For investors looking for a systematic, long-term method to accumulate wealth, few strategies hold the authority of Peter Lynch's approach. As explained in his book One Up on Wall Street, Lynch's thinking focuses on finding well-managed, expanding companies available at sensible prices, a concept often called Growth at a Reasonable Price (GARP). His method steers clear of speculative attempts to time the market, concentrating on fundamental business strength, maintainable expansion, and solid valuation. A primary instrument for applying this is a stock screener that sorts for particular financial measures, which lately found WILLIAMS-SONOMA INC (NYSE:WSM) as a possible candidate for more examination.

A Detailed Examination of the Lynch Criteria

The Peter Lynch screen uses a number of quantitative filters intended to separate companies with a distinct financial picture. Williams-Sonoma seems to satisfy these central requirements, which are basic to Lynch's trust in maintainable, comprehensible businesses.

- Maintainable Earnings Expansion: Lynch wanted companies expanding consistently, not violently. The screen calls for a 5-year average annual EPS growth between 15% and 30%. Williams-Sonoma's stated growth of 29.28% rests near the top limit of this span, pointing to a solid historical expansion path that Lynch would label as possibly maintainable, unlike extreme growth that is hard to continue.

- Sensible Valuation Compared to Growth: Maybe the most well-known Lynch measure is the PEG ratio (Price/Earnings to Growth), which he preferred at a value of 1 or below. This ratio modifies the standard P/E ratio for a company's expansion rate, trying to locate stocks that are not too expensive for their growth. Williams-Sonoma's PEG ratio, calculated from its last five-year growth, is stated at 0.68, suggesting its stock price could be sensible relative to its historical earnings increase.

- Sound Financial Condition: Lynch stressed investing in companies with strong balance sheets to endure economic declines. The screen requires a Debt/Equity ratio under 0.6 and a Current Ratio of at least 1. Williams-Sonoma performs very well here, stating no outstanding debt (a Debt/Equity of 0) and a Current Ratio of 1.43. This shows a very good financial situation with sufficient cash to cover immediate needs, matching exactly Lynch's liking for financially stable companies.

- High Profit Generation: To guarantee effective use of shareholder money, the screen selects for a Return on Equity (ROE) above 15%. Williams-Sonoma's ROE of 53.45% is unusually high, indicating the company is very skilled at creating earnings from its equity foundation, a primary sign of management skill and a competitive advantage.

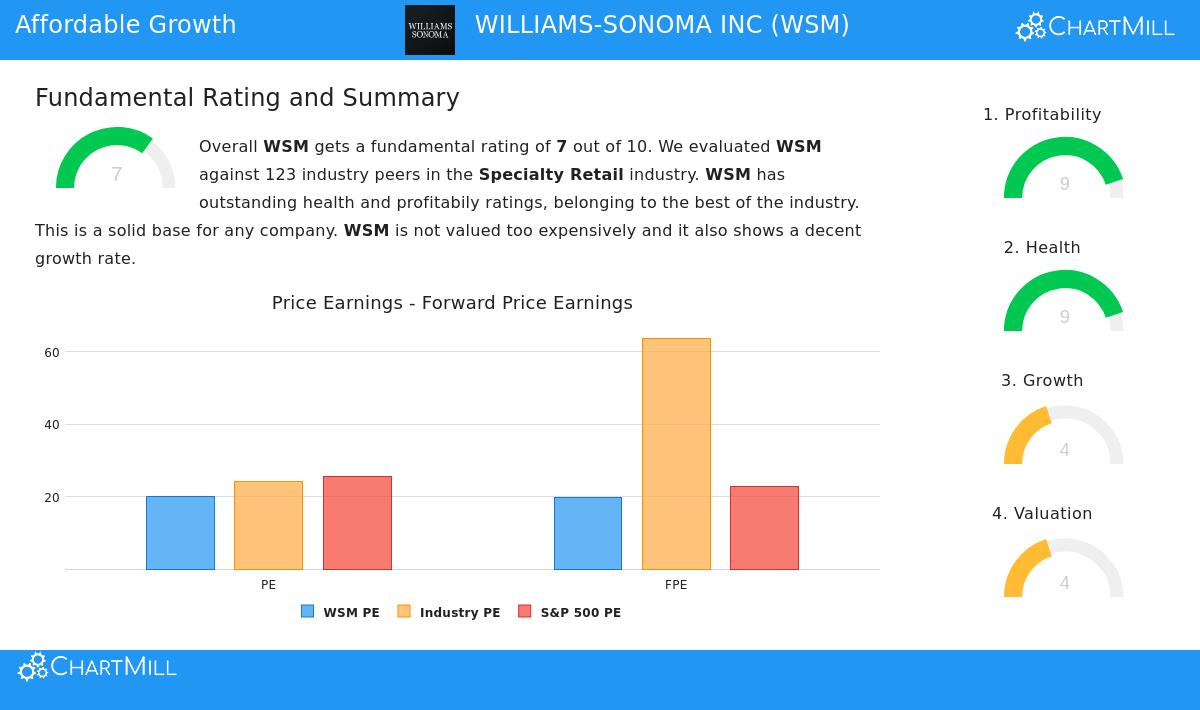

Fundamental Analysis Summary

A wider fundamental analysis of Williams-Sonoma supports the image shown by the Lynch screen. The company receives a high total fundamental score, pushed by two prominent parts: outstanding profit generation and very good financial condition.

The profit generation examination shows sector-leading margins and returns. The company's operating margin above 18% and its return on invested capital (ROIC) above 31% are much better than most of its competitors in the specialty retail industry. This indicates an ability to set prices and operational effectiveness. The health score is supported by the total lack of debt and a solid Altman-Z score, showing very little chance of bankruptcy.

The expansion score is more average, recognizing that while past EPS growth has been solid, future projections are for a more gradual, single-digit rate. This slowing is an item for investors to note, as Lynch preferred maintainable models. The valuation score is not uniform; while the P/E ratio is less expensive than many industry competitors, the forward P/E and PEG ratios using future growth projections indicate the market may have already accounted for much of the company's high-quality nature.

Is It a Foundational Investment?

Williams-Sonoma makes a strong case for investors who follow the GARP thinking. It works in the comprehensible, common area of home goods, a sector Lynch might like for its physical nature. The company meets the quantitative Lynch filters very well, displaying a record of solid growth combined with a perfect balance sheet and exceptional profit generation. These are the characteristics of a financially strong business.

Nevertheless, consistent with Lynch's principles, the screener is only a first step for non-quantitative investigation. Investors need to evaluate whether the company's brands, such as Pottery Barn and West Elm, can keep their attraction and pricing ability in a competitive retail environment, and if the projected decrease in expansion is a short-term phase or a lasting condition. The present valuation indicates the market sees its quality, allowing less room for mistakes.

Find Other Possible Candidates

Williams-Sonoma is one of multiple companies that presently meet the systematic filters of the Peter Lynch strategy. For investors aiming to construct a varied collection of fundamentally healthy expanding companies, inspecting the complete list of screen outcomes can supply a good investigation list. You can view the present results of the Peter Lynch screen here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any securities. The analysis is based on provided data and a specific investment strategy model. Investors should conduct their own thorough research and consider their individual financial circumstances before making any investment decisions.