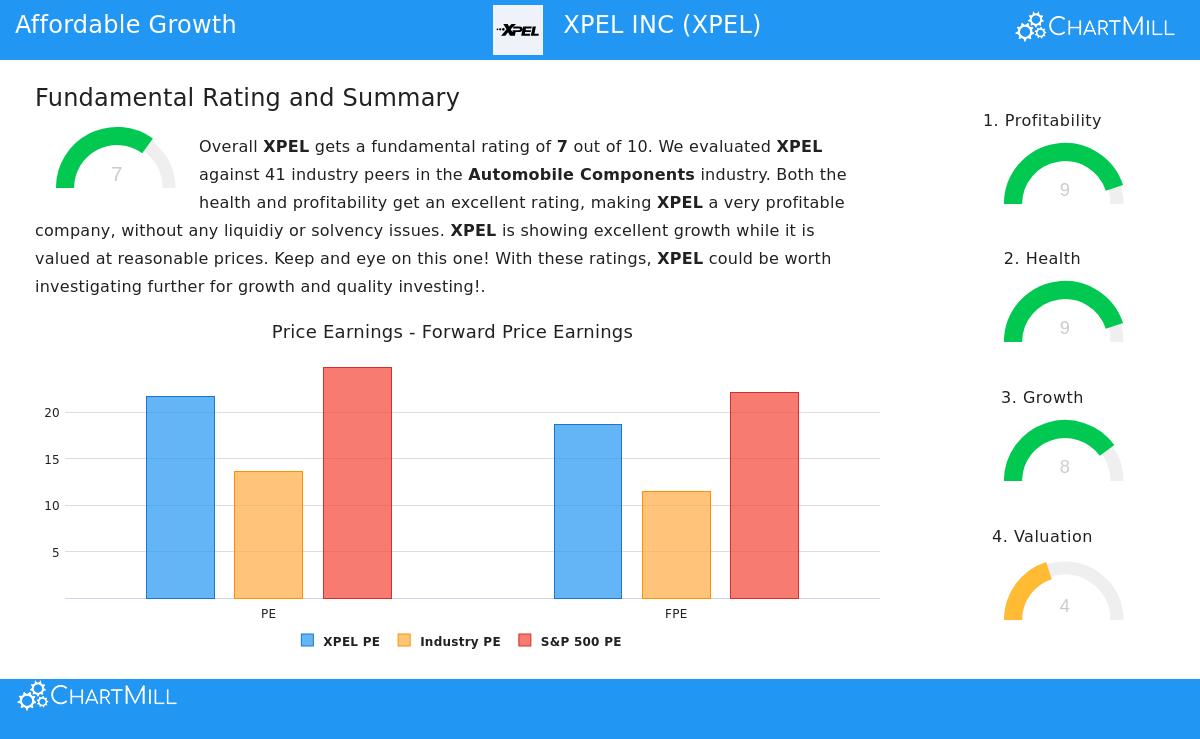

A closer look at XPEL's detailed fundamental report supports the image shown by the filter. The company receives an overall fundamental score of 7 out of 10, seen as positive, especially when measured against similar companies in the active Automobile Components field.

The report notes two strong areas: Profitability and Financial Health. XPEL gets a 9 out of 10 for profitability, having field-leading margins and returns on assets, equity, and invested capital (ROIC). Its health score is also a 9, pushed mainly by its absence of debt and a very high Altman-Z score, which almost removes short-term insolvency danger.

The Growth area is another positive, with a score of 8. The company has a confirmed record of good revenue and EPS increases and, notably, analysts forecast a rise in earnings growth to above 30% each year in the next few years. The primary area of average performance is Valuation, which scores a 4. While its P/E ratio is above the field average, this is mostly explained by its better profitability and growth picture, as seen in its acceptable PEG ratio.

Investment Case for the GARP Investor

For an investor using Peter Lynch's thinking, XPEL offers a relevant example. It works in a specialized but growing market, automotive aftermarket protection and architectural films, that is physical and clear. The company has shown it can expand at a quick but not excessive speed, all while keeping a clean balance sheet free of debt. This monetary restraint offers a notable buffer during economic slowdowns and allows management freedom to fund future expansion.

The Lynch filter successfully found a business that is not a speculative concept stock, but a financially established company performing its growth strategy well. The fair PEG ratio implies the market has not yet completely priced its future achievements into the present share price, giving a possible opening for investors with a long-term view. While the wider market direction is now unfavorable, Lynch’s method clearly recommends seeing past such near-term instability to concentrate on the basic business quality, which in XPEL’s situation seems firm.

Finding Other Possibilities

XPEL is one of a few companies that presently meet this strict group of filters. Investors curious about finding other possible choices that fit the Peter Lynch GARP method can examine the full filter findings here: View the Peter Lynch Strategy Screen.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. The analysis is based on data and a predefined filtering method. Investors should perform their own complete research and think about their personal financial situation and risk tolerance before making any investment decisions. Past performance is not indicative of future results.