The investment philosophy of legendary fund manager Peter Lynch, as detailed in his book One Up on Wall Street, centers on identifying companies with strong, sustainable growth that are trading at reasonable prices. Often categorized as a "Growth at a Reasonable Price" (GARP) approach, Lynch’s strategy seeks to avoid the extremes of speculative growth stocks and deep-value turnarounds. Instead, it focuses on financially healthy businesses with a proven record of earnings expansion, solid profitability, and a manageable debt load, all while ensuring the stock price does not overpay for that future potential. A key tenet is investing in what you understand, suggesting that often the best opportunities are in companies with straightforward, durable business models.

One company that recently surfaced from a screen built on Lynch's core criteria is TaskUs Inc-A (NASDAQ:TASK), a provider of digital outsourcing services. The firm supports clients in areas like customer experience, content moderation, and artificial intelligence operations. Let's examine how TaskUs fits the principles of long-term, growth-at-a-reasonable-price investing.

Alignment with Peter Lynch Criteria

The Lynch-inspired screen applies several quantitative filters to identify candidates. TaskUs meets these specific benchmarks, which are designed to find companies with sustainable growth, financial health, and attractive valuations.

- Sustainable Earnings Growth: Lynch favored companies growing earnings per share (EPS) between 15% and 30% annually, fast enough to be notable but slow enough to be maintainable. TaskUs demonstrates a solid five-year average EPS growth rate of 25.7%, placing it within this target range.

- Reasonable Valuation via PEG Ratio: Perhaps the most famous Lynch metric is the Price/Earnings to Growth (PEG) ratio. A PEG of 1 or less suggests the stock's price is reasonable relative to its earnings growth. TaskUs has an exceptionally low PEG ratio of 0.15, indicating the market may be pricing its historical growth trajectory very low.

- Strong Profitability (ROE): Return on Equity (ROE) measures how efficiently a company generates profits from shareholder equity. Lynch looked for high ROE as a sign of a durable competitive advantage. TaskUs's ROE of 17.05% is above the screen's 15% threshold, reflecting good profitability.

- Conservative Financial Health: To avoid high risk, Lynch emphasized strong balance sheets. The screen requires a Debt/Equity ratio below 0.6 and a Current Ratio above 1. TaskUs meets both, with a Debt/Equity ratio of 0.37 and a very sound Current Ratio of 3.12, indicating strong liquidity to meet short-term obligations.

Fundamental Health Check

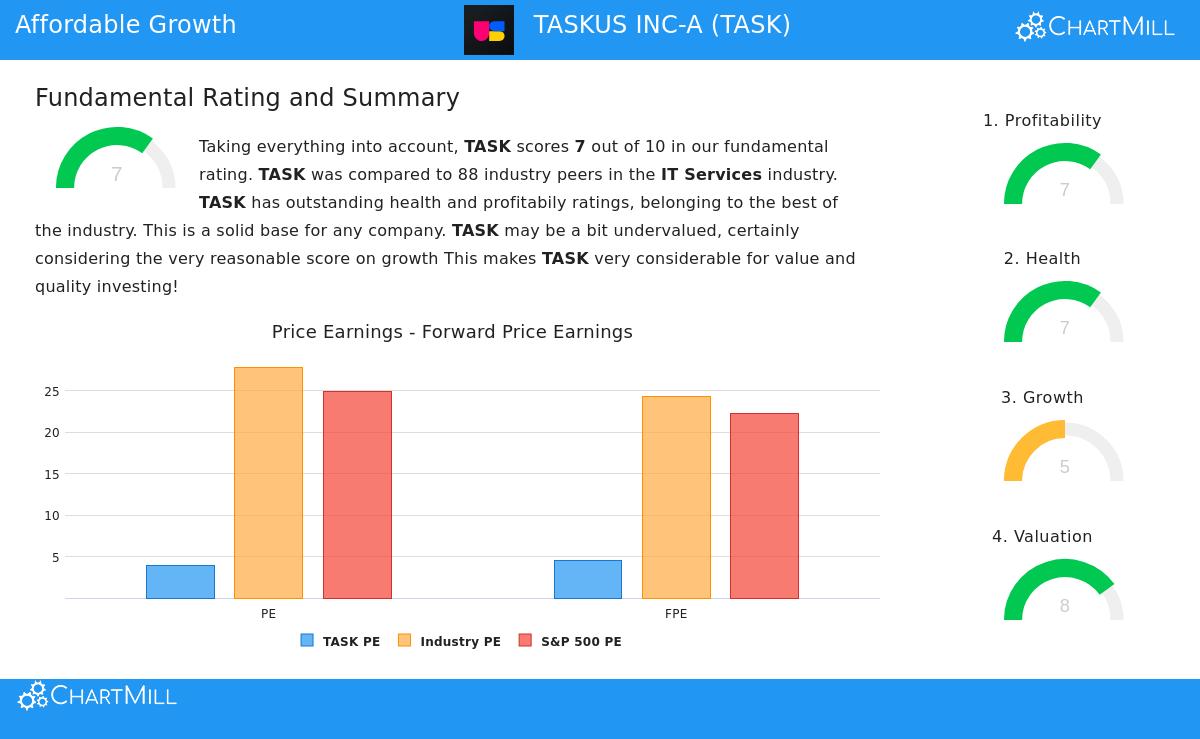

Beyond the screen's filters, a wider look at TaskUs's fundamental profile supports its potential interest to GARP investors. According to a detailed fundamental analysis report, the company earns an overall rating of 7 out of 10, performing adequately across key categories.

- Profitability & Margins: The company receives good scores for profitability, with sound Return on Assets (9.73%) and Return on Invested Capital (10.87%). Its operating margin of 11.93% is better than many of its peers in the IT Services industry and has shown positive change in recent years.

- Valuation Stands Out: The valuation rating of 8 is a specific strength. TaskUs trades at a Price-to-Earnings (P/E) ratio of just 3.96 and a Forward P/E of 4.50, which is lower than over 90% of its industry peers and the broader S&P 500. This low value exists despite the company's sound historical profitability.

- Growth Trajectory: The growth rating is a moderate 5. While past revenue and EPS growth have been notable, analyst expectations for future growth are more measured. This difference between past performance and future expectations is a key area for investors to study more, as it often lies at the center of valuation differences.

A Stock for Further Research

TaskUs presents an interesting case for investors using a Peter Lynch-style strategy. It shows the characteristics Lynch valued: a history of solid, bounded earnings growth, notable profitability metrics, a very strong balance sheet with little debt, and a valuation that seems priced low relative to its performance. The very low PEG ratio suggests the market is not currently valuing the company for its past growth.

However, true to Lynch's philosophy, a screen is only the beginning for "doing your homework." The company's future growth estimates are less strong than its past, which calls for a closer look into its competitive position, client concentration, and the long-term demand for its digital outsourcing services. Investors must determine whether the current valuation is a short-term gap or a sign of basic challenges ahead.

For investors interested in finding other companies that fit this disciplined growth-and-value approach, the full Peter Lynch Strategy screen can provide a list of possible candidates for more study.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any securities. The analysis is based on data and a specific investment strategy framework, investors should do their own complete research and consider their personal financial circumstances before making any investment decisions.