For investors looking for chances where the market price may not fully show a company's true worth, a methodical value investing method can be a useful rule. This method, made famous by Benjamin Graham and Warren Buffett, centers on finding stocks selling for less than their true value, often shown by good basics combined with low price measures. The aim is to discover good businesses the market has not noticed or has priced too low for now, offering a possible "margin of safety" for the patient investor. One way to find these companies is by searching for firms with good marks in earnings and money strength, that also have appealing prices based on important value measures.

A present stock that comes up from using this "fair value" search is PAYPAL HOLDINGS INC (NASDAQ:PYPL). The digital payments leader is in an unusual spot: its network is still large and fixed in worldwide online shopping, but its stock price has fallen a lot. A look at its basic report hints the market's present price may not completely include the company's lasting good points, possibly making it a noteworthy option for value-focused study.

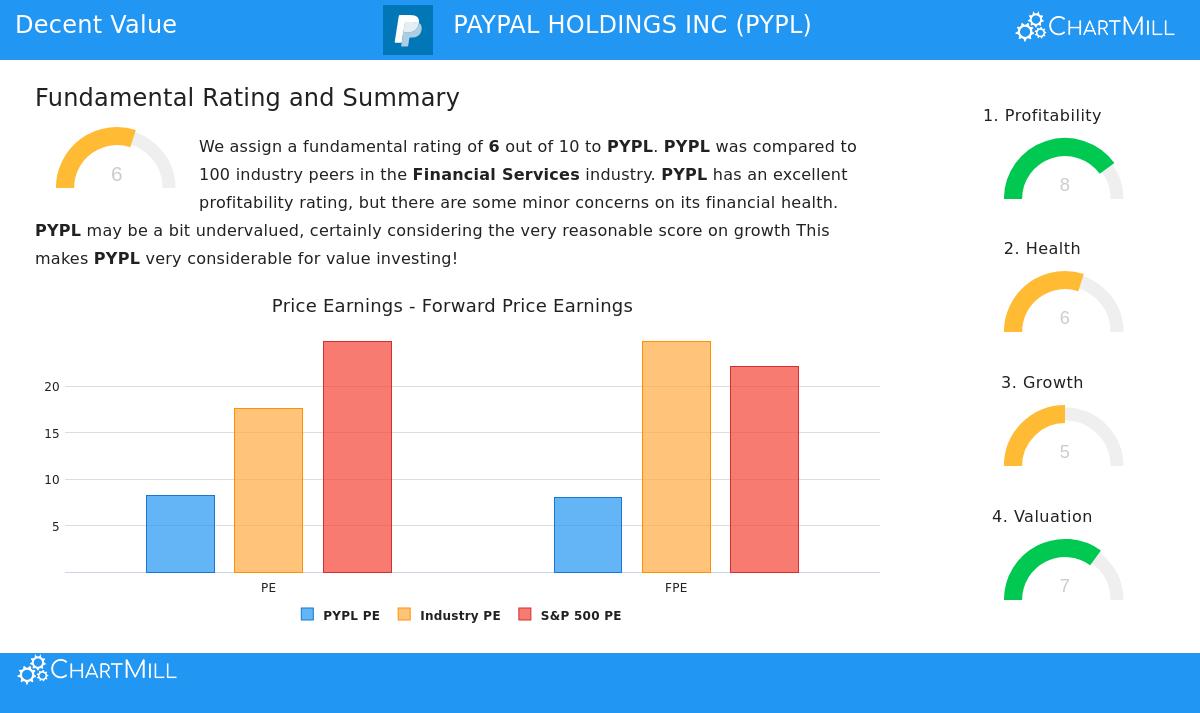

Valuation: The Heart of the Chance

The strongest point for PYPL as a value choice is in its price measures, which seem separate from the company's continuing earnings. For a value investor, a low price compared to earnings and cash flow is the main first step, showing a possible gap from true worth.

- Price-to-Earnings (P/E): PayPal sells at a P/E ratio of 8.22, which is seen as "very low." This is much under the S&P 500 average of 24.88 and also costs less than 66% of similar companies in the Financial Services field.

- Forward P/E: The view stays much the same for the future, with a forward P/E of 8.05, meaning the low price continues based on coming earnings guesses.

- Cash Flow & EBITDA Multiples: The value idea is also backed by cash-based measures. The company's Enterprise Value to EBITDA ratio shows it costs less than 91% of its field rivals, and 83% of similar companies are higher priced based on its Price-to-Free Cash Flow ratio.

These numbers are key to the value investing idea. They imply investors can buy a part of PayPal's earnings and cash flow at a much lower cost than the wider market and most of its direct rivals, giving that needed number-based start for a margin of safety.

Profitability & Money Strength: The Quality Test

A low-priced stock is only a sound investment if the business itself is solid. This is where value investing needs a quality check to steer clear of "value traps," companies that are low-priced for a basically bad reason. PayPal's basic report displays clear good points in these parts.

Profitability is a definite area of strength, with a ChartMill Profitability Rating of 8 out of 10. The company shows high returns on capital:

- Its Return on Invested Capital (ROIC) of 15.26% is better than 93% of the field and is above its cost of capital, proving it makes real economic value.

- Return on Equity is a solid 25.83%, and earnings margins stay good, showing efficient use of owner capital and strong ability to set prices within its system.

Money Strength gets a fair rating of 6. Important debt-paying measures are positive:

- The company has an acceptable Debt-to-Equity ratio of 0.49 and a good Debt-to-Free-Cash-Flow ratio of 2.05, so it could pay all debt in just over two years using its present cash flow.

- Cash position measures are sufficient and match or beat field averages, suggesting no near-term money pressure.

These points are vital for the value plan. They show that PayPal's low price is not mainly caused by a debt disaster or failing earnings, but may be due to other things like growth worries or field changes.

Growth & The Full View

The growth story is where details emerge, seen in a medium Growth Rating of 5. Past sales growth has been fair, averaging above 9% each year lately, though it has become slower recently. For the future, experts predict mild sales growth but a quicker rise in Earnings Per Share (EPS), thought to grow almost 13% each year. This expected EPS growth is a good signal that working efficiency and share buybacks could push owner value even if sales growth becomes steadier.

For a value investor, this varied growth setting is a main piece of the present story. The market often sets a high price for fast growth. PayPal's move to a more settled, cash-making stage has led to a lower price for its stock. Yet, its mix of strong earnings, a sound balance sheet, and a very low price shows a standard value situation: a high-quality business dealing with seen challenges, offered at a cost that may understate its lasting ability to earn and its network benefits.

You can see the full basic study that shapes this view here: Fundamental Analysis of PYPL.

Discovering Like Chances

PayPal shows the kind of chance a planned value search tries to find. For investors wanting to use this "fair value" way to discover other possible options, a set search exists. This filter looks for stocks with good value scores while making sure of basic quality in earnings, strength, and growth. You can see the present results of this search and look at other possible ideas here.

Disclaimer: This article is for information only and is not money advice, a suggestion, or a deal to buy or sell any securities. The study uses data and ratings from ChartMill, and investors should do their own study and think of their personal money situation before any investment choices. Past results do not show future outcomes.