For investors looking to build a portfolio that creates steady passive income, a strict screening process is necessary. One useful method is to concentrate on stocks that provide a good dividend and are also supported by solid core business operations. A filter that selects for a high ChartMill Dividend Rating, while also asking for good scores for profit and financial condition, tries to achieve this. This method helps find companies where the dividend is probable to be maintained and could increase, instead of being a high-yield pitfall caused by a troubled business. One company that appears from this kind of strict search is ResMed Inc (NYSE:RMD), a top worldwide company in digital health for sleep apnea and respiratory care.

Examining the Dividend Details

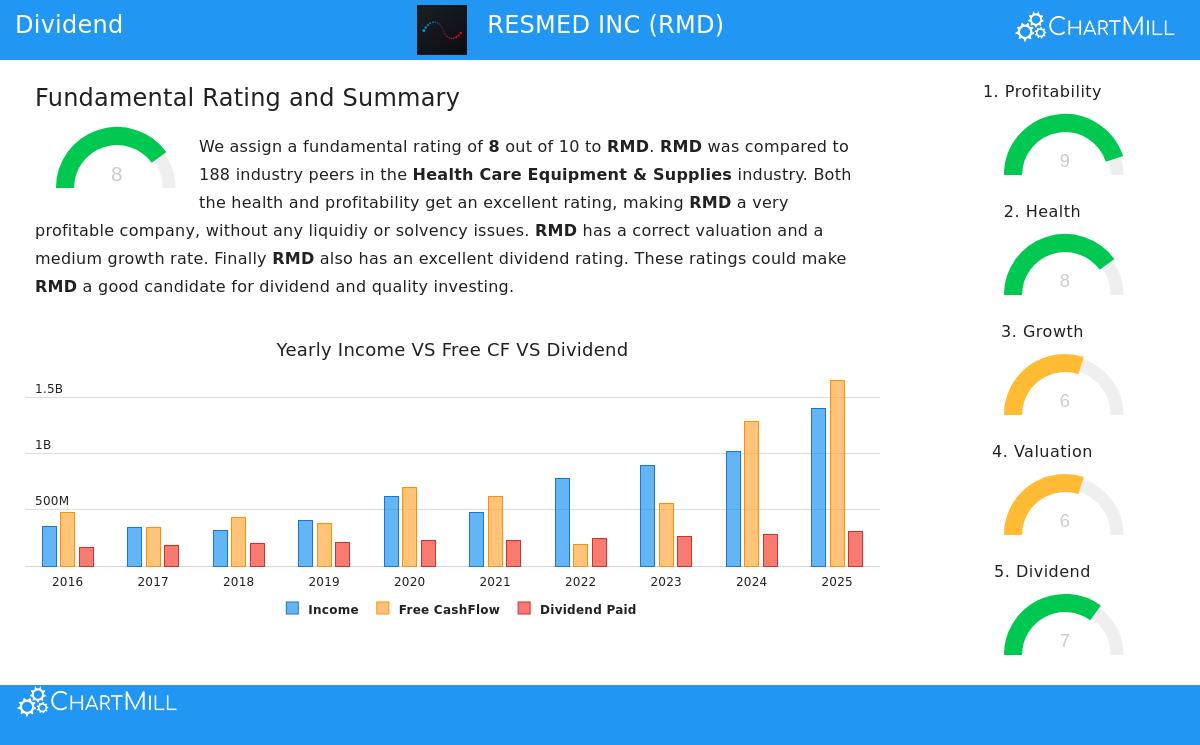

For dividend investors, the durability and growth path of a payment are frequently more critical than the basic yield. ResMed’s dividend details receive a 7 out of 10 on the ChartMill Dividend Rating, showing a good overall evaluation. The company gives a fair yield of 1.05%, which, while not striking by itself, is reinforced by several good elements that indicate steadiness.

- Steady Record and Increase: ResMed has built a consistent history, having paid and raised its dividend for at least ten straight years. The dividend has increased at a good yearly rate of 6.33% over the last five years, showing a dedication to giving more capital back to shareholders.

- Maintainable Payment: Importantly, the dividend seems well-covered by the company’s profits. ResMed uses only 22.25% of its income for dividends, a careful amount that leaves plenty of space to put money back into the business and handle economic declines without threatening the payment. This low payout percentage is a key part of dividend durability, directly meeting the screening plan's aim of steering clear of companies where the dividend is in danger.

- Profits Support Increase: Also, the company’s profit increase is faster than its dividend increase. This situation means the dividend is turning into an even lesser part of total earnings over time, making its base and ability for future raises stronger. For a dividend growth plan, this match between profit increase and dividend increase is perfect.

The Base: Profit and Financial Condition

A lasting dividend cannot be present without a profitable and financially stable company. This is why the screening process gives the same importance to the ChartMill Profit and Condition Ratings. ResMed does very well here, with ratings of 9 and 8, in that order, giving a firm base for its shareholder returns.

The company’s profit is outstanding. Important measures like Return on Assets (17.47%), Return on Equity (23.51%), and Return on Invested Capital (20.84%) all place in the best group of its Health Care Equipment industry. Its operating margin of 34.11% is very high, doing better than over 99% of industry competitors. This operational quality creates the large and steady cash flows required to pay for dividends, research, and growth projects at the same time.

Financially, ResMed is in a strong position. It has a good Altman-Z score of 12.03, showing very little bankruptcy risk, and holds a very small amount of debt compared to its cash flow. Its debt-to-free-cash-flow ratio of 0.37 is very good, meaning it could in theory pay off all its debt in under five months using current cash flow. This financial strength makes sure the company can keep its dividend during economic ups and downs, a main thought for long-term income investors.

Value and Growth Setting

While the main attention is on income, knowing value and growth possibilities gives a full view. ResMed’s value gets a neutral-to-good evaluation with a score of 6. Its Price-to-Earnings ratio of 22.4 is similar to the wider S&P 500 and is actually less expensive than many in its own industry. More significantly, its Price-to-Free-Cash-Flow ratio is less expensive than 90% of its competitors, hinting the market might be pricing its strong cash creation fairly.

The company also displays a satisfactory growth path, with a score of 6. Over the last year, it has given solid revenue growth of 9.57% and notable EPS growth of 16.29%. While analyst forecasts point to a slowing in growth rates in the future, they still predict a satisfactory high-single-digit rise in revenue and a double-digit jump in EPS. This continuing growth backs the chance for ongoing dividend raises, connecting back to the central aim of a dividend growth plan.

Final Thoughts

ResMed Inc offers a strong argument for dividend-focused investors who value quality and durability above maximum yield. It comes from a screen made to find companies with steady payments supported by solid core operations. The stock joins a rising dividend with a ten-year history, a very maintainable payout ratio, outstanding profit, and a very firm balance sheet. While the present yield may be moderate, the mix of dividend growth, financial condition, and business strength fits well with a long-term, income-focused investment method.

For investors wanting to look at other companies that fit similar standards of high dividend quality, good profit, and stable financial condition, you can see the full screen findings here.

Disclaimer: This article is for information only and does not make up financial guidance, a suggestion, or a plan to buy or sell any security. Investors should do their own study and talk with a skilled financial advisor before making any investment choices. The study is based on given data and shows conditions at a particular time, which can change.