The investment philosophy of legendary fund manager Peter Lynch, as detailed in his book One Up on Wall Street, centers on finding companies with strong, sustainable growth that are trading at reasonable prices. Often categorized as a "Growth at a Reasonable Price" (GARP) approach, Lynch’s strategy avoids speculative high-flyers in favor of profitable, financially sound businesses that an investor can understand and hold for the long term. His methodology uses specific quantitative screens to find candidates, focusing on earnings growth, valuation, profitability, and balance sheet health. A recent screen based on these principles has identified DR. REDDY'S LABORATORIES-ADR (NYSE:RDY) as a stock for more study.

Alignment with Lynch's Core Criteria

The Peter Lynch screen applies several strict filters to find companies with the right profile for long-term investment. DR. Reddy's Laboratories appears to meet these key benchmarks, which are made to identify sustainable growth without too much risk.

- Sustainable Earnings Growth: Lynch looked for companies with a proven history of growth, but was cautious of unsustainably high rates. The screen requires a 5-year earnings per share (EPS) growth rate between 15% and 30%. DR. Reddy's reports a 5-year EPS growth rate of 23.6%, comfortably within this target range. This shows a history of strong, yet potentially manageable, expansion.

- Reasonable Valuation (PEG Ratio): Perhaps the central part of Lynch's valuation approach is the Price/Earnings to Growth (PEG) ratio. A PEG of 1 or less suggests the stock's price is reasonable relative to its earnings growth. DR. Reddy's has a PEG ratio of 0.78, indicating that the market may be undervaluing its growth path when viewed this way.

- Strong Profitability (Return on Equity): Lynch preferred companies that efficiently generate profits from shareholder equity. A minimum Return on Equity (ROE) of 15% is a key filter. DR. Reddy's has an ROE of 16.0%, demonstrating its ability to deliver solid returns on the capital invested in the business.

- Financial Health (Debt & Liquidity): A conservative balance sheet is important for handling economic downturns. The screen requires a Debt/Equity ratio below 0.6 and a Current Ratio above 1. DR. Reddy's does well here, with a very low Debt/Equity ratio of 0.03 and a Current Ratio of 1.85. This shows minimal use of debt and good short-term liquidity, fitting with Lynch's preference for financially strong companies.

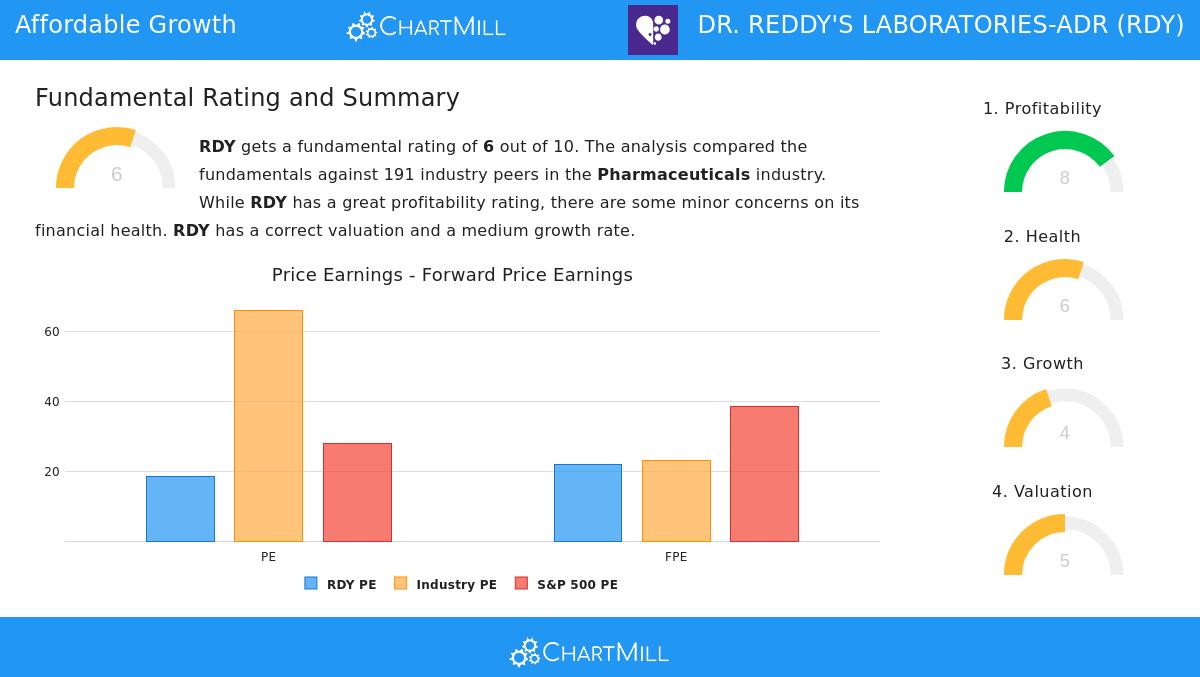

Fundamental Profile Overview

A wider look at DR. Reddy's fundamental rating, which scores a 6 out of 10, gives a more detailed picture that mainly supports the Lynch screen's findings. The company's clear strength is its profitability, where it scores an 8 out of 10. It ranks well within the pharmaceuticals industry for measures like Return on Assets, Return on Invested Capital, and its healthy profit margins.

The company's financial health receives a neutral score of 6, supported by a very strong solvency position (excellent Altman-Z score and low debt) but somewhat weaker liquidity ratios compared to industry peers. Its valuation score of 5 is mixed; while its P/E ratio appears expensive alone, it is actually lower than most of its industry and the broader S&P 500, especially when considering measures like Enterprise Value to EBITDA.

The main area of caution is growth, which scores a 4. While the company has a strong history of revenue and EPS growth over the past five years, analyst estimates point to a possible slowdown in the years ahead. This highlights the need for an investor's own research to judge the sustainability of its growth drivers. You can review the full, detailed fundamental analysis report for DR. Reddy's Laboratories here.

Conclusion for the Long-Term Investor

For an investor following Peter Lynch's principles, DR. Reddy's Laboratories presents an interesting case. It passes the quantitative screen by showing a history of strong earnings growth, trading at a reasonable PEG valuation, maintaining high profitability, and operating with a very solid balance sheet. These are exactly the traits Lynch linked with successful long-term holdings. The company works in the essential and understandable pharmaceutical sector, further fitting with his "invest in what you know" idea.

However, the Lynch strategy is a beginning for research, not a final buy signal. The fundamental report points out the need to look into the expected growth slowdown. A long-term investor must judge whether the company's pipeline, market expansion, and operational efficiency can overcome these lower expectations and continue its historical path.

If DR. Reddy's profile interests you, it was found using a specific stock screening method. You can find other companies that currently pass the Peter Lynch investment screen by viewing the full results here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. The Peter Lynch strategy is a historical framework, and past performance is not indicative of future results. Investors should do their own complete research and consider their individual financial situation and risk tolerance before making any investment decisions.