For investors looking for chances where the market price may not completely show a company's actual value, a methodical value method can offer a structure. This process involves searching for companies that seem fundamentally healthy but are priced below their true worth, using numerical financial measures. The aim is to find businesses with good balance sheets, steady earnings, and acceptable expansion possibilities that are currently priced cautiously by the market, possibly giving a buffer for those investing over a long period.

One company that recently appeared from such a search process is Winnebago Industries (NYSE:WGO), a top producer of recreational vehicles and marine products. By using filters that focus on a good valuation rating together with acceptable scores in earnings, financial condition, and expansion, WGO comes forward as a candidate needing more review for its possibility as a lower-priced stock.

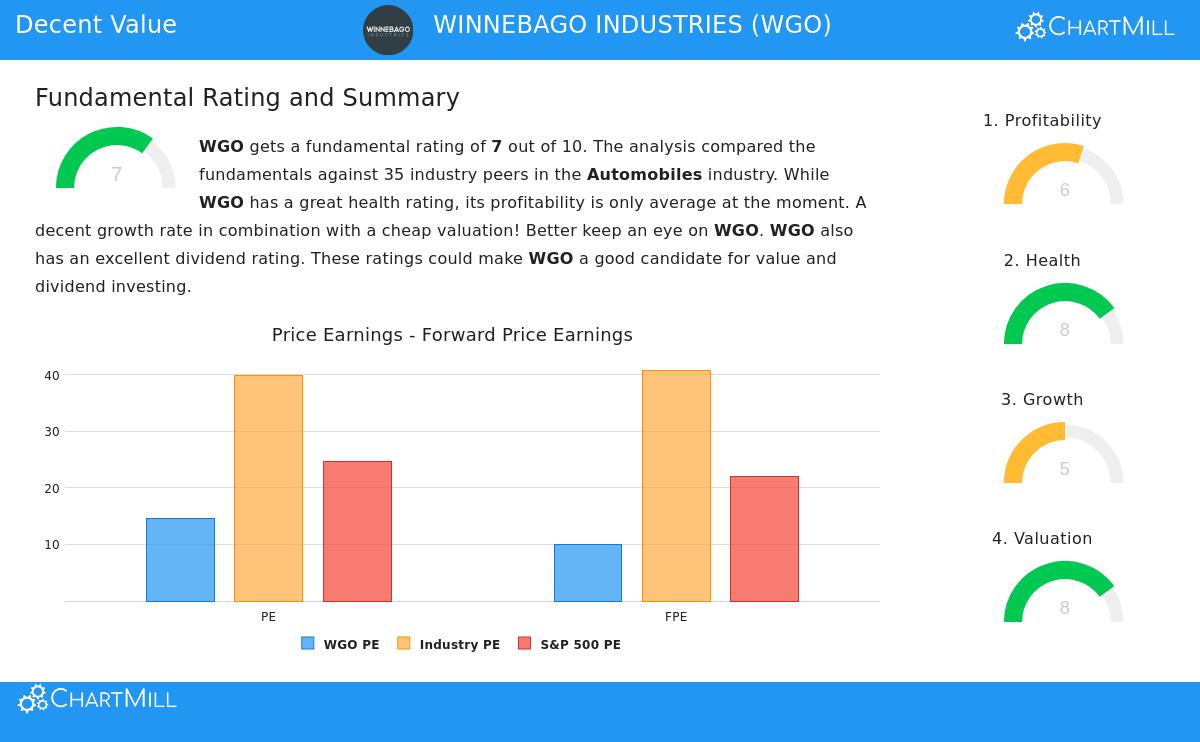

Valuation: An Attractive Entry Point

The central idea of value investing is buying a dollar's worth of assets for fifty cents. Winnebago's current valuation measures suggest the market may be giving such a lower price. According to its fundamental analysis report, the company gets an 8 out of 10 on valuation, showing it is priced well compared to both its own basics and similar companies.

