For investors aiming to assemble a portfolio of lasting, high-performing businesses, the quality investing method provides a structured system. This method centers on finding companies with durable competitive strengths, sound financial condition, and a demonstrated history of producing high returns on capital over many years. Instead of searching for very cheap stocks, quality investors accept paying a reasonable price for superior businesses they can hold for a long time. One organized method to find these companies is through a "Caviar Cruise" stock filter, which selects for particular, measurable signs of quality, such as steady revenue and profit increase, high returns on invested capital, solid free cash flow production, and a low-debt financial structure.

A recent application of this filter has identified ULTA BEAUTY INC (NASDAQ:ULTA) as a company that fits its main standards. The beauty retailer's financial results indicate it has many of the traits quality investors look for.

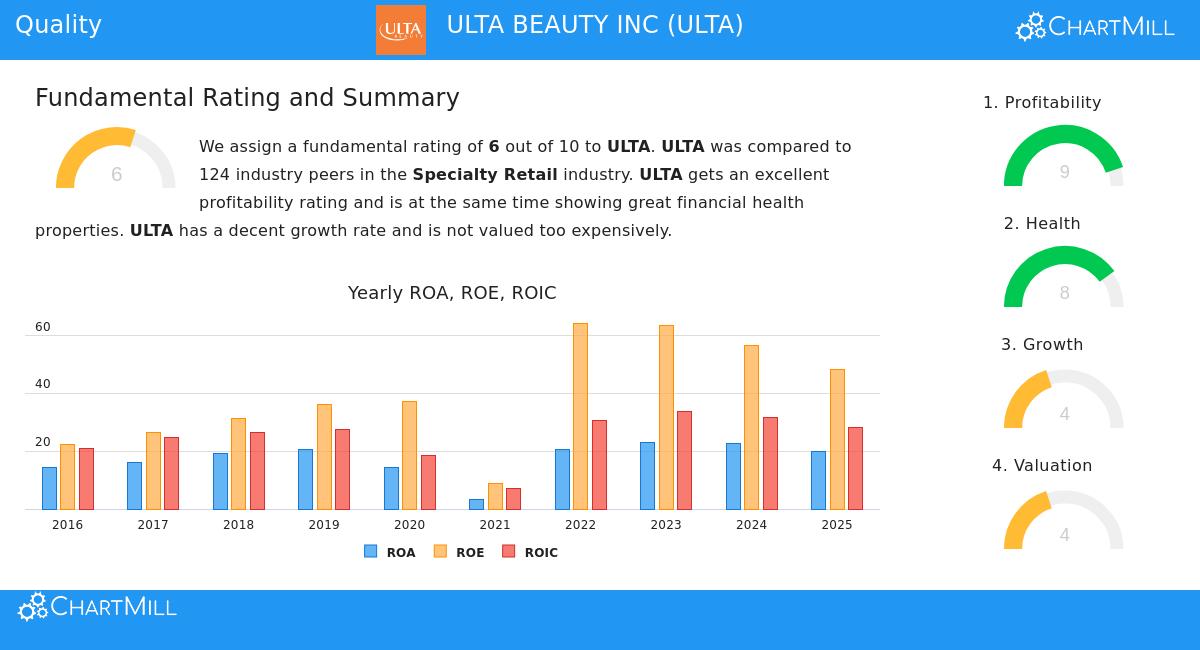

Fitting the Main Quality Standards

The Caviar Cruise filter uses several strict rules to separate companies with a record of high performance and financial soundness. Ulta Beauty's measurements match these rules closely:

- Profitable Increase: The filter requires a minimum 5% compound annual growth rate (CAGR) for both revenue and EBIT (earnings before interest and taxes) over five years. Ulta exceeds this, with a revenue CAGR of 6.28% and a higher EBIT CAGR of 11.68%. Importantly, EBIT increase exceeding revenue increase—as seen here—points to better operational efficiency and possible pricing strength, a main sign of a quality business growing well.

- Superior Capital Use: A core idea of quality investing is a company's skill in producing high returns on the capital it uses. The filter asks for a Return on Invested Capital (excluding cash, goodwill, and intangibles) above 15%. Ulta’s measurement of 27.05% is excellent, suggesting management uses capital very effectively to create profits.

- Financial Strength and Cash Flow Soundness: The method stresses financial safety and the soundness of earnings. The filter selects for a Debt-to-Free Cash Flow ratio below 5, showing how many years of present cash flow would be required to settle all debt. Ulta’s ratio of 0.53 is very strong, showing a balance sheet with almost no debt. Also, the filter looks for a 5-year average Profit Quality (Free Cash Flow/Net Income) above 75%. Ulta’s measurement of 143.84% is notable, showing it turns accounting profits into actual cash at a rate much higher than its net income, giving great financial options for dividends, share repurchases, or new investment.

A Broad Fundamental Perspective

An examination of Ulta’s wider fundamental analysis report supports the image shown by the filter. The company gets a good total rating, with specific strong points in profitability and financial condition.

- Profitability is a Main Strong Point: Ulta’s profitability measurements are consistently very good compared to other specialty retail companies. Its Return on Equity (45.20%) and Return on Assets (16.97%) are in the highest group of the industry. Both its Operating Margin (13.12%) and Profit Margin (9.93%) have shown upward trends and are above industry averages.

- Very Strong Financial Condition: The company’s financial health score is solid. With very little debt, a high Altman-Z score pointing to low bankruptcy risk, and the previously mentioned very good Debt/FCF ratio, Ulta works from a position of notable strength. This gives a buffer in economic slowdowns and allows for strategic movement.

- Valuation and Increase Factors: Valuation measurements show a varied image. While Ulta’s P/E ratio is below the present S&P 500 average, it may be seen as reasonable to somewhat high compared to its own past. Increase is stable, with positive expected future EPS and revenue growth, although analysts forecast a slowdown from the higher past rates. This is common for an established, high-quality company.

For a detailed look at these measurements, you can examine the complete fundamental analysis report for ULTA.

Is Ulta Beauty a "Quality" Business?

Beyond the figures, quality investors evaluate non-financial factors. Ulta’s business plan fits several of these ideas. It works in the stable beauty sector, which has shown qualities of enduring during recessions. Its competitive strength comes from its distinct "all-in-one" store model, merging high-end and popular brands with salon services in one place—a plan hard to copy. The company has national size and a rising online operation, matching the standards of a business with a broad reach. While facing competition and consumer spending changes, its strong brand relationships and loyalty program give some level of pricing strength and customer retention.

Locating Other Quality Possibilities

Ulta Beauty acts as a leading example of the kind of company a quality-centered filter can find. For investors wanting to examine other companies that meet similar strict financial rules, the Caviar Cruise filtering method can be a useful first step. You can see and adjust the filter to view present results here.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer to buy or sell any security. Investing has risk, including the possible loss of the original investment. Readers should do their own research and talk with a qualified financial advisor before making any investment choices.