Quality investing is not about chasing the cheapest stock or timing market swings. It’s about finding durable companies with strong competitive advantages, consistent growth, and the ability to compound capital over long periods. The Caviar Cruise stock screener, inspired by Luc Kroeze’s book "The Caviar Formula," is designed to surface exactly these kinds of businesses. The screen focuses on quantifiable criteria that indicate a company is not only profitable but also financially healthy, growing efficiently, and capable of turning earnings into real cash. Today, we’re looking at one company that passes this screen with strong marks: Watts Water Technologies Inc (NYSE:WTS).

Watts Water Technologies develops products for water conservation, safety, and flow control, serving residential, commercial, and industrial markets. With a market cap of roughly $6.5 billion and a history stretching back over a century, it represents the kind of mature yet growing firm quality investors tend to favor. The company has managed to combine steady revenue expansion with improving profitability, a solid balance sheet, and high returns on capital.

The Caviar Cruise Criteria and How WTS Measures Up

The Caviar Cruise screen applies several core filters designed to separate genuine quality companies from the rest. Each filter targets a specific aspect of financial health or performance that quality investors consider critical for long-term holding.

Revenue and Profit Growth Must Be Consistent

A quality company needs to show that its core business is growing. The screen requires a minimum of 5% annual revenue growth over five years and at least 5% annual EBIT (earnings before interest and taxes) growth over the same period. Even more important, the screen demands that EBIT growth outpaces revenue growth, which signals improving operational efficiency and pricing strength.

Watts Water Technologies clears these hurdles comfortably. Its revenue CAGR over the past five years is 6.9%, while EBIT CAGR comes in at a much stronger 19.6%. That EBIT growth is nearly triple the revenue growth rate, a clear indicator that the company is benefiting from economies of scale, cost management, or pricing strength—exactly what quality investors want to see. As the Caviar Cruise methodology notes, when EBIT grows faster than revenue, it suggests the firm is becoming more profitable over time.

High Return on Invested Capital (ROIC)

The screen uses a specific version of ROIC—excluding cash, goodwill, and intangibles—and requires a minimum of 15%. This metric is arguably the most important for quality investors because it measures how effectively a company deploys its capital to generate profits.

WTS posts an ROICexgc of 44.3%, far exceeding the 15% threshold. For context, a 44% return means that for every dollar of core invested capital, the company generates nearly 45 cents in profit. This level of efficiency is rare and strongly suggests the company has a sustainable competitive advantage. Quality investors are willing to pay a fair price for companies with this kind of capital efficiency because it signals that the business model is genuinely difficult to copy.

Manageable Debt Relative to Free Cash Flow

The screen limits the debt-to-free-cash-flow ratio to a maximum of 5. This ratio indicates how many years it would take for a company to repay all its debt using its current free cash flow. A low number means the company has ample financial flexibility.

Watts Water’s Debt/FCF ratio is 0.55—well within the acceptable range. In fact, it would take the company barely more than half a year of free cash flow to pay off all its outstanding debt. This gives WTS significant room to invest in growth, pay dividends, or weather economic downturns without financial strain. Quality investors value this kind of balance sheet discipline because it reduces risk over long holding periods.

Profit Quality: Turning Net Income Into Cash

The screen requires an average profit quality of at least 75% over five years. Profit quality is defined as free cash flow divided by net income. A high percentage means the company is converting its accounting profits into actual cash, which is essential for funding dividends, buybacks, or reinvestment without needing to borrow.

WTS posts a Profit Quality of 98.9% on average over the last five years. This is exceptionally high—nearly every dollar of net income turns into free cash flow. In many cases, a ratio close to 100% suggests a mature business that doesn’t require heavy reinvestment, but a closer look at CapEx relative to depreciation confirms that the company is still investing enough to grow. For quality investors, this combination of high cash conversion and reasonable reinvestment is ideal.

