For investors looking for chances where the market price may not completely show a company's true worth, a methodical screening process can help find possible candidates. One such way is to look for stocks that show good fundamental condition and earnings power, yet trade at prices that seem fair or even low compared to their sector and the overall market. This idea fits with basic value investing rules, which concentrate on finding good businesses selling for less than their calculated value, offering a buffer. A "Decent Value" screen that selects for good valuation marks together with firm marks in earnings power, financial condition, and expansion can reveal these kinds of chances.

One stock that recently came from a screen like this is Visteon Corp (NASDAQ:VC), a worldwide automotive technology firm focused on cockpit electronics and battery management systems. According to a fundamental analysis report from ChartMill, Visteon shows an interesting profile that deserves more attention from investors focused on fundamental value.

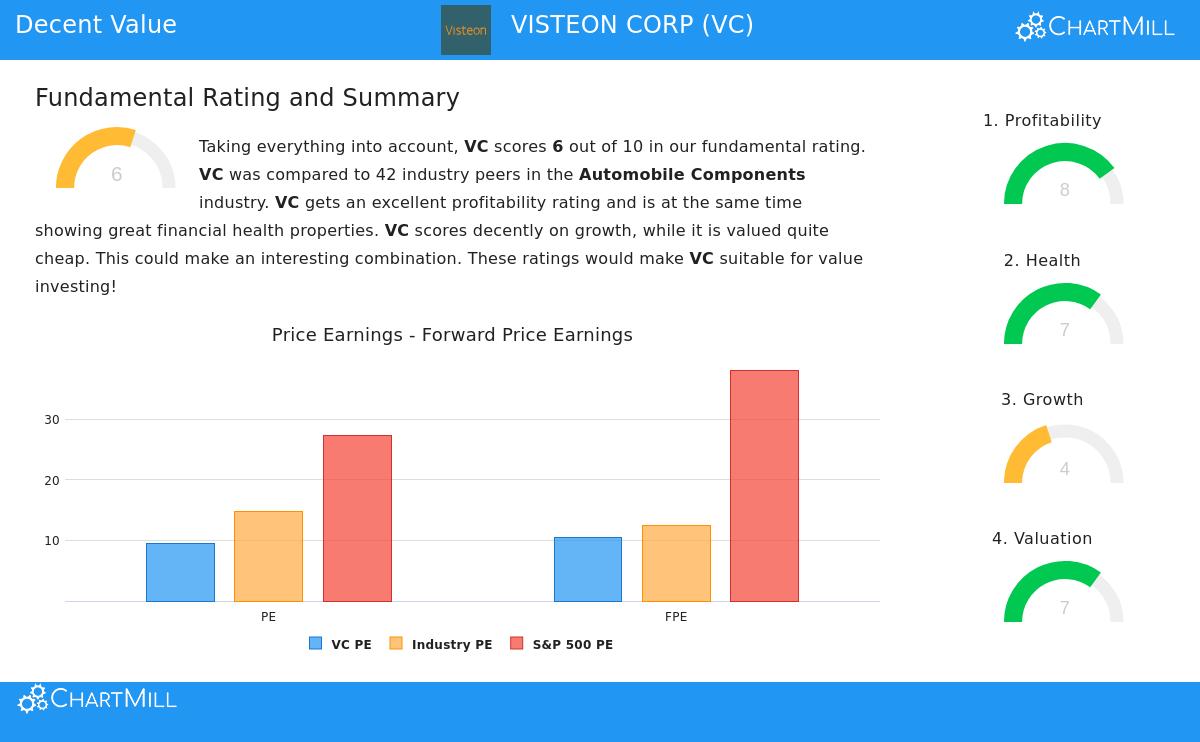

Valuation: An Interesting Starting Price

The heart of any value investment case is a good price. Visteon’s ChartMill Valuation mark of 7 out of 10 indicates the stock is priced well. The details behind this mark support this view:

- Price-to-Earnings (P/E) Ratio: At 9.47, Visteon’s P/E ratio is much lower than the S&P 500 average of 27.33. Within its Automobile Components sector, it is less expensive than about 90% of similar companies.

- Forward P/E Ratio: The future-looking measure of 10.53 also shows a fair price, trading below both the wider market and most of its sector rivals.

- Enterprise Value to EBITDA & Price/Free Cash Flow: These other valuation measures support the idea, with Visteon seeming less expensive than more than 90% of its sector peers based on these numbers.

For a value investor, these numbers are the first step. They show the market is not adding extra value to Visteon’s earnings or cash flows, possibly making a chance if the company’s fundamental positives are lasting.

Financial Health: A Firm Base

A low price means little if the company’s finances are poor. Value investing needs a buffer, and a financially sound company gives exactly that. Visteon gets a firm Health mark of 7, with several main positives:

- Strong Solvency: The company’s Altman-Z score of 3.73 points to a very small short-term chance of financial trouble and is with the best in its sector. Its Debt-to-Equity ratio of 0.18 shows a careful balance sheet with a good mix between debt and equity.

- Very Good Debt Management: Maybe most notable is the Debt to Free Cash Flow (FCF) ratio of 1.09. This means Visteon could pay off all its debt with just a bit more than one year of its present FCF production, a situation that beats 90% of its sector and shows very good financial room.

This firm financial health lowers investment risk and gives the company the steadiness to handle economic changes and put money into future expansion, a key part for a long-term value holding.

Profitability: Quality at a Fair Price

Value investing is not only about buying the lowest-priced stocks, it is about buying sound companies at a discount. Visteon’s high Profitability mark of 8 confirms it is a fundamentally good business. The company shows effective use of its money and assets:

- High Returns: Its Return on Assets (5.94%), Return on Equity (12.82%), and Return on Invested Capital (8.90%) all put it in the top group of its sector, doing better than over 80% of peers.

- Getting Better Margins: Both its Profit Margin (5.33%) and Operating Margin (8.97%) are firm compared to the sector and, notably, have been getting better in recent years.

These numbers are important because they show Visteon is not only making sales, but is turning those sales into earnings effectively. A profitable company with high returns on money can build shareholder value over time, which is the final aim for a value investor.

Growth: A Careful View

While pure value stocks sometimes miss expansion, Visteon’s profile includes a future-looking expansion part. Its Growth mark of 4 is average, but the facts show a detailed picture:

- Firm Historical EPS Growth: On average over recent years, Earnings Per Share (EPS) has grown at a very firm rate of over 61% each year.

- Positive Future Predictions: Experts expect this expansion to continue, though at a more careful speed, with future EPS growth guessed at 12% each year and sales growth around 5.6%.

For a value plan, this expected expansion is important. It suggests the company is not stuck, and its fair price is not because of a business in lasting drop. The expansion helps support the idea that calculated value may rise over the holding time.

Conclusion

Visteon Corp shows an example of what a "Decent Value" screen tries to find: a company with a very firm balance sheet, shown earnings power, and fair expansion hopes, all available at a price that seems modest. The mix of a good Valuation mark together with firm Health and Profitability marks suggests the market may be pricing the company’s lasting business model and financial strength too low. While past results are not a promise, the fundamental numbers fit with a methodical value way that looks for quality businesses trading at a fair price.

Interested in finding more stocks that fit this profile? You can use the "Decent Value" screen yourself to see other possible chances by following this link: Discover More Decent Value Stocks.

Disclaimer: This article is for information only and does not make financial advice, a suggestion, or an offer to buy or sell any security. Investing has risk, including the chance of losing the original money. You should do your own study and talk with a qualified financial advisor before making any investment choices.