For investors looking for chances in the market, a disciplined method often requires examining many companies to find those priced below their estimated real worth. One frequent plan is to use a "Decent Value" filter, which tries to find stocks that are fundamentally inexpensive, shown by a good valuation score, while also showing good basic business soundness, earnings, and expansion possibilities. This technique tries to sidestep the typical "value trap," where a low price signals a lasting fall instead of a short-term market error. The aim is to find companies where the market price does not completely show the soundness and future possibility of the business.

Universal Health Services (NYSE:UHS) recently appeared from such a filtering process. As a big operator of acute care and behavioral health facilities in the United States and the U.K., its business is firmly set in necessary healthcare services. The company's latest fundamental analysis report gives a thorough, data-centered view of its financial position, showing a profile that matches closely with the ideas of value investing.

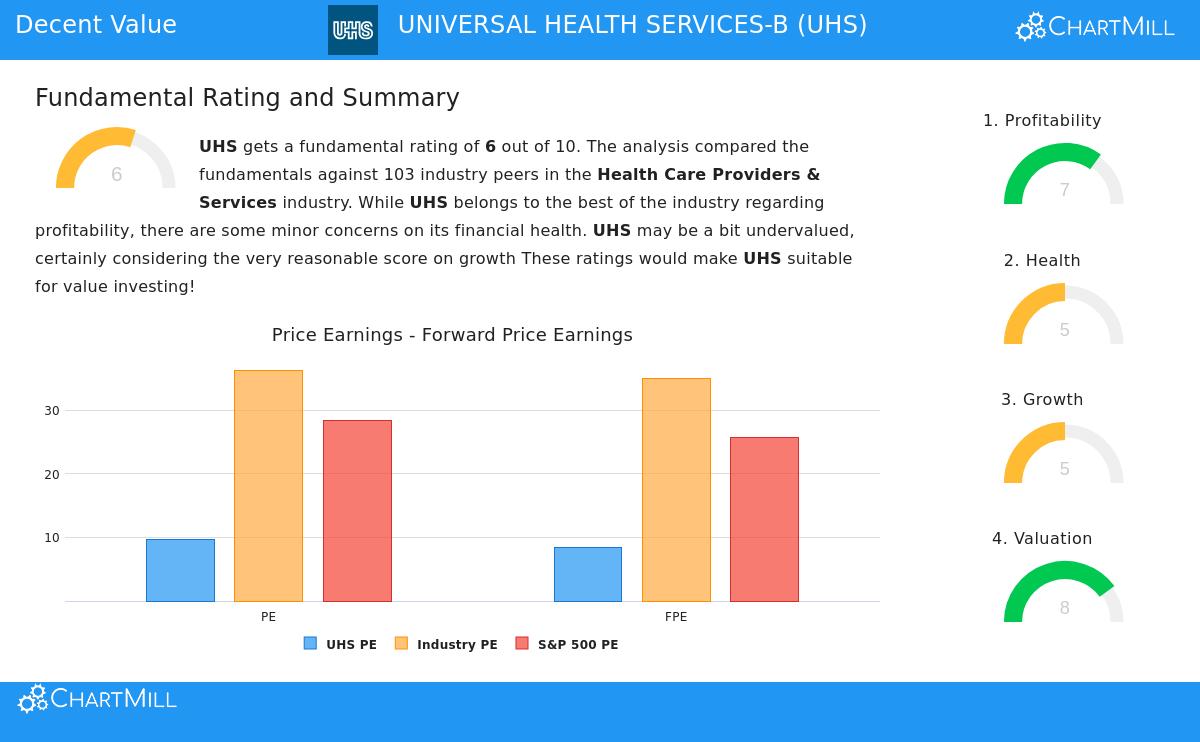

An Interesting Valuation View

The most noticeable part of Universal Health Services' current profile is its valuation, which gets an 8 out of 10 in ChartMill's rating system. This score is the base of the value investment idea, as it implies the stock is priced well compared to the company's earnings and cash flow.

- Price-to-Earnings (P/E) Ratio: At 9.62, UHS's P/E ratio is much lower than both its industry average (36.34) and the wider S&P 500 average (28.39). It is less expensive than 93% of similar companies in the Health Care Providers & Services industry.

- Forward P/E Ratio: The valuation stays interesting looking forward, with a forward P/E of 8.40, which is also below industry and market comparisons.

- Cash Flow and EBITDA: The company also seems priced low based on cash flow and earnings measures. Its Enterprise Value to EBITDA and Price to Free Cash Flow ratios are less expensive than 85% and 78% of industry rivals, in that order.

For a value investor, these numbers are important. They show that investors are paying a fairly low price for each dollar of the company's present and forecasted earnings, making a possible "margin of safety" if the business does as forecasted.

Basic Earnings and Financial Soundness

A low valuation is only interesting if the company is basically sound. This is where the filter rules for decent earnings and soundness matter, making sure the low price isn't a warning sign for worse issues. UHS gets a 7 for earnings and a 5 for financial soundness.

The company's earnings numbers are a specific strong point:

- It has a good Return on Equity of 19.18% and a Return on Invested Capital of 12.33%, both doing better than most of its industry peers.

- Operating and Profit Margins are sound at 11.47% and 8.09%, in that order, putting UHS in the higher group of its sector.

Financial soundness shows a more varied, but workable, view. The company has a middling debt level with a Debt/Equity ratio of 0.55 and a sound Altman-Z score of 3.10, showing no short-term bankruptcy danger. However, cash availability numbers like the Current and Quick Ratios are on the lower side compared to industry averages, suggesting investors should watch the company's short-term working capital handling. In total, the soundness score of 5 suggests a steady, if not exceptionally strong, balance sheet that supports continuing operations.

Expansion Supporting the Idea

A full value investment thinks about not just the present low price and sound base, but also the possibility for future expansion to push the stock price up. UHS's expansion rating of 5 shows a steady, sensible path.

- Recent Results: The company has shown strong recent speed, with Earnings Per Share (EPS) expanding by over 40% in the last year and Revenue going up by 10.21%.

- Future Forecasts: Analysts expect this positive trend to continue, with EPS predicted to expand at an average yearly rate of 13.53% in the coming years. Revenue expansion is expected to be more modest but positive.

This expansion part is important for the value plan. It gives the trigger that could lead the market to re-price the stock, closing the difference between its present low valuation measures and its real worth as an expanding, earning company.

Conclusion

Universal Health Services presents an example in the modern value filter: a company trading at a big markdown to its industry and the wider market, yet supported by good earnings, a steady financial setup, and believable expansion forecasts. Its business model, centered on necessary healthcare services, gives some recession protection. While investors should be aware of its cash availability numbers and the changing nature of some healthcare spending, the total fundamental view suggests the market may be pricing low its steady cash-making ability.

For investors wanting to examine similar chances, the "Decent Value" filter that found UHS can be a helpful beginning point. You can find more stocks that meet these rules of good valuation paired with decent basics via this link.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. Investing involves risk, including the potential loss of principal. Always conduct your own research and consider your financial situation and risk tolerance before making any investment decisions.