In the search for investment chances, many investors use a disciplined, fundamental method that aims to find companies trading below their intrinsic worth. This approach, often called value investing, involves looking for stocks that seem priced low by the market while still showing strong basic business condition. A usual plan is to find companies with good valuation measures, such as low price-to-earnings ratios, along with firm profitability, a sound financial state, and acceptable growth outlook. This mix can indicate a possible chance where the market price does not completely show the company's lasting earning ability or financial soundness.

One stock that recently came from such a search is Qualys Inc (NASDAQ:QLYS), a supplier of cloud-based security and compliance tools. The company's combined platform aids organizations in managing and protecting their IT assets. According to a fundamental analysis report made by ChartMill, Qualys shows a profile that may interest investors using a value-focused plan. The complete report, which assesses the stock in five main areas, is ready for study here.

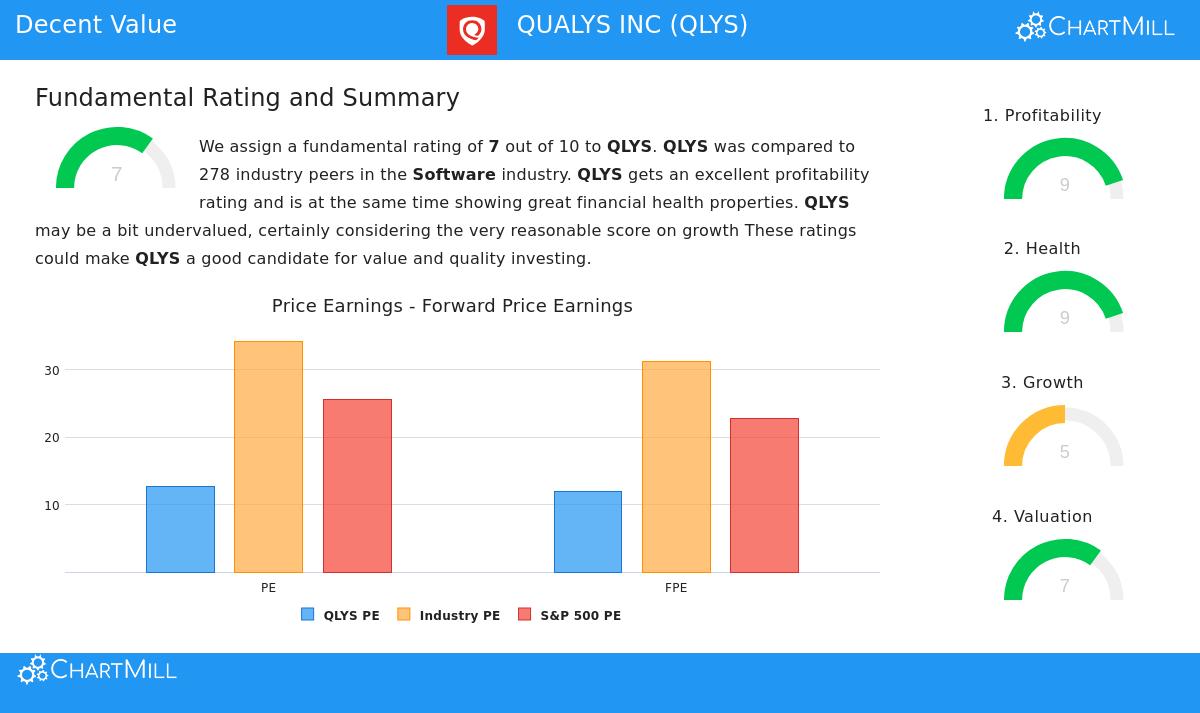

Valuation: The Basis of Chance

For a value investor, valuation is the main screen. A good price compared to earnings, cash flow, or assets is what makes the initial safety buffer, a protection against mistakes in study or unexpected business declines. Qualys's valuation measures are notable as especially interesting, giving it a ChartMill Valuation Rating of 7 out of 10.