- Price-to-Earnings (P/E): WGO is priced at a P/E ratio of 14.54, which is lower than 80% of its industry competitors and much below the S&P 500 average.

- Forward P/E: The view gets better when looking forward, with a forward P/E of 10.02. This is lower than over 82% of the industry and hints the market has set very low expectations.

- Enterprise Value/EBITDA & Price/Free Cash Flow: On these wider valuation measures, Winnebago is valued lower than 82.86% and 94.29% of its industry, in turn, pointing out a notable discount to cash flow creation.

For a value investor, these measures are the beginning. They show that even if the company's expansion is average, an investor is getting its earnings and cash flow at a cost below most rivals, creating a possible buffer against loss risk.

Financial Condition: A Solid Base

A low-priced stock is only a good investment if the company is financially stable. A good balance sheet is essential for value methods, as it gives strength during economic declines and lowers the chance of a poor investment. Winnebago's financial condition rating is a strong 8 out of 10.

- Solvency: The company shows low need for debt funding, with a Debt-to-Equity ratio of 0.36, more favorable than 71% of its industry. Its Altman-Z score of 3.60 shows no short-term bankruptcy danger and is better than 94% of peers.

- Liquidity: With a Current Ratio of 2.30, Winnebago has a good ability to meet near-term needs, performing better than 88% of the industry. This liquidity gives operational room to maneuver.

- Shareholder Alignment: Management has been lowering the count of shares available over the past one and five years, a move that can raise ownership for continuing shareholders over time.

This financial strength is key. It means the company has the endurance to handle industry cycles, which is particularly important for a business linked to consumer optional spending.

Earnings and Expansion: Driver for Value Achievement

While very low price can sometimes mean buying troubled companies, the best candidate also shows a capacity to make profits and expand. Winnebago's earnings rating is a good 6, and its expansion rating is a 5. The point for value investors is that the current low price is not just a sign of permanent drop.

- Earnings Strength: The company has been regularly profitable with positive earnings and operating cash flow for the past five years. Its Return on Invested Capital (ROIC) of 2.60% is with the best in its industry, better than 85% of peers, which shows effective use of capital.

- Earnings Path: While past earnings per share (EPS) have had some movement, the future appears more positive. Analysts predict a very good EPS expansion of over 43% on average per year in the coming years. This predicted rise is a good sign that the company's work may be building momentum.

- Dividend Support: Adding to the value case, WGO has a dividend yield of 3.04%, which is better than both its industry and the wider S&P 500 average. The dividend has a steady 10-year history of growth and no cuts.

The mix of acceptable current earnings, a high predicted earnings expansion rate, and a shareholder-friendly dividend policy suggests that if the company performs on its plans, the market may need to price the stock higher, reducing the difference between price and seen true value.

Conclusion and Investor Points

Winnebago Industries presents an example in how value search standards can find possible chances. It is priced at a clear discount to the market and its sector based on normal valuation measures. This discount exists together with a financially sound balance sheet that gives stability and a business that is predicted to go back to notable earnings expansion. The good dividend yield offers investors a return while they wait for a possible price adjustment.

It is important to see the setting. The recreational vehicle industry moves in cycles and reacts to consumer sentiment and loan costs. The company's high dividend payout ratio is also a point for watching. However, for investors using a value method that looks for quality companies at fair prices, WGO's profile, marked by low valuation, good financial condition, and bettering expansion outlook, makes it a stock deserving of more review.

This review of Winnebago Industries was found using a methodical search process. Investors wishing to find other companies that fit similar standards of good valuation, acceptable earnings, condition, and expansion can view more outcomes through this "Decent Value" stock screen.

Disclaimer: This article is for information only and does not make up financial guidance, a suggestion, or an offer or request to buy or sell any securities. The information given is based on data thought to be dependable but is not assured. Investors should do their own separate study and talk with a qualified financial advisor before making any investment choices. Past results are not a guide for future outcomes.