For investors looking for a disciplined, long-term way to build wealth, few strategies are as respected as Peter Lynch’s method. The famous manager of the Fidelity Magellan Fund supported investing in what you understand, concentrating on companies with clear operations, lasting growth, and fair prices. His thinking, often called Growth at a Reasonable Price (GARP), avoids speculative trends for basic soundness. It focuses on locating companies increasing at a steady, manageable rate, not too slow, but not so quick that it turns unstable, and buying their stock when it seems priced below that growth possibility. This structure gives a solid checklist for finding lasting businesses suitable for a long-term portfolio.

One company that now meets a filter built on Lynch’s main standards is Paycom Software Inc (NYSE:PAYC), a supplier of cloud-based human capital management (HCM) software. The company’s complete system manages all tasks from payroll and hiring to HR operations, helping businesses aiming to simplify their employee administration. We can review how Paycom’s financial picture matches the ideas of GARP investing.

Match with Peter Lynch Standards

Peter Lynch’s filter uses particular number-based tests to find companies with the correct mix of growth, financial soundness, and price. Paycom’s present measurements indicate a good match:

- Lasting Earnings Growth: Lynch preferred companies with a confirmed history of growth, but cautioned against overly high rates that might not continue. The filter seeks a 5-year earnings per share (EPS) growth rate from 15% to 30%. Paycom’s EPS has increased at a typical yearly rate of 21.5% over the last five years, putting it directly in this preferred zone of solid yet possibly maintainable increase.

- Fair Price (PEG Ratio): Maybe the central part of the GARP method is the Price/Earnings to Growth (PEG) ratio, which changes the standard P/E ratio for a company’s growth rate. Lynch viewed a PEG ratio of 1 or below as a mark of good price. Paycom’s PEG ratio, calculated from its past growth, is about 0.57. This implies the market could be pricing the company’s historical growth path too low, a main sign for Lynch-type investors.

- High Profitability (Return on Equity): To confirm a company is using shareholder money well, Lynch demanded a high Return on Equity (ROE). The filter sets a lowest point of 15%. Paycom greatly passes this level with an ROE of 26.2%, showing high profitability and capable management.

- Good Financial Soundness: Lynch gave importance to companies with firm balance sheets to handle economic declines. Two main tests are:

- Minimal Debt: The method chooses a Debt-to-Equity ratio under 0.6, with Lynch himself liking even lower amounts. Paycom does very well here with a Debt/Equity ratio of 0.0, meaning it functions with no interest-owing debt, a notable sign of financial firmness and choice.

- Sufficient Cash: A Current Ratio (current assets divided by current debts) of at least 1 makes sure a company can pay its near-term bills. Paycom’s Current Ratio of 1.09 satisfies this basic need, showing acceptable cash.

Basic Soundness and Price Summary

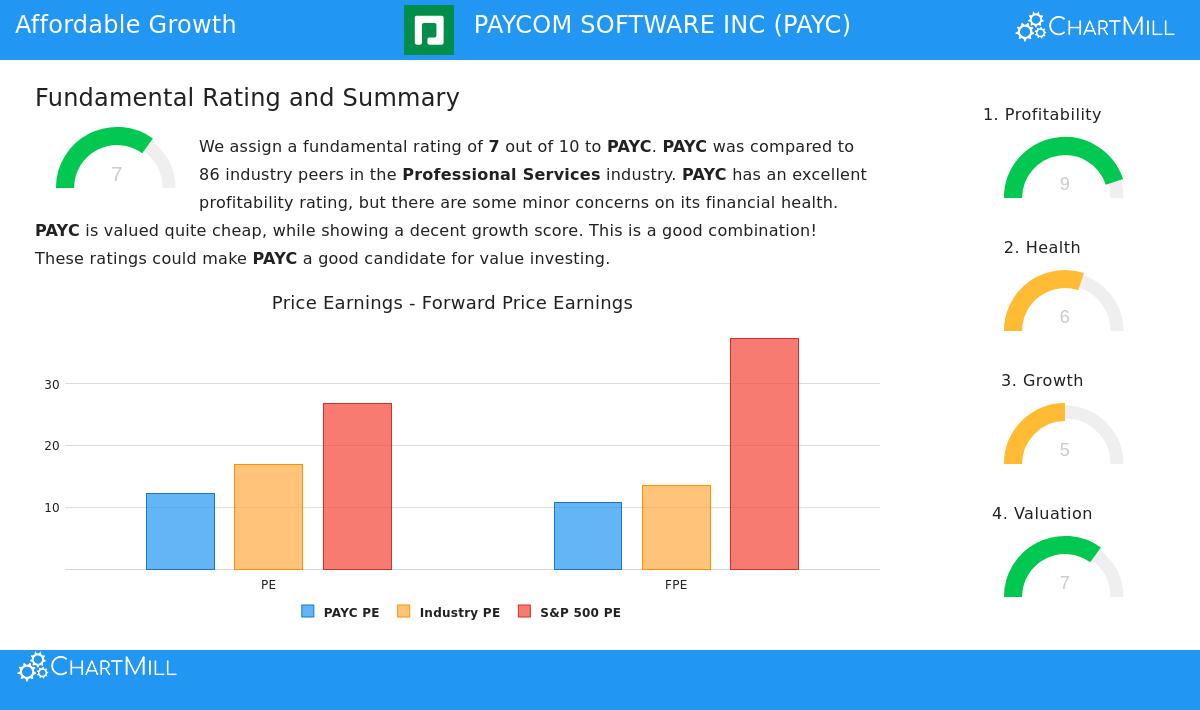

Beyond the specific filter standards, a wider view of Paycom’s basic report shows a company with notable profitability but some points for investor examination. The company gets a high profitability grade, pushed by very good margins and returns on capital. Its price measurements seem appealing compared to both its industry and the wider market, with a P/E ratio that looks low next to the S&P 500 average.

However, the financial soundness grade is more average. While the clean, debt-free balance sheet is a large plus, experts see questions about the company’s Altman Z-Score, a test of bankruptcy danger, and its cash ratios are not as strong as many industry competitors. Growth is also predicted to slow from its historical peaks, with future guesses for sales and earnings indicating a more gradual, though still good, path.

For a complete summary of these positives and negatives, you can see the full basic analysis report for PAYC.

Is Paycom a Lynch-Type "GARP" Choice?

Combining the information, Paycom Software makes a strong case for investors using a GARP philosophy. It meets the necessary points Peter Lynch highlighted: a clear business in the important area of payroll and HR software, a firm past of earnings growth in a maintainable span, and a price that seems fair when that growth is considered. The company’s outstanding profitability and total absence of debt are more pillars of basic quality that fit a long-term, buy-and-hold approach.

The main thoughts for a possible investor would be the expected slowing in growth and the varied signs from some financial soundness tests. A genuine Lynch follower would use this filter as a beginning for more study, looking into the causes behind the dropping growth predictions and judging the company’s competitive position in the full HCM software field.

Locating More Possible Investments

The Peter Lynch method is made to methodically find companies with these wanted features. Paycom Software is one of the stocks that lately passed this strict filter. For investors trying to build a varied collection of similar GARP-type stocks, new options can be located by using the filter often.

You can see the present outcomes and use the filter yourself here: Peter Lynch Strategy Stock Filter.

Disclaimer: This article is for information only and is not financial guidance, a suggestion, or a plan to buy or sell any security. The study uses data and a set filtering system; it does not include personal investment goals or money situations. Investors should do their own complete research and think about talking with a registered financial advisor before making any investment choices.