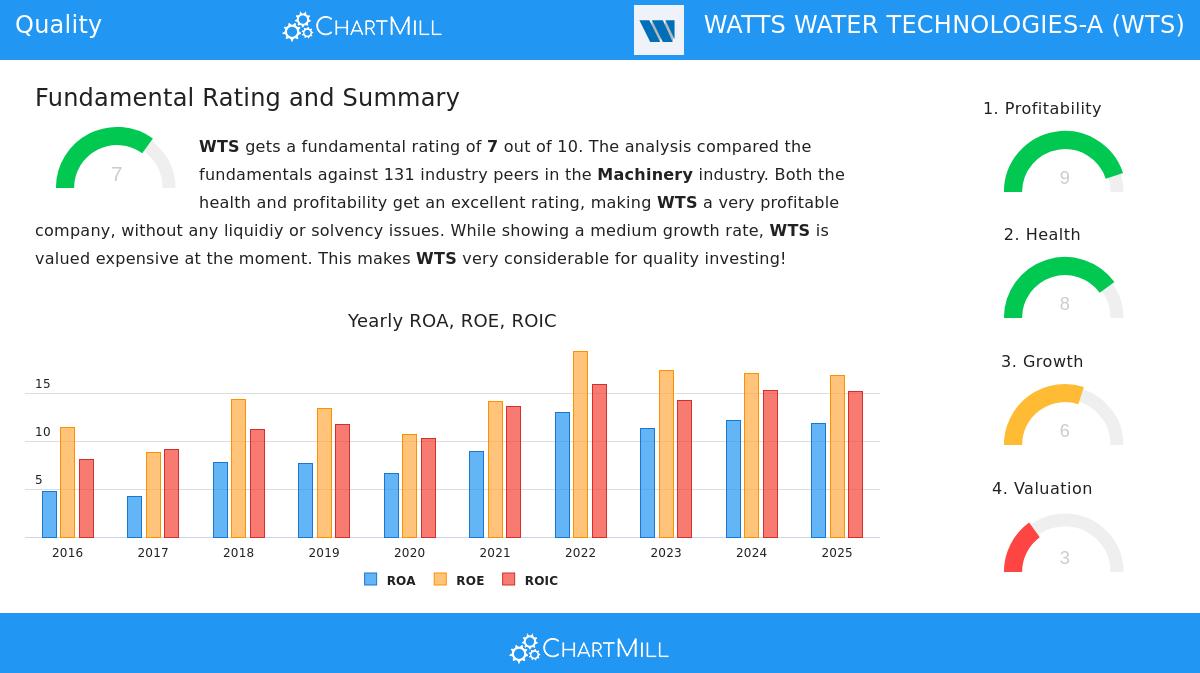

Fundamental Analysis Summary

According to our fundamental analysis report (link), Watts Water Technologies scores a solid 7 out of 10. The report highlights standout strengths in profitability and financial health, with the company outperforming roughly 90% of its industry peers on key metrics like ROIC, profit margin, and operating margin. The dividend yields only 0.68%, which is below average, but the dividend has grown at a 16.6% annual rate over the past decade and has never been cut in at least ten years. The main area of weakness is valuation: with a P/E ratio of 28.4 and a forward P/E of 25.4, the stock is not cheap. However, the report notes that the company’s outstanding profitability may justify the premium. Growth metrics are healthy, with historical EPS growth of 22.2% per year and expected forward EPS growth of 10.1%, though the pace of revenue expansion is expected to slow modestly.

Analyst Views and Valuation Context

Valuation is often the sticking point for quality stocks, and WTS is no exception. The Caviar Cruise screen does not include a valuation filter—quality investors are willing to pay a fair price for excellent businesses—but valuation should still be evaluated before any buy decision. At a P/E of 28.4, WTS trades in line with its industry average and slightly above the S&P 500’s current P/E of around 26.8. The PEG ratio (which adjusts P/E for expected growth) suggests the stock may be somewhat expensive relative to its near-term growth prospects. However, given the company’s high ROIC, strong cash conversion, and improving margins, many analysts see a reasonable case for the premium.

More Quality Opportunities

The Caviar Cruise screen is designed to filter for a select group of companies that combine profitability, health, and growth in a way that suits long-term buy-and-hold investors. Watts Water Technologies is a strong example, but the screen can uncover many other candidates. To explore the full list of stocks that meet these rigorous criteria, you can access the Caviar Cruise screener results directly [here](https://www.chartmill.com/stock/stock-screener?sid=673&f=sl_rev5y_5_X,sl_roicNg_15_X,sl_debt2fcf_X_5,sl_profitQ5y_75_X,sl_ebit5yGrowth_5_X,exch_us&v=22&s=ta&sd=DESC&cpl=2&bc=false&nw=1&o1=3&op1=200,16711680&o2=3&op2=50,255&o3=1&cf=(ebit5yGrowth%3Erev5y>).

Disclaimer: This article is for informational and educational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Always conduct your own research and consider consulting a financial professional before making any investment decisions.