TaskUs Inc. (NASDAQ:TASK) has emerged as a notable candidate for investors following the Peter Lynch-inspired "growth at a reasonable price" (GARP) approach. The strategy, detailed in Lynch's book One Up on Wall Street, focuses on identifying companies with sustainable earnings growth—typically between 15% and 30% annually—combined with low valuations and strong financial health. The core idea is to avoid speculative high-growth names or deeply distressed value traps, instead targeting businesses that can deliver steady expansion without excessive debt or inflated price tags. This method prioritizes long-term buy-and-hold investing, relying on fundamental metrics like the PEG ratio, debt-to-equity, and return on equity to filter out companies that are both growing and reasonably priced.

Recent Performance and Growth Profile

TaskUs has demonstrated strong historical growth that aligns well with the Peter Lynch framework. Over the past five years, the company has achieved an impressive average earnings per share (EPS) growth rate of 25.72%, comfortably within Lynch’s preferred 15% to 30% sweet spot. This suggests the business has been expanding at a sustainable clip, not the kind of explosive, unsustainable growth that Lynch warns against.

In the most recent fiscal year, EPS growth accelerated to 26.36%, while revenue expanded by nearly 19%. These figures indicate the company is still firing on all cylinders. However, analysts expect some deceleration: future EPS growth is projected at around 2.16% annually, with revenue growth of roughly 6.2% per year. While this slowdown is a point of caution, it also reflects the maturing nature of the business, which Lynch himself acknowledges as acceptable if valuations remain attractive.

Valuation Metrics

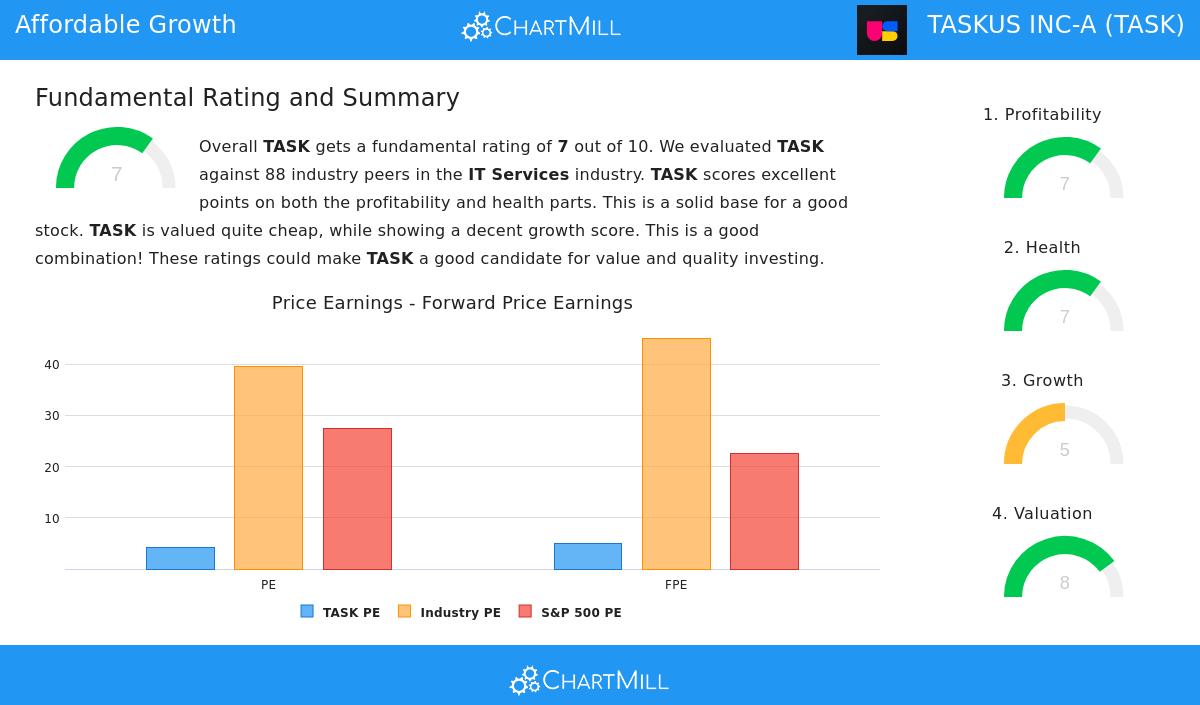

One of the strongest arguments for TaskUs as a GARP candidate is its valuation. The company currently trades at a price-to-earnings (P/E) ratio of just 4.27. This is extraordinarily cheap compared to the broader market—the S&P 500’s average P/E is about 27.5—and even more so relative to its industry peers, where 92% of companies in the IT Services sector trade at higher multiples.

The PEG ratio—which Lynch popularized as a way to measure price relative to growth—stands at just 0.17 when using past five-year growth. A PEG below 1.0 is considered undervalued by Lynch’s standards, and TaskUs’s figure sits far below that threshold, signaling a strong bargain. Even using forward growth estimates, the value proposition remains strong. The price-to-forward earnings ratio is 4.91, again well below both the industry and the S&P 500, reinforcing that the market has not fully priced in the company’s earning potential.

Financial Health and Profitability

TaskUs passes Lynch’s health checks with flying colors. The company’s debt-to-equity ratio is 0.37, well within the 0.6 upper limit Lynch set (and close to his preferred 0.25 threshold). This indicates a conservative capital structure where equity funds most operations, reducing financial risk.

The current ratio stands at 3.12, far above the 1.0 minimum Lynch required. This means TaskUs has more than three times the current assets needed to cover short-term liabilities, providing a strong liquidity cushion. Profitability is also solid: return on equity (ROE) is 17.05%, exceeding the 15% filter used in the Lynch screen. Operating margins are healthy at 11.93%, and gross margins sit at 38.36%, with both metrics trending positively in recent periods.

Our full fundamental analysis—available in the detailed report here—awards TaskUs a strong overall rating of 7 out of 10. The company scores highest in valuation (8/10) and health (7/10), with profitability also earning a 7/10. Growth receives a 5/10, reflecting the expected deceleration but still respectable for a value-focused screen.

Analyst Views and Market Context

While the long-term trend for the broader S&P 500 remains positive, both over the short and long term, TaskUs operates in the IT Services industry, which benefits from ongoing digital transformation trends. The company’s focus on digital customer experience, trust and safety, and AI services positions it well for secular growth, even if near-term forecasts are modest. Insider buying and share buyback programs—both favored by Lynch—are worth monitoring as additional signals of confidence.

The attractive valuation combined with solid profitability and low debt makes TaskUs a textbook example of what the Lynch strategy targets: a growing business that the market has overlooked, priced for a meaningful margin of safety.

Further Screening Opportunities

For investors interested in applying this same disciplined approach to other stocks, the Peter Lynch Strategy screen offers a wider list of candidates meeting the same criteria. These filters help identify companies with solid earnings growth, reasonable valuations, and strong financial health—ideal for long-term GARP investors seeking quality at a discount.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Always conduct your own research before making any investment decisions.