For investors looking for chances where a company's market price seems separate from its basic financial condition, a systematic value method can be a useful rule. This process involves searching for companies that are basically in good shape, showing good profitability, sound finances, and expansion, but are priced at levels that imply the market may not see their possibility. The aim is to find investments where a "margin of safety" is present, offering protection against error and market swings. One stock that recently came up through such a search process, which focuses on good valuation numbers together with acceptable basics, is SSR Mining Inc (NASDAQ:SSRM).

The Denver-based precious metals producer, with operations in the U.S., Canada, Turkey, and Argentina, offers an example in how numerical basic study can point out possible value. A look at SSR Mining’s detailed basic report shows a picture that matches closely with the conditions wanted by value-focused searches.

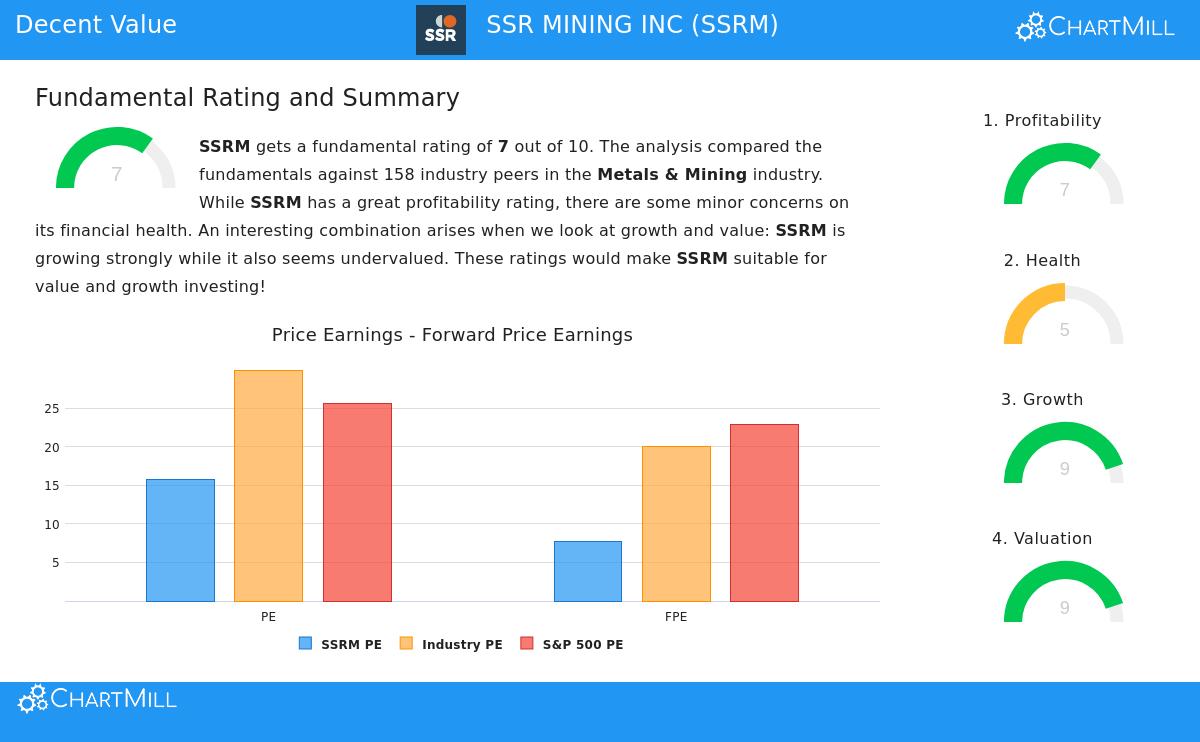

Valuation: The Heart of the Chance

The most persuasive point for SSRM as a value pick rests in its valuation numbers. The company’s ChartMill Valuation Rating is a high 9 out of 10, showing it is priced well compared to both its own basics and similar companies in the Metals & Mining business.

