The search for undervalued companies is a core part of value investing, a method established by Benjamin Graham and widely used by Warren Buffett. This approach focuses on finding stocks priced below their inherent worth, decided by examining a company's financial condition, earnings, and future possibilities. The aim is to discover good businesses the market has incorrectly priced for now, providing a possible "margin of safety" for investors. One way to find these stocks is by filtering for those with good valuation numbers while also having acceptable scores in other important fundamental categories.

Universal Health Services (NYSE:UHS) recently appeared from this kind of methodical filtering process. The company, a major owner of hospitals and mental health centers in the United States and the United Kingdom, seems to present a strong case when looked at through classic value investing ideas.

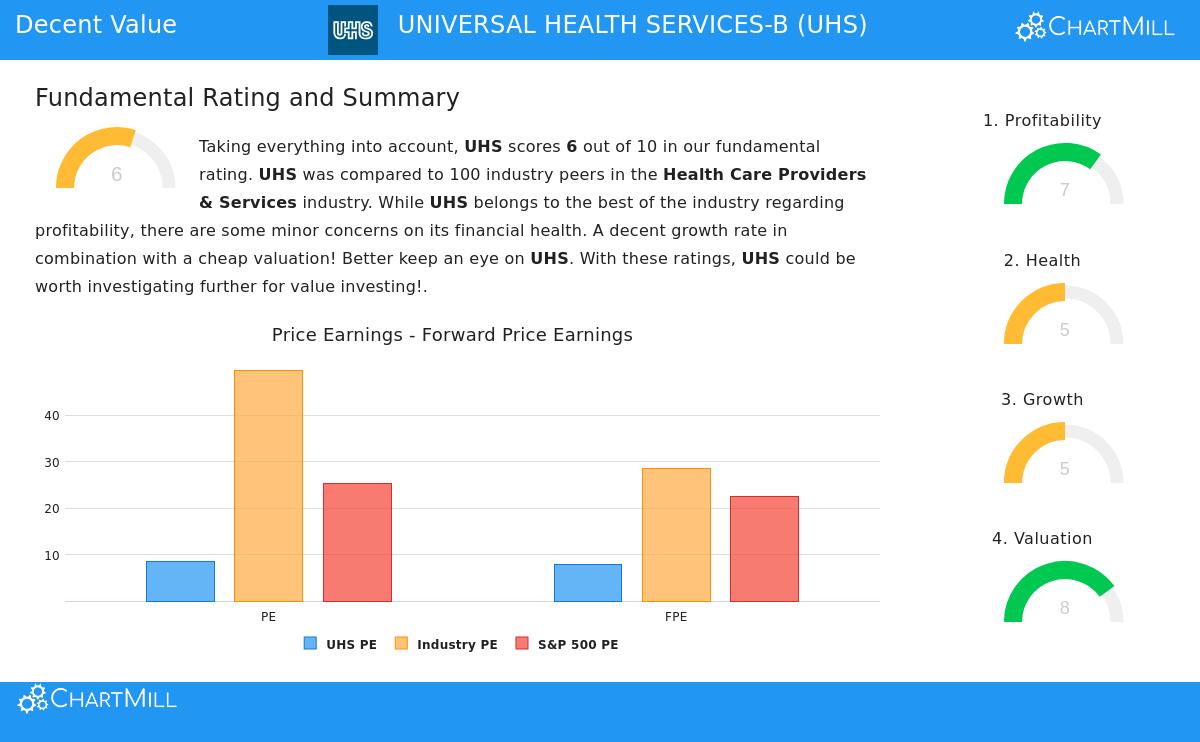

A Strong Valuation Picture

The most noticeable part of Universal Health Services' current fundamental situation is its valuation. In a market where many areas trade at high historical multiples, UHS is distinct as very low-priced. This is exactly the beginning for a value investor: a low cost compared to the company's financial facts.

- Price-to-Earnings (P/E) Ratio: At 8.51, the P/E ratio for UHS is much lower than the S&P 500 average, about 25.2. More significant, it costs less than 96% of similar companies in the Health Care Providers & Services field, where the average P/E is near 49.7.

- Forward P/E Ratio: Looking forward, the valuation stays appealing with a forward P/E of 7.76, which is also under both the wider market and field averages.

- Enterprise Value to EBITDA: This number, which includes debt, gives more proof of the low valuation, showing UHS is valued more cheaply than 89% of its field competitors.

For a value investor, these numbers imply the market might be giving a negative price to the stock, possibly making a chance if the basic business stays good.

Basic Earnings and Financial Condition

A low-cost stock is only a worthwhile find if the company is fundamentally sound. A low valuation with poor finances is frequently a "value trap." UHS's filter results point to force in earnings and sufficient financial condition, which are needed to verify a real undervaluation.

Earnings are a clear positive. The company's Return on Equity (ROE) of 20.46% and Return on Invested Capital (ROIC) of 12.52% are some of the top in its field, doing better than 89% and 87% of similar companies, in order. Its net and operating margins are also solid and have been steady. This reliable skill to create earnings from its assets is a main quality value investors look for, as it supports the idea of a lasting business trading at a lower price.

Financial Condition shows a more varied but acceptable view. The company's ability to pay debts is not a big worry, with a safe Altman-Z score and a sensible Debt-to-Equity ratio that is improved over many field peers. But, liquidity numbers like the Current and Quick ratios are low, pointing to a closer working capital position that needs watching. In total, the condition rating implies the company is not in trouble but works with a balance sheet that needs capable management.

Growth Path and Dividend

While pure value stocks at times do not have growth, UHS displays a good history. Over the last year, Earnings Per Share increased by a notable 30.77%, with a good multi-year average growth rate in both EPS and Revenue. Still, analysts think this growth will slow noticeably in the next few years. This predicted moderation may partly clarify the stock's low valuation. For a value investor, the past proof of growth ability is a good sign, suggesting the business model works, even if near-term increase is thought to be more limited.

The company also gives a small but rising dividend, having raised it for more than ten years. While the yield is very small, the dependable and increasing payment adds to total return and shows management's belief in steady cash flow.

Conclusion: A Possibility for the Value Portfolio

Universal Health Services represents the kind of chance value filters are made to locate: an earning, well-known company in a necessary field, trading at a valuation that seems separate from its operational force. Its high earnings scores and low multiples make a situation where the "margin of safety" Graham stressed may be there. The primary points of care are the weaker liquidity numbers and the predicted slowing in growth, things value investors must balance against the appealing price.

This review of UHS came from a structured examination of its detailed fundamental report. Investors curious about finding other companies that match this "acceptable value" profile, having good valuations with firm fundamentals, can look for more possible choices using the specific stock screener.

Disclaimer: This article is for information only and is not financial advice, a suggestion to buy or sell any security, or a support of any investment plan. Investors should do their own complete research and think about their personal money situation and risk comfort before making any investment choices.