Paycom Software Inc (NYSE:PAYC) has become an interesting option for investors using the Peter Lynch investment method. This strategy, explained in Lynch's book One Up on Wall Street, looks for companies with maintainable growth paths that are available at fair prices. The method focuses on fundamental soundness rather than market prediction, searching for businesses with good profitability, acceptable debt, and steady earnings growth that stays within maintainable limits. Lynch's idea is to find what he called "growth at a reasonable price" opportunities, companies that mix growth features with value investing ideas.

Company Summary and Business Method

Paycom Software offers cloud-based human capital management tools that assist businesses in handling the complete employee lifecycle using a single database system. The company's software-as-a-service platform manages all functions from hiring and onboarding to payroll and talent management. Based in Oklahoma City, Paycom has kept its standing in the competitive HR technology field by providing a full solution that needs little adjustment. The company became public in 2014 and has since grown to employ more than 7,300 people while serving clients in different industries looking to make their HR tasks more efficient.

Growth Measurements and Maintainability

The Peter Lynch strategy stresses earnings growth that is significant but also maintainable, usually focusing on companies with 5-year EPS growth between 15% and 30%. Paycom displays solid performance in this band, with an 18.56% average yearly EPS growth over the last five years. This growth rate shows the company has been enlarging at a sound speed without hitting the high levels Lynch viewed as unstable. The steadiness of this growth path implies Paycom has built a repeatable business method able to continue its progress without needing improbable expansion rates that could cause future letdowns.

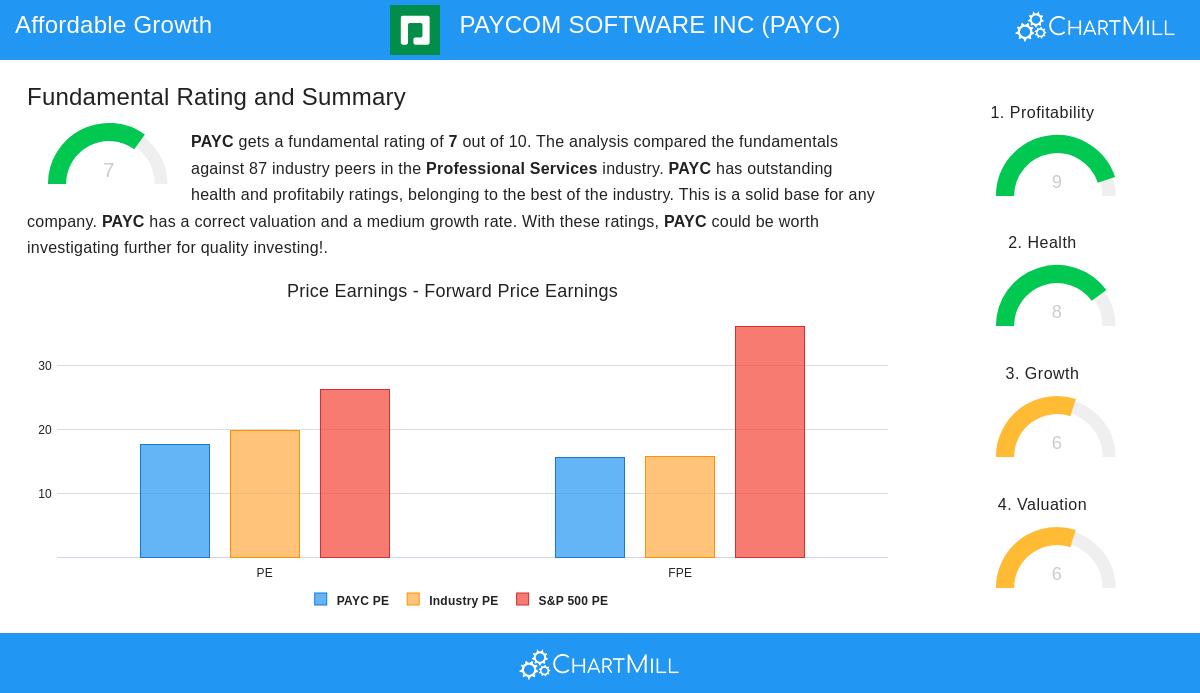

Valuation Review

Lynch gave great weight to the PEG ratio, which measures a company's P/E ratio against its growth rate, with numbers under 1.0 suggesting possible under pricing. Paycom's PEG ratio of 0.95 sits well within Lynch's favored band, indicating the market might be under pricing the company compared to its growth path. Other valuation measurements from the fundamental analysis report back this review:

- P/E ratio of 17.63 is good compared to industry and S&P 500 averages

- Price/Forward Earnings ratio of 15.63 shows fair future outlooks

- Enterprise Value to EBITDA ratio places the company as less expensive than 70% of industry rivals

Financial Condition and Profitability

Lynch favored companies with sound balance sheets and very good profitability measurements, and Paycom does well in both areas. The company holds no outstanding debt, greatly surpassing Lynch's liking for debt-to-equity ratios below 0.6. This absence of debt gives notable financial room and lowers risk during economic slowdowns. The company's return on equity of 26.51% greatly passes Lynch's 15% mark, showing effective use of shareholder money. More strength is visible in margin measurements, with operating margins of 27.91% and profit margins of 22.64% rating near the top in the professional services field.

Fundamental Soundness Summary

Paycom's full fundamental analysis report gives the company a total rating of 7 out of 10, with especially good scores in profitability (9/10) and financial condition (8/10). The report notes the company's very good return measurements, getting better margins, and sound cash flow creation. While growth outlooks have softened from past levels, analysts still forecast solid forward EPS growth of about 12.55% each year. The company's current ratio of 1.22 shows enough cash to meet short-term responsibilities, although this measurement is a bit under industry averages.

Investment Points

For investors applying the Peter Lynch method, Paycom stands for the kind of business that joins understandable activities with sound fundamental performance. The company works in the fairly clear HR technology sector, giving necessary services that businesses frequently use and comprehend. Its debt-free balance sheet, steady profitability, and fair valuation relative to growth form a profile that fits well with Lynch's rules of investing in financially sound companies at sensible prices.

The company does encounter some tests, including softening revenue growth outlooks and competitive forces in the HCM software area. However, its sound market position, steady performance, and strong financial measurements suggest it has the qualities Lynch prized for long-term investment success.

For investors wanting to find more companies that fit the Peter Lynch investment requirements, more screening outcomes can be found through this link.

Disclaimer: This analysis is for information only and does not form investment advice, suggestion, or support of any security. Investors should do their own research and talk with financial advisors before making investment choices. Past performance does not ensure future outcomes.