- Price-to-Earnings (P/E) Ratio: At 12.70, Qualys's P/E ratio is much lower than the S&P 500 average of about 25.6. More significantly, it costs less than about 84% of similar companies in the competitive software field, where average P/E ratios are often much higher.

- Forward P/E and Cash Flow: The valuation story stays the same when looking forward. With a forward P/E of 11.95, the stock is valued cheaper than over 80% of its field. Also, its Price-to-Free Cash Flow ratio is more appealing than almost 88% of software companies, showing the market is paying a relatively low price for the cash the business produces.

While one measure, the PEG ratio, indicates the stock is costly when growth is considered, this is balanced against the company's outstanding profitability, which can support a higher earnings multiple. Overall, the valuation view suggests Qualys is not priced for ideal conditions, possibly giving a purchase point below its intrinsic worth.

Financial Health: A Base of Soundness

A low-cost stock is only a good investment if the company is financially stable. A firm balance sheet makes sure a business can endure economic troubles, put money into growth, and avoid weakening financing, key points for long-term investors. Qualys does very well here, having a top-level ChartMill Financial Health Rating of 9.

- Debt-Free Balance Sheet: Maybe the most notable part is that Qualys has no debt. This provides it great operational freedom and takes away the risk and cost linked to interest payments and refinancing.

- Solvency and Value Creation: The company's Altman-Z score of 4.88 shows a very low short-term risk of financial trouble, doing better than over three-quarters of its field. Importantly, its Return on Invested Capital (ROIC) easily goes beyond its cost of capital, meaning it is making real economic value for shareholders.

- Shareholder-Friendly Actions: The company has been lowering its share count over the past one and five years, a habit that can raise the ownership stake and earnings per share for remaining investors.

Profitability: High-Standard Earnings Ability

Value is not only about a low price; it is about getting a stake in a high-standard business at that price. Superior and lasting profitability is a sign of such businesses, as it shows pricing ability, operational effectiveness, and a lasting competitive edge. Qualys's profitability is outstanding, getting a near-perfect rating of 9.

- Field-Leading Margins: The company works with top-level efficiency. Its Profit Margin of 29.64% and Operating Margin of 33.17% do better than over 91% and 96% of software field peers, in that order. Its Gross Margin of almost 83% is also very good, indicating a highly scalable software-as-a-service (SaaS) business model.

- Firm Returns on Capital: Qualys turns its investments into profits at a notable rate. Its Return on Assets (18.11%), Return on Equity (35.34%), and ROIC (28.84%) all place in the top tenth of its field, displaying management's effective use of capital.

Growth: A Considered Way Forward

While pure value stocks sometimes lack growth, the best candidate provides an acceptable growth path to help narrow the difference between price and worth over time. Qualys's growth profile is acceptable, with a ChartMill Growth Rating of 5. Its past performance has been firm, with EPS growing almost 20% each year on average and revenue growing over 13% each year in recent years.

The view, however, is for a more measured speed. Analysts estimate average yearly EPS growth of around 5.7% and revenue growth of about 6.9% for the coming years. This estimated slowdown is probably a main reason in the stock's modest valuation. For a value investor, this makes a situation where the company's shown skill to produce large profits and cash flow is not matched with strong growth hopes, possibly leading to a wrong price.

Conclusion

Qualys presents a case that fits several ideas of value investing. It seems to be valued at a lower price relative to both the wider market and its own field, giving a possible safety buffer. This lower price exists together with a very strong balance sheet with no debt and profitability measures that are with the best in the software area. While its growth is expected to become normal, the company's proven model of producing high-margin, repeating revenue gives a stable base. For investors searching for fundamentally sound companies trading at sensible prices, Qualys deserves more study.

This analysis was based on a "Decent Value" search that filters for stocks with good valuation ratings and firm fundamentals. Investors curious about finding other companies that meet similar conditions can find more outcomes through this pre-set stock screen.

Disclaimer: This article is for information only and does not make up financial advice, a suggestion to buy or sell any security, or a support of any investment plan. Investing includes risk, including the possible loss of original money. Readers should do their own study and talk with a qualified financial advisor before making any investment choices.