Investors looking to balance the search for growth with fiscal care often use strategies like Growth at a Reasonable Price (GARP). The central concept is to find companies with strong and lasting expansion, but whose shares are not valued at extreme prices that allow no room for error. This method tries to gain from growth paths while reducing the danger of paying too much for future prospects. One way to conduct this search is through systematic filtering, like an "Affordable Growth" filter that selects for stocks with high growth grades, good profitability and financial condition, and at least a fair valuation grade.

Insulet Corp (NASDAQ:PODD) recently appeared from such a filtering process. The medical device company, known for its tubeless Omnipod insulin management system, presents an interesting profile that fits the affordable growth idea. Its fundamental report shows a company performing well in several areas, especially in those important for lasting expansion.

Notable Growth Path

The most noticeable part of Insulet's profile is its strong growth, which received a top ChartMill Growth Rating of 9 out of 10. This grade is based on notable past performance and encouraging future estimates. For a GARP strategy, continued growth is essential, as it is the main driver for future investor gains.

- Revenue Growth: Over the past year, revenue increased by 30.73%. More significantly, the company has shown the ability to keep this pace, with an average yearly revenue growth of 24.53% over recent years.

- Earnings Increase: The bottom-line growth is even more marked. Earnings Per Share (EPS) grew by a notable 49.25% in the last year and has been increasing at an average yearly rate of 73.08%.

- Future Outlook: Analysts anticipate this good performance to persist, though at a somewhat slower speed that stays very appealing. Forecasts suggest average yearly EPS growth of 22.46% and revenue growth of 16.94% in the next years.

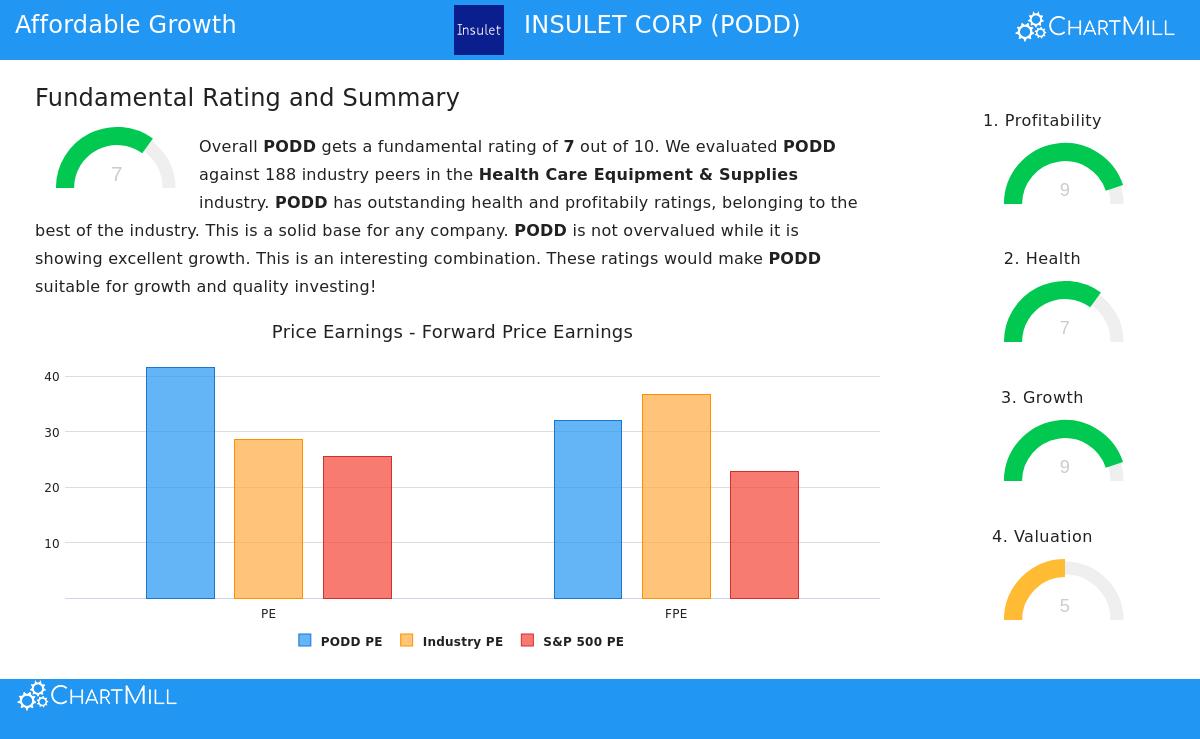

Valuation Considered

With such excellent growth, a higher valuation is anticipated. Insulet's ChartMill Valuation Rating of 5 shows a varied situation, which is exactly the detailed scenario a GARP investor reviews. The rating implies the stock is not low-cost in simple terms, but its price may be fair compared to its growth outlook and industry counterparts.

- Absolute Multiples: On its own, measures like a Price/Earnings (P/E) ratio of 41.66 and a Forward P/E of 32.02 point to a high-priced stock, particularly when measured against the wider S&P 500.

- Relative Value: The setting is key. Compared to its peers in the Health Care Equipment & Supplies industry, Insulet seems more fairly priced. Its P/E ratio is below about 69% of the industry, and its Forward P/E is less expensive than around 71% of rivals.

- Growth Adjustment: Important for GARP review, the PEG ratio—which modifies the P/E for growth—is mentioned as showing a "correct valuation." This indicates the market price may suitably account for the company's high growth rate. The fundamental report clearly says that the high profitability and anticipated earnings growth "may justify a more costly valuation."

Supporting Strength: Profitability and Financial Condition

A growth narrative is only lasting if based on a firm base. This is where Insulet's high grades in Profitability (9) and Financial Health (7) become important. For the affordable growth strategy, these scores offer assurance that the company can finance its growth from within and manage economic challenges.

Profitability Points:

- The company has good and getting better margins, with a Profit Margin of 9.12% and an Operating Margin of 17.50%, each doing better than a large portion of industry peers.

- Returns on capital are very good, with a Return on Invested Capital (ROIC) of 13.74% that puts it in the high group of its industry, showing efficient use of investor capital to create profits.

Financial Condition Review:

- The company shows acceptable liquidity, with a Current Ratio of 2.81 and a Quick Ratio of 2.15, indicating no immediate solvency issues.

- Its Altman-Z score of 7.15 shows a very small short-term bankruptcy risk.

- While the company has some debt, with a Debt-to-Equity ratio of 0.61, its good free cash flow production means it could in theory pay off all debt in about 2.7 years, a positive standing compared to peers.

Conclusion

Insulet Corp represents the qualities desired in an affordable growth investment. It is not a low-price stock, but its valuation seems considered next to its excellent growth rate, high profitability, and acceptable financial position. The company works in a stable healthcare area with a new product, and its financial measures suggest it is carrying out its growth plan successfully. For investors, this profile shows a possible chance to take part in a good growth story without paying a very high price for the opportunity.

A detailed look at Insulet's fundamental analysis, including the complete report with all basic measures, is ready for more study here.

This review of Insulet Corp came from a particular filtering method. Investors curious about finding other companies that meet similar standards of acceptable growth, fair valuation, and good fundamentals can examine more outcomes using the Affordable Growth stock screener.

Disclaimer: This article is for information only and does not make up financial advice, a suggestion to buy or sell any security, or a support of any investment plan. The information given is based on supplied data and should not be the only foundation for an investment choice. Investors should do their own complete research and think about their personal financial situation and risk comfort before making any investment.