For investors looking to balance the search for growth with fiscal care, the Growth at a Reasonable Price (GARP) or "affordable growth" method offers a practical middle path. This method tries to find companies that are increasing their earnings and sales at a good rate and are also priced at levels that do not assume flawless execution. By looking for stocks with good growth basics, steady earnings, firm financial positions, and acceptable prices, investors can try to lessen some of the dangers that come with pursuing high-growth stocks in volatile markets. One company that recently appeared from this sort of search is Vertex Pharmaceuticals Inc (NASDAQ:VRTX).

Growth at the Center

The base of any affordable growth pick is, expectedly, its growth path. Vertex Pharmaceuticals shows firm growth traits, receiving a ChartMill Growth Rating of 7 out of 10. The company’s recent results are especially notable, with Earnings Per Share (EPS) rising by a remarkable 6248.28% over the last year. While this number is affected by a year-ago comparison, it points to a strong earnings turnaround. More significantly, the core trend is firm:

- Historical Growth: The company has recorded an average yearly EPS growth of 12.27% and revenue growth of 14.10% over recent years.

- Future Expectations: Analysts expect this pace to persist, with estimated forward yearly growth rates of 12.36% for EPS and 10.31% for revenue.

This steady and expected double-digit growth in both earnings and sales is a main support for its label as a growth stock. For the GARP method, such reliable and good growth is needed to support the current share price and allow for future gains.

Valuation: Acceptable Within a High-Valued Sector

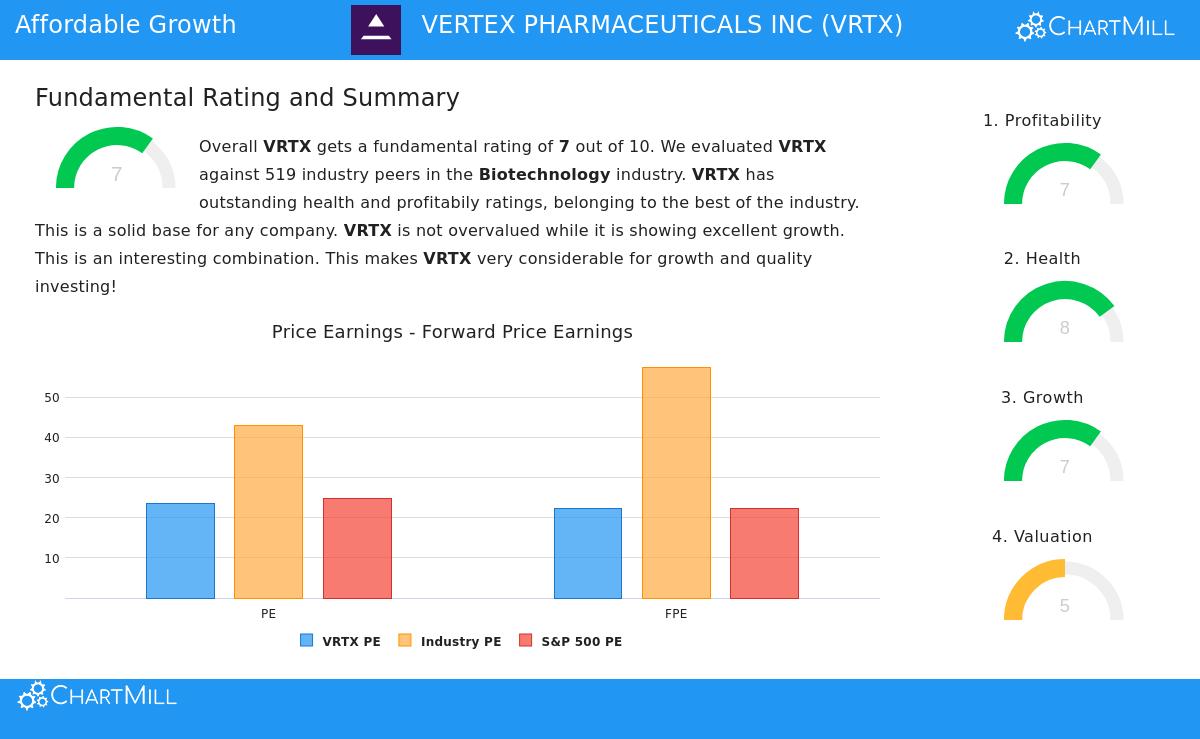

Where many high-growth biotech companies trade at very high prices, Vertex’s valuation shows a more moderate case, scoring a 5 on ChartMill’s Valuation Rating. The review shows a varied but finally positive view when considered next to its industry.

- Peer Comparison is Important: Vertex’s Price-to-Earnings (P/E) ratio of 23.52 and Forward P/E of 22.34 are seen as high on their own. However, next to its biotechnology peers, these multiples look acceptable. The stock is priced lower than over 92% of its industry based on its P/E ratio and lower than over 93% based on its Forward P/E.

- Cash Flow and EBITDA Measures: The valuation view improves when examining cash-based measures. Vertex’s Enterprise Value to EBITDA and Price to Free Cash Flow ratios are priced lower than about 93% of the industry, suggesting the market may be pricing its large cash generation fairly.

This comparative valuation is important for the affordable growth search. It looks for companies where the growth potential is not already completely—and overly—reflected in the stock price, providing a possible buffer that pure growth investing frequently misses.

Supporting Basics: Strength and Earnings

A growth prospect built on weak finances is a dangerous idea. The affordable growth method specifically looks for acceptable strength and earnings to avoid such issues. Vertex does well here, which supports the investment case.

- Very Good Financial Strength (Rating: 8): The company’s financial position is very strong. With an Altman-Z score of 12.07 showing very little bankruptcy risk and a very small Debt-to-Equity ratio of 0.01, Vertex works with minimal debt. Its debt-to-free-cash-flow ratio of 0.03 is very good, meaning it could pay off all its debt in just over a week from its cash flow. This financial power gives it stability and room to fund its research without weakening shareholder value.

- High Earnings (Rating: 7): Vertex is not just growing, it is highly profitable. It has a Return on Invested Capital (ROIC) of 16.99%, doing better than nearly 97% of its industry, which points to efficient use of money. Its operating margin of 39.04% and profit margin of 32.94% are also high within the biotech sector. Good earnings confirm the business model and make sure that sales growth turns into bottom-line profits for shareholders.

These points are essential for a lasting GARP investment. They make sure the company has the operational soundness and financial steadiness to handle difficulties and keep funding its growth projects.

Conclusion and Next Steps

Vertex Pharmaceuticals shows a strong profile for investors focused on the affordable growth category. It joins a clear and good growth story in its core cystic fibrosis business and future pipeline with a valuation that, while not low-price cheap, is acceptable compared to its high-growth, high-margin industry group. This is supported by a very strong financial position and better earnings measures, lowering basic risk.

The company’s full basic analysis report, which covers these scores across growth, valuation, strength, and earnings, can be seen here.

For investors aiming to create a list of similar options, the "Affordable Growth" search that found Vertex can be a helpful beginning. You can look at more stocks that fit these needs of good growth, acceptable valuation, and firm basic finances through this link.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer or request to buy or sell any securities. The information given is based on supplied data and should not be the only reason for any investment choice. Investors should do their own complete research and talk with a qualified financial advisor before making any investment decisions. Past results do not guarantee future outcomes.