For investors looking for a disciplined, long-term market method, few strategies have the substance of Peter Lynch's approach. The famous manager of the Fidelity Magellan Fund supported putting money into what you understand, concentrating on companies with clear operations, maintainable expansion, and fair prices. His model is frequently called a "growth at a reasonable price" (GARP) method, intending to sidestep the extremes of speculative growth stocks while gaining the compounding effect of financially stable, enlarging businesses. A filter built on Lynch's central ideas, including tests for earnings, financial soundness, and price, can reveal companies deserving of more detailed study.

One company found by this filter is PAYCOM SOFTWARE INC (NYSE:PAYC), a supplier of cloud-based human capital management (HCM) software. The company provides a full set of tools that manages all tasks from hiring and payroll to talent development, all inside one system. For investors using Lynch's perspective, Paycom offers a strong example of how a contemporary software company can match classic investment guidelines.

Match with Peter Lynch Standards

Peter Lynch stressed maintainable expansion, financial soundness, and good price. The filter settings are made to select for these precise traits, and Paycom's present measurements show a solid match.

- Maintainable Earnings Expansion: Lynch preferred companies increasing earnings per share (EPS) between 15% and 30% each year, quick enough to be a frontrunner, but not so unstable that the speed is unmaintainable. Paycom’s five-year average EPS expansion of 21.5% rests well inside this goal zone, showing a record of solid, yet possibly steady, enlargement.

- Fair Price (PEG Ratio): A central part of the GARP method is the PEG ratio, which modifies the common price-to-earnings (P/E) ratio for expansion. Lynch wanted companies with a PEG of 1 or lower, hinting the market is not overpaying for future expansion. Paycom’s PEG ratio, calculated from its past five-year expansion, is about 0.62, indicating the stock may be priced low relative to its historical expansion path.

- High Earnings (ROE): Return on equity (ROE) calculates how well a company produces profits from shareholder funds. Lynch searched for an ROE above 15%. Paycom’s ROE of 26.2% is outstanding, showing high earnings and good management use of equity capital.

- Sound Financial Condition: Lynch was cautious about high debt. The filter demands a debt-to-equity ratio below 0.6, and Paycom meets this well with a ratio of 0.0, meaning it functions with no interest-bearing debt. Also, its current ratio of 1.09 meets the filter’s lowest limit of 1, suggesting it has enough short-term resources to meet its immediate obligations.

Fundamental Condition Review

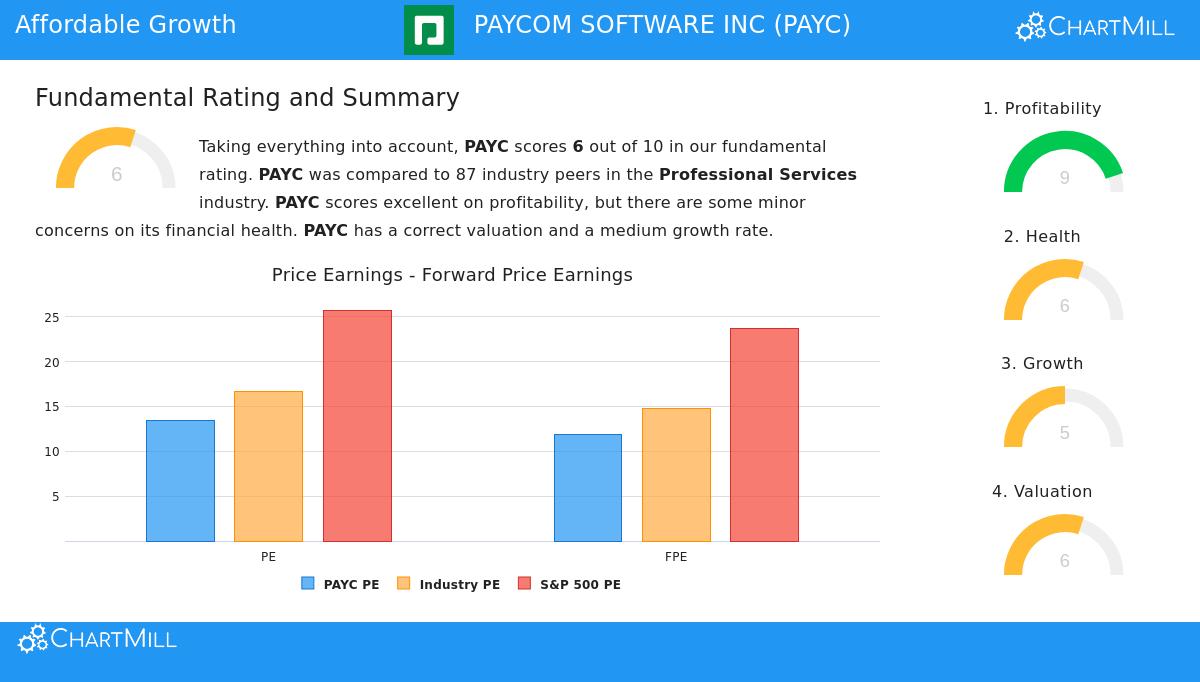

A wider view of Paycom’s fundamental picture, as shown in its detailed analysis report, supports the image created by the Lynch filter. The company gets a total fundamental score of 6 out of 10, with definite positives and some parts to watch.

Main Positives:

- Outstanding Earnings: Paycom gets a 9 out of 10 for earnings. It has sector-leading margins, including a gross margin above 83% and an operating margin close to 28%. Its return on invested capital (ROIC) of over 19% also places in the top group of its professional services industry peers.

- Clear Balance Sheet: The lack of debt is a major benefit, giving notable financial room and stability. The company also has a record of lowering its share count through buybacks, another detail Lynch saw as positive.

- Fair Price: Compared to both its sector and the wider S&P 500, Paycom’s price multiples (P/E, Forward P/E, EV/EBITDA) seem moderate to low, particularly when viewed next to its high earnings.

Parts for Review:

- Expansion Slowdown: Experts forecast a reduction in both sales and EPS expansion over the coming years compared to the past five-year averages. This is a vital detail for GARP investors to study more, as the future expansion rate is a key part of the investment case.

- Liquidity Measurements: While the current ratio is above 1, it is lower than many sector peers. Also, the company’s Altman Z-Score, a measure of financial firmness, is noted as a point of attention, though it matches the sector average.

Summary

For an investor using a Peter Lynch-style GARP method, PAYCOM SOFTWARE INC offers a notable prospect. It meets the main conditions: a history of solid, within-range earnings expansion, a price that seems fair when expansion is considered, high earnings, and a very strong balance sheet with no debt. The company works in the understandable, repeat-revenue area of cloud software, addressing a basic business requirement.

Still, the Lynch approach needs more than just clearing a filter; it requires detailed study. The expected slowdown in expansion and the details of its liquidity measurements are important factors for any investor to learn before making a long-term decision. The filter acts as a beginning, finding companies that have historically followed the ideas of growth at a reasonable price.

You can review other companies that clear this disciplined investment filter by going to the Peter Lynch Strategy screener.

Disclaimer: This article is for information only and does not form financial guidance, a suggestion, or an offer to buy or sell any security. The study is based on data and a particular investment method structure; it is not a replacement for your own study and careful review. Investing includes risk, including the possible loss of initial funds.