In the world of long-term investing, few strategies have received as much respect as the one outlined by legendary fund manager Peter Lynch. His approach, often called Growth at a Reasonable Price (GARP), focuses on finding companies with solid, lasting growth paths that are not yet shown in very high stock prices. The central idea is to invest in clear businesses that show sound financial condition, high profitability, and a price that pays investors for the growth they are purchasing. This method avoids speculative trends for basic strength, looking for companies that can build value over many years rather than months.

A recent filter built on Lynch’s ideas has pointed to XPEL INC (NASDAQ:XPEL) as a possible choice for this kind of careful, long-term portfolio. The San Antonio-based company, a maker and seller of paint protection films, automotive window tints, and architectural glass solutions, works in a small but important part of the automotive and building aftermarkets. Its products, which protect and improve surfaces, match Lynch’s idea of a "simple" but needed business that consumers and companies depend on.

Fit with Peter Lynch Standards

The filter uses specific number-based rules taken from Lynch’s lessons to search for quality. XPEL’s financial picture shows a solid fit with these main points, which are made to find expanding companies without paying too much for that expansion or accepting too much financial danger.

- Lasting Earnings Expansion: Lynch preferred companies expanding earnings per share (EPS) between 15% and 30% each year, fast enough to be interesting, but slow enough to be lasting. XPEL’s five-year EPS expansion rate of 23.03% sits well within this target range, showing a record of solid, controlled growth.

- Fair Price via PEG Ratio: Maybe the most important Lynch number is the Price/Earnings to Growth (PEG) ratio, which tries to price a company next to its expansion rate. A PEG ratio at or under 1.0 suggests the market may not be completely valuing the future expansion. XPEL’s PEG ratio, based on its past five-year expansion, is 0.94, indicating a fair price when its historical expansion is examined.

- Sound Financial Condition: Lynch required companies with clear balance sheets. Two key rules are a Debt/Equity ratio under 0.6 and a Current Ratio above 1.0. XPEL does very well here, with a very small Debt/Equity ratio of about 0.0004, practically no debt, and a strong Current Ratio of 2.78, showing more than enough cash to cover near-term needs.

- High Profitability: Steady, high returns on equity (ROE) are a sign of a well-run business. Lynch searched for ROE above 15%. XPEL’s ROE of 17.35% not only meets this level but puts it in the high group of its industry, showing management’s skill in creating earnings from shareholder money.

Basic Condition Review

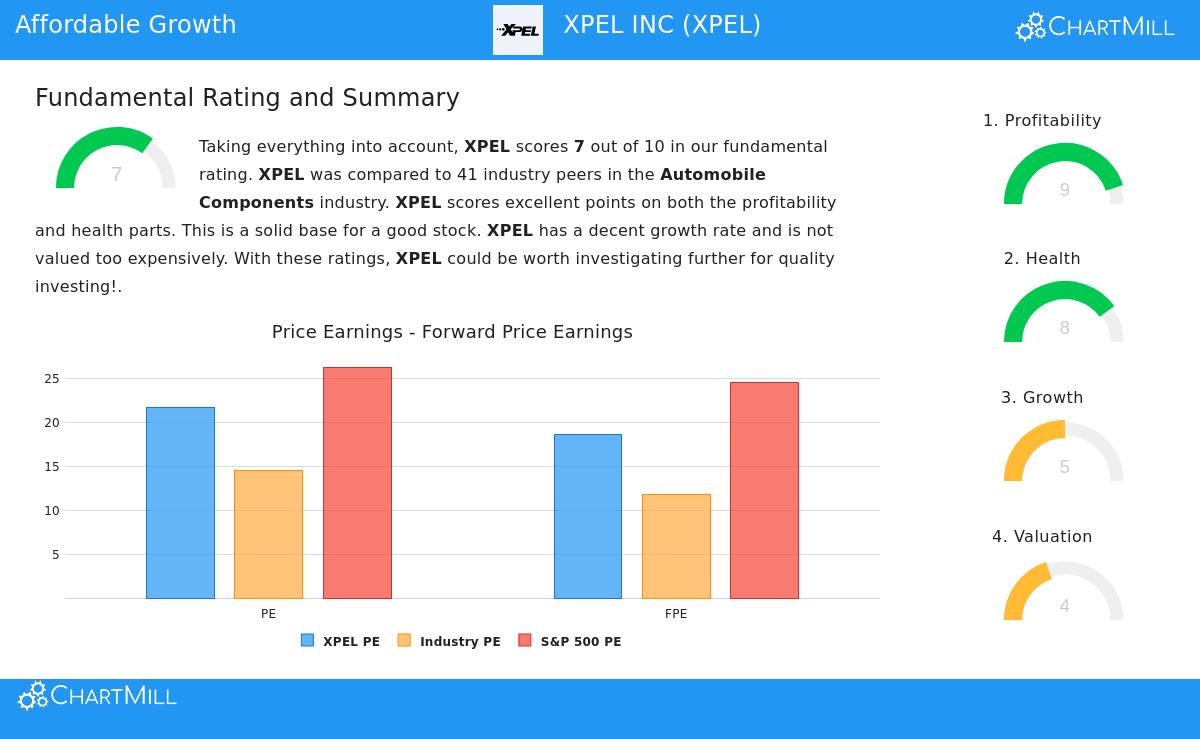

A wider fundamental analysis of XPEL supports the image shown by the Lynch filter. The company gets a high total basic rating of 7 out of 10, with especially high marks in Profitability (9/10) and Financial Condition (8/10).

The profitability review points out industry-leading margins and returns. XPEL’s profit margin of 10.12% and operating margin of 12.82% do better than most of its competitors in the automobile parts industry. Its return on invested capital (ROIC) of 15.61% further proves efficient use of capital.

On the condition side, the company’s clean balance sheet is a major positive. With no important debt, an Altman-Z score showing very little bankruptcy danger, and solid cash measures, XPEL has the financial strength that long-term investors value. This firm foundation gives stability during economic slowdowns and room to pay for future expansion projects.

The parts of Price (4/10) and Expansion (5/10) show a more varied, yet clear, image. The stock’s Price-to-Earnings ratio is above its industry average, which the report notes as "rather high." However, this is explained by the company’s better profitability and solid predicted future EPS expansion of over 30%. The "Expansion" score is limited by a medium past sales expansion rate, but experts forecast a speed-up in both sales and earnings going ahead.

A Choice for the Long-Term Investor

For an investor following the Peter Lynch method, XPEL offers an interesting example. It works in a clear, non-flashy area, the exact kind of business Lynch suggested studying. The company meets his strict rules for lasting historical expansion, fair price compared to that expansion, exceptional financial condition, and high profitability. While its current P/E number may make some strict value investors hesitant, the Lynch-focused PEG ratio and the company’s excellent balance sheet and margins give a reason for a higher price.

The filter that found XPEL is only the initial stage in Lynch’s process, a tool for creating study ideas. The following stage, which he stressed is key, requires non-number based careful checking: knowing the company’s competitive edge, the lasting need for its paint protection and window films, and the performance skill of its management group.

Interested in seeing other companies that match this careful growth-at-a-fair-price strategy? You can look at the present results of the Peter Lynch filter here.

Disclaimer: This article is for information only and does not make financial guidance, a suggestion, or an offer to buy or sell any security. Investing includes danger, including the possible loss of original money. Readers should do their own study and talk with a qualified financial advisor before making any investment choices.