For investors aiming to construct a portfolio on the ideas of value investing, the central task is finding companies selling for less than their inherent value. This established method, created by Benjamin Graham and used by Warren Buffett, requires a systematic hunt for stocks where the market price is below a measured guess of the company's real value. The aim is to buy these discounted assets and keep them as the market in time sees and fixes the difference. A useful first step for this hunt is to filter for companies that show sound basic condition and earnings but are valued at a lower price compared to similar companies and the wider market, hinting at a possible buffer.

QUALYS INC (NASDAQ:QLYS), a supplier of cloud security and compliance tools, comes up as a possibility from this kind of filtering. The company's recent fundamental analysis report shows a picture that fits several important value-investing measures, joining sound finances with what seems a fair price.

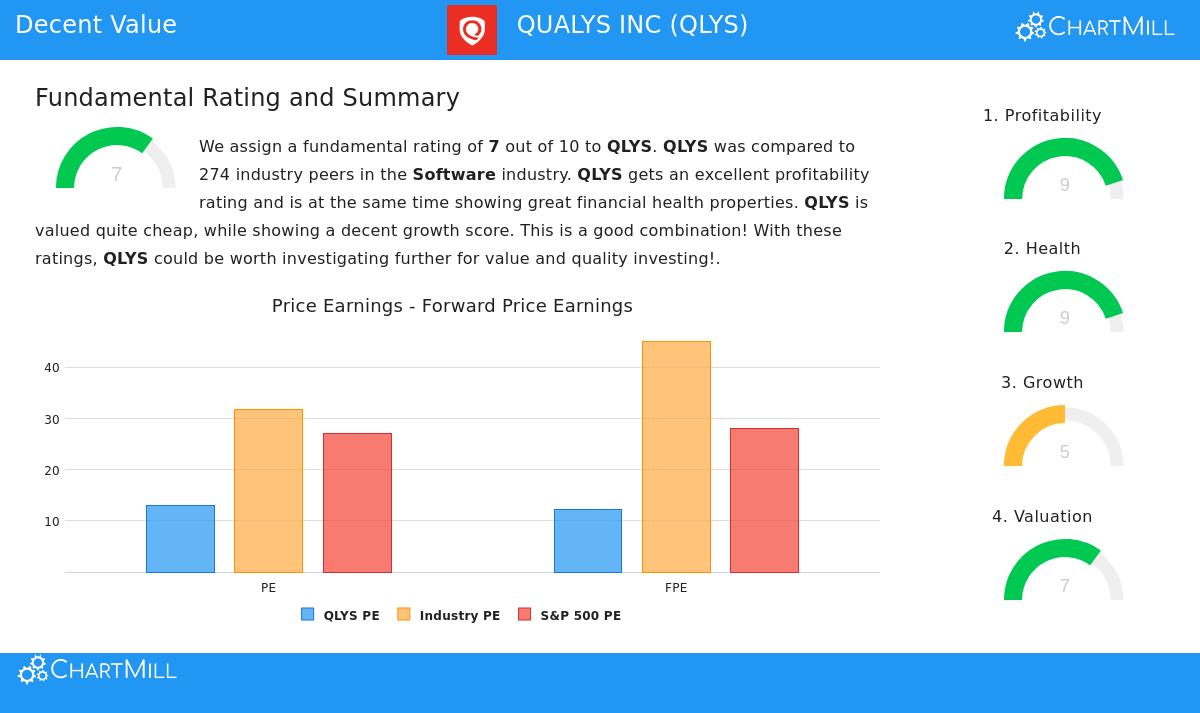

Valuation: An Interesting Starting Price

The most noticeable part of Qualys for a value-focused investor is its price measures. In a market where high prices are common for software and cloud stocks, QLYS sells at levels that imply a lower price.

- Price-to-Earnings (P/E): The company's P/E ratio of 13.06 is much below the S&P 500 average of about 27.10. More significantly, it costs less than 83% of similar companies in the software field.

- Forward P/E and Enterprise Value: This pattern holds with its forward P/E of 12.27 (costing less than almost 80% of the field) and its Enterprise Value to EBITDA ratio, which also shows a price lower than 84% of software companies.

- Price-to-Free-Cash-Flow: Maybe most important, Qualys sells at a Price/Free Cash Flow ratio that is below 89% of its field rivals. For value investors, good free cash flow production at a fair price is a very interesting mix, as it supports the company's financial options and inherent value.

While the report mentions a high PEG ratio, which can mean a costly price when growth is considered, this is greatly balanced by the company's excellent earnings. This better earnings can support a higher earnings multiple, making the present low multiples seem even more interesting.

Financial Health: A Strong Balance Sheet

A key idea of value investing is staying away from companies with too much financial danger. Qualys does very well here, getting a nearly full Health score of 9 out of 10. The company works with no debt on its balance sheet, an uncommon and careful financial state that puts it with the best in its area. This no-debt position removes interest cost danger and gives great operational and planning freedom. Also, its Altman-Z score of 5.05 shows a very small short-term danger of financial trouble, doing better than more than three-quarters of its field. The company has also been steadily lowering its share count over recent years, an action good for shareholders that raises the ownership part of remaining investors.

Profitability: High-Grade Earnings

Value is not only about a low cost; it is about paying a low cost for a high-grade business. Qualys shows excellent earnings, scoring a 9 out of 10. Its measures are not just acceptable; they are field-leading.

- Excellent Margins: The company has a Gross Margin of 82.85%, an Operating Margin of 33.17%, and a Profit Margin of 29.64%. These numbers are better than 87% to 94% of software field peers, showing a very efficient and scalable business model.

- Better Returns on Capital: Qualys produces a Return on Invested Capital (ROIC) of 28.84%, doing better than 96% of its rivals. Importantly, this ROIC is well above the company's cost of capital, meaning it is truly building value for shareholders with each dollar invested. Its Return on Equity of 35.34% and Return on Assets of 18.11% are also top-level.

For a value investor, this degree of earnings is key. It suggests the business has a lasting competitive edge and that the earnings ability shown in the price ratios is lasting and of high grade.

Growth: A Stable, Profitable Path

The filter looked for companies with "acceptable" growth, and Qualys gives a balanced picture here. Its Growth score of 5 shows a history of good performance now moving to more modest, but still positive, outlooks.

- Past Results: Over the last year and on a multi-year average, Qualys has given sound double-digit growth in both Revenue and Earnings Per Share (EPS).

- Future Outlook: Experts estimate future revenue growth near 7% and EPS growth about 6%. While this shows a slowing from past high rates, it means the company is still on a path of increase, not decrease. For a value investor, this reasonable growth outlook can help avoid the "value trap" of a company in lasting drop, while the lower growth rate may be a reason adding to the stock's discounted price.

Conclusion

QUALYS INC shows an example of what value investors frequently look for: a financially very strong company with top-level earnings, selling at a price that seems separate from its basic condition. Its debt-free balance sheet gives an important buffer, while its best-in-class margins and returns on capital show a high-grade business. The expected slowing in growth seems to be the main factor pushing down its market price, making a possible opening for investors who think the company's central earnings and market place stay sound.

This review of Qualys came from a methodical hunt for acceptable value stocks. Investors wanting to look at other companies that fit similar measures of good price, sound health, earnings, and growth can see the full filter results here.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or a deal to buy or sell any security. The review uses data and scores from ChartMill. Investors should do their own complete study and think about their personal money situation and risk comfort before making any investment choices. Past results do not show future outcomes.