For investors aiming to assemble a portfolio of lasting, high-achieving businesses, the quality investing method provides a structured system. This system centers on finding companies with durable competitive strengths, reliable earnings, and sound financial condition, with the plan of owning them for many years. One useful instrument for this hunt is the Caviar Cruise stock screen, which uses measurable filters for sales increase, earnings growth, high returns on capital, and good cash flow production. This screen aids in finding firms that are not only increasing in size, but doing so productively and with longevity.

A recent notable result from this screening method is Visa Inc (Class A Shares) (NYSE:V), the worldwide payments technology leader. Visa runs a large network that enables digital payments in over 200 countries, acting as a key piece of infrastructure for international trade. The company's basic financial picture seems to match the central principles of quality investing well, making it an interesting option for more review.

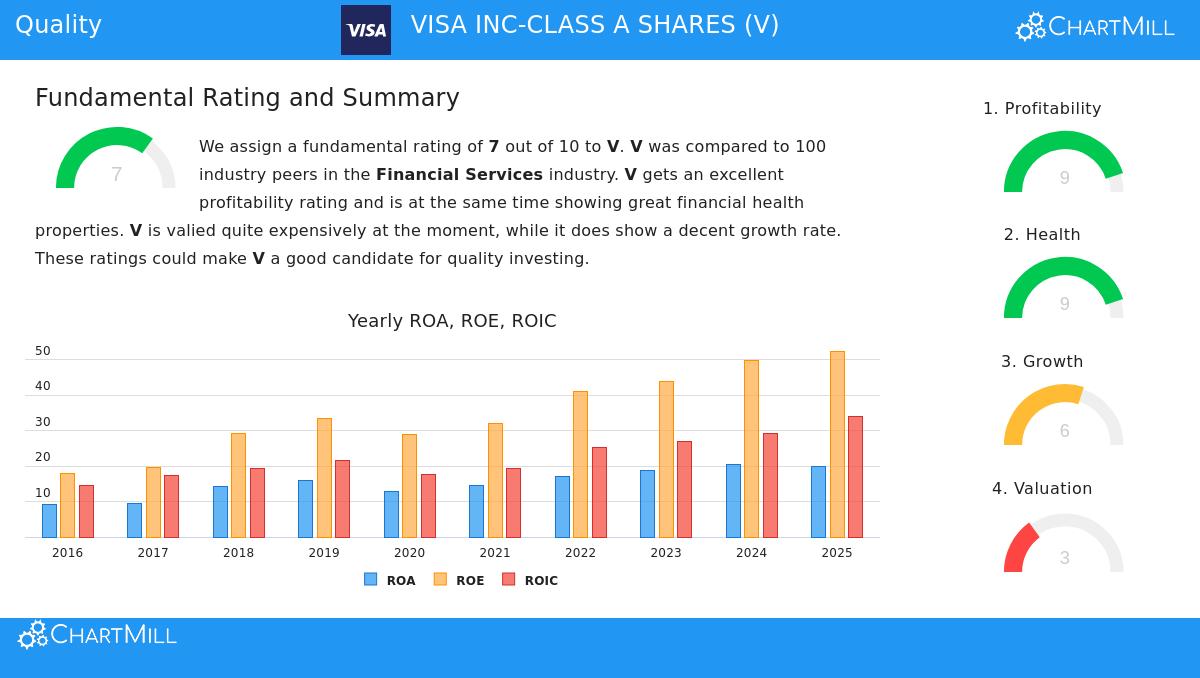

Matching the Central Standards for Quality

The Caviar Cruise screen employs a number of important financial measures to assess a company's caliber. Visa's results against these filters are particularly good.

-

Lasting Increase: The screen demands at least a 5% compound annual growth rate (CAGR) for both sales and EBIT (earnings before interest and taxes) over five years. Visa comfortably passes this, with a 5-year sales CAGR of 10.14% and an EBIT CAGR of 13.51%. Significantly, its EBIT increase is faster than its sales growth, a clear mark of better operational productivity and possible pricing strength, a key trait of a high-caliber business with scale benefits.

-

Outstanding Capital Productivity: Possibly the most important filter for quality investors is a high Return on Invested Capital (ROIC), which calculates how well a company produces earnings from its capital. The screen searches for a ROIC (leaving out cash, goodwill, and intangibles) over 15%. Visa's result is a remarkable 1,665.56%. This very high figure mirrors the asset-light, expandable character of Visa's payment network, where extra transactions need little extra capital, letting earnings move easily to net income.

-

Careful Financial Stewardship: Quality companies handle debt cautiously. The screen uses the Debt-to-Free Cash Flow ratio, favoring companies that could in theory clear all debt in under five years using their present cash flow. Visa's ratio of 0.92 is excellent, showing it could eliminate its complete debt in less than a year, indicating a very strong balance sheet.

-

Superior Earnings: The Profit Quality measure contrasts free cash flow with net income, showing how much reported profit becomes actual, usable cash. A five-year average above 75% is desired. Visa's average of 112.77% shows it reliably creates more free cash flow than its stated net income, a signal of excellent earnings caliber and a business that does not require heavy capital investment.

A Broad Basic Financial Summary

An examination of Visa’s detailed fundamental report supports the screening outcome. The report gives Visa a good total score of 7 out of 10, with special goodness in two zones vital for quality investors:

- Earnings Power (Score: 9/10): Visa ranks near the best in its field for key measures. Its net profit margin is close to 50%, its operating margin is over 66%, and its ROIC and Return on Equity are regularly at the top of the financial services industry. This shows a strong and wide competitive edge.

- Financial Condition (Score: 9/10): The company's ability to pay debts is very good, with a very low chance of financial trouble shown by a strong Altman-Z score. The report affirms the small debt load compared to cash flow, giving notable stability in economic slowdowns.

The main point of care in the report focuses on Valuation (Score: 3/10), where Visa is considered "quite pricey" with a Price-to-Earnings ratio a bit higher than the industry average. This is a typical feature of high-caliber companies; investors frequently must pay more for better and predictable financial results. The report states that this higher price might be partly reasonable due to Visa's exceptional earnings power and anticipated future earnings increase.

The Non-Quantifiable Traits of a Quality Business

Apart from the figures, Visa has several non-numerical characteristics that quality investors value. Its business model gains from the strong, long-term worldwide shift to digital and non-cash payments. It operates a standard "toll road" network, receiving a small charge on a huge and rising number of transactions, which supplies a lasting competitive benefit. The company's services are necessary globally, its model is fairly simple to grasp, and it has shown a capacity to keep pricing strength. Also, as a focused payment processor, it does not face consumer credit risk, making its income more stable during economic changes.

Finding Other Quality Prospects

Visa's close fit with the Caviar Cruise standards makes it a leading sample of the kind of company quality investors look for. For those wanting to find other companies that meet this strict screen, you can see the complete list of results here.

Disclaimer: This article is for information only and is not financial guidance, a suggestion, or an offer to buy or sell any security. Investing carries risk, including the possible loss of the original investment. You should perform your own investigation and talk with a certified financial consultant before making any investment choices.