- Price-to-Earnings (P/E): At 15.79, SSRM’s P/E ratio is not only much lower than the current S&P 500 average of 25.60 but is also less expensive than about 87% of its industry rivals.

- Forward P/E: An even more notable number is the forward P/E of 7.75, which is much lower than the industry and S&P 500 averages, suggesting the market is setting very low hopes for future earnings.

- Price-to-Free-Cash-Flow & EV/EBITDA: The stock also seems inexpensive on cash flow and enterprise value measures, doing better than a large majority of its industry peers.

For a value investor, these numbers are the first step. A low valuation alone can be a "value trap," but when paired with sound basics, it can mark a real chance where the market has not yet acknowledged the company’s true value.

Profitability and Growth: The Basic Driver

An inexpensive stock is only a sound investment if the core business is stable and enlarging. SSRM’s basics indicate it is not a still company. It receives a solid Profitability Rating of 7 and an outstanding Growth Rating of 9.

- Sound Margins: The company has notable profit margins, with a Gross Margin of 50.60% and an Operating Margin of 33.01%, putting it in the top group of its industry. Its Return on Equity of 11.28% also does better than most peers.

- Strong Past Growth: Over the last year, SSRM has shown very high growth, with Revenue up 63.68% and Earnings Per Share rising by over 614%. While this speed is unusual, the multi-year average growth rates for both revenue and EPS stay positive and good.

- Increasing Future Projections: Analysts predict this movement to continue, with expected yearly EPS growth of over 15% and Revenue growth above 22% in the next years. The report states that this expected growth rate is actually a rise from recent times.

This pairing is vital for the value plan. It shifts the idea past a simple "inexpensive stock" story to one of an "enlarging company found at an inexpensive price." The growth supplies a reason for the market to finally adjust the valuation upward.

Financial Health: Reviewing the Balance Sheet

The financial condition of a company is a main protection for value investors, making sure the business can handle drops and keep running. SSRM’s Health Rating is an average 5, showing a combination of positives and points that need review.

- Solvency Positives: The company shows sound solvency numbers. Its Debt-to-Equity ratio is a very low 0.04, showing little use of debt funding. Also, its Debt-to-Free-Cash-Flow ratio of 1.55 is very good, meaning it could in theory pay off all its debt with less than two years of cash flow.

- Points for Care: The report notes that the company’s Return on Invested Capital (ROIC) is now under its cost of capital, which is not a perfect sign of value generation. Its Altman-Z score, a bankruptcy risk measure, is also in a "middle area," though the sound cash flow position lessens quick liquidity risk.

For the value search used, an "acceptable" health score is allowable. The search puts a good valuation first, but needs that profitability, growth, and health are not bad. SSRM’s very low debt and sound cash flow creation meet the need for a stable enough base to support more study, even with the mentioned warnings.

Conclusion: A Pick for Value Review

SSRM comes from this basic study as a persuasive pick for investors using a systematic value plan. It presents the classic value situation: a company with sound profitability, notable recent and expected growth, and a fairly stable balance sheet, all found at a valuation that is lower than both the wider market and its own industry. The separation between its operational results and its stock price measure is what value searches are made to find.

It is key to recall that no search is perfect. The mining field is cyclical and affected by material price changes, and the particular points about ROIC and the Altman-Z score call for more detailed review. However, based on the numerical conditions of valuation, growth, profitability, and health, SSR Mining Inc fits with the picture of an underrated stock deserving of closer look by value-centered investors.

This study of SSR Mining was found using a search plan that looks for acceptable value. Investors can review more stocks that match this picture through the Acceptable Value Stocks search.

Disclaimer: This article is for information only and does not form financial guidance, a suggestion, or an offer to buy or sell any securities. The study is based on data and ratings given by ChartMill, and investors should do their own complete research and think about their personal financial situation before making any investment choices. Past results are not a guide for future results.