For investors looking to find undervalued opportunities, a disciplined screening process can be a useful starting point. One such method is to look for companies that are fundamentally good but priced below their intrinsic value. This usually means filtering for stocks with high ratings in financial condition and earnings, paired with an attractive valuation score, while also showing some ability to grow. This process tries to find possible bargains, companies whose market price might not yet show their actual business quality, providing a margin of safety that is key to value investing ideas.

Radian Group Inc. (NYSE:RDN), a provider of private mortgage insurance and risk management services, appears from such a screen as a stock needing more examination. The company’s fundamental picture, as shown in its ChartMill Fundamental Analysis Report, shows a business with good condition trading at what looks like a large discount.

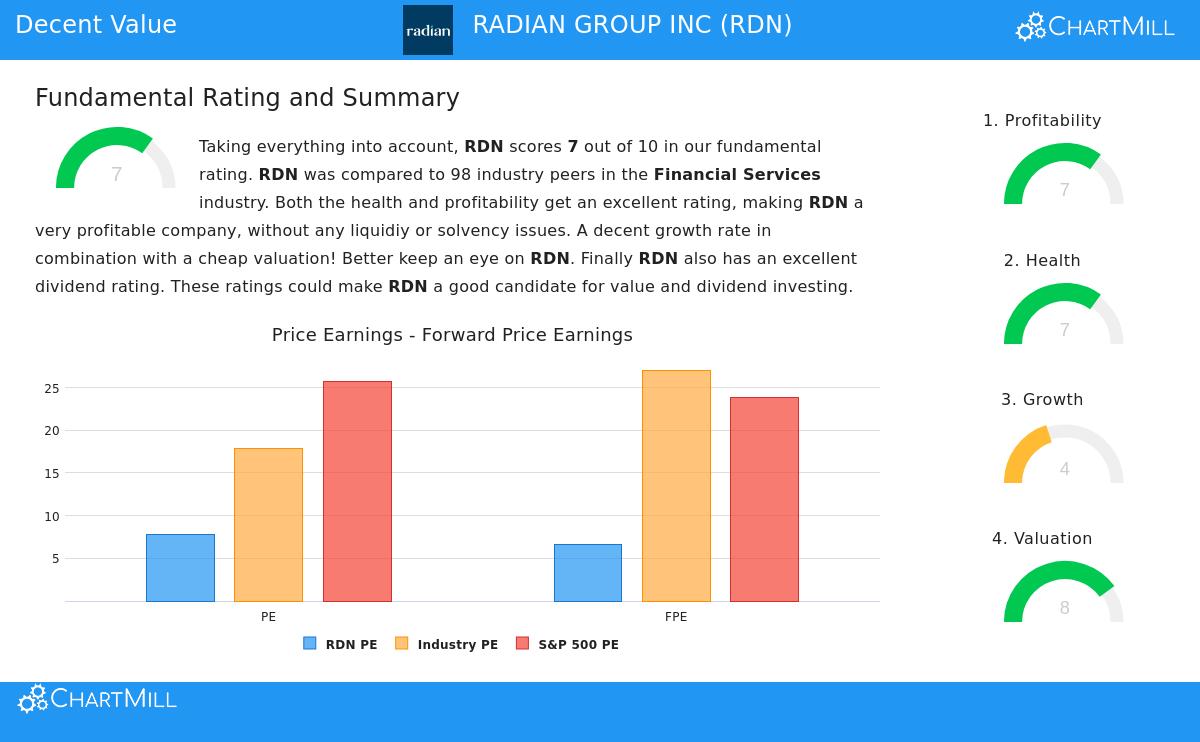

An Attractive Valuation Picture

The main point of the value case for Radian is its very appealing valuation measures. In a setting where many stocks trade at high prices, RDN is notable for being inexpensive compared to both its profits and the wider market.

- Price-to-Earnings (P/E) Ratio: At 7.74, RDN’s P/E ratio is called "very cheap" in the report. This is much lower than the S&P 500 average of 25.71 and less expensive than over 72% of similar companies in the Financial Services industry.

- Forward P/E Ratio: The valuation seems even more attractive looking ahead, with a Price/Forward Earnings ratio of 6.60. This shows the market is using a low multiple for the company’s expected future earnings.

- Enterprise Value to EBITDA: Adding to the inexpensive valuation, 85.7% of companies in its industry are priced higher than RDN based on this measure of a company’s total value.

For a value investor, these measures are important. A low P/E ratio can indicate a stock is priced low, if the company’s fundamentals are strong. It allows for possible price increase as the market adjusts its view, moving the stock price nearer to the company’s earnings ability.

Basic Strength: Earnings and Financial Condition

An undervalued stock is only a real opportunity if the company is financially stable. A low price on a poor or declining business is often a "value trap." Radian’s report, however, points to high scores in both earnings and financial condition, giving a firm base for its low valuation.

Earnings is a main area of quality. The company has notable margins that do better than most of its industry.

- Its Operating Margin of 69.05% is higher than nearly 94% of industry peers.

- In the same way, its Profit Margin of 46.91% is better than almost 89% of competitors.

- Returns on important investments, Assets, Equity, and Invested Capital, all rate in the top groups of its industry, showing very efficient use of capital.

Financial Condition is similarly strong, especially related to liquidity. A company’s ability to meet near-term needs is critical, and Radian does very well here.

- Its Current Ratio and Quick Ratio are both a very high 5.43, showing more than enough resources to cover near-term debts. This ratio is better than over 91% of its peers.

- The company keeps a careful Debt-to-Equity ratio of 0.23, showing little use of debt financing.

These high ratings in condition and earnings are key filters for the value approach. They help make sure the "inexpensive" stock is not inexpensive for a bad reason, but instead represents a financially steady business that is producing significant profits.

Growth and Dividend Points

While the main attention is on value, the screen also asked for acceptable growth potential. Radian’s growth picture is varied but displays good signals. Past Earnings Per Share (EPS) growth has been high at nearly 20% each year, though recent revenue patterns have been weak. Looking forward, analysts predict a return to growth, with EPS forecast to rise by over 10% per year. This expected growth, together with its inexpensive valuation, leads to a low PEG ratio, which is often viewed as a signal of an undervalued stock with growth.

Also, RDN provides an appealing dividend yield of 3.08%, which is above both its industry and the S&P 500 averages. The company has a steady 10-year history of paying and raising its dividend, backed by a manageable payout ratio. This income part can give a return buffer while investors wait for a possible valuation adjustment.

Conclusion

Radian Group Inc. shows an example of what value-focused screens try to locate: a company with a very strong balance sheet, high earnings, and a dividend good for shareholders, all available at a price that seems to not fully account for these traits. Its high valuation rating implies the market may be missing its fundamental qualities. While all investments have risk, and the mortgage insurance field is affected by economic changes, RDN’s mix of low valuation, high condition, and strong earnings fits with the main ideas of searching for undervalued opportunities with a margin of safety.

This review of RDN came from a methodical search for acceptable value stocks. Investors wanting to look at other companies that fit similar standards of good valuation, firm condition, earnings, and growth can see the complete screen results here.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer to buy or sell any security. The review uses data and ratings from ChartMill. Investors should do their own research and think about their personal money situation and risk comfort before making any investment